Advertisement

3 High Insider Ownership Growth Companies On Chinese Exchanges With Earnings Growth Up To 107%

Simply Wall St

Reviewed by Simply Wall St

Amid a backdrop of rate cuts and economic reassessment in China, the local equity markets have shown volatility, reflecting investor concerns about the country's near-term economic trajectory. In such an environment, focusing on growth companies with high insider ownership might offer investors a unique blend of growth potential and aligned interests between shareholders and management.

Top 10 Growth Companies With High Insider Ownership In China

| Name | Insider Ownership | Earnings Growth |

| Anhui Huaheng Biotechnology (SHSE:688639) | 31.5% | 26.5% |

| Ningbo Sunrise Elc TechnologyLtd (SZSE:002937) | 24.3% | 27.7% |

| ShenZhen Woer Heat-Shrinkable MaterialLtd (SZSE:002130) | 19% | 27.9% |

| Zhejiang Jolly PharmaceuticalLTD (SZSE:300181) | 24% | 22.3% |

| Cubic Sensor and InstrumentLtd (SHSE:688665) | 10.1% | 34.3% |

| KEBODA TECHNOLOGY (SHSE:603786) | 12.8% | 25.1% |

| Arctech Solar Holding (SHSE:688408) | 38.7% | 28.4% |

| Suzhou Sunmun Technology (SZSE:300522) | 36.5% | 63.4% |

| Sineng ElectricLtd (SZSE:300827) | 36.5% | 39.8% |

| UTour Group (SZSE:002707) | 23% | 33.1% |

Let's review some notable picks from our screened stocks.

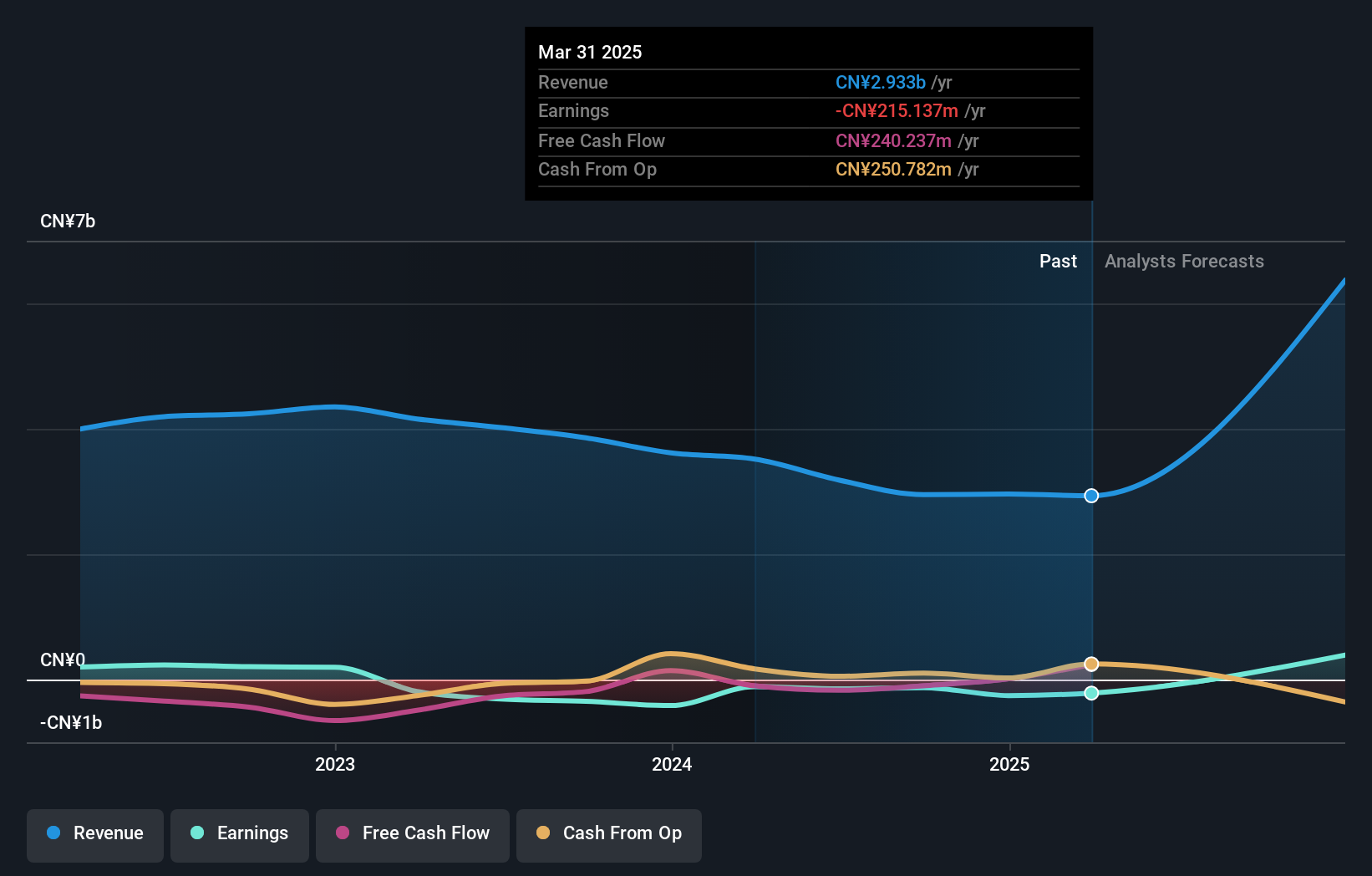

Asian Star Anchor Chain Jiangsu (SHSE:601890)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Asian Star Anchor Chain Co., Ltd. Jiangsu specializes in producing and selling anchor chains, marine mooring chains, and related accessories globally, with a market capitalization of approximately CN¥6.91 billion.

Operations: The company generates its revenue primarily from the production and sales of anchor chains and marine mooring chains, along with associated accessories on a global scale.

Insider Ownership: 37.9%

Earnings Growth Forecast: 23.6% p.a.

Asian Star Anchor Chain Jiangsu exhibits promising growth with its revenue and earnings forecast to increase by 21.7% and 23.6% per year respectively, outpacing the broader Chinese market. Despite this, the company's Return on Equity is expected to remain low at 10.7% in three years. Additionally, its dividend coverage by free cash flows is weak. Analysts predict a significant potential price increase of 41.8%, noting the stock is trading at a 22.9% discount to fair value.

- Click to explore a detailed breakdown of our findings in Asian Star Anchor Chain Jiangsu's earnings growth report.

- Our valuation report here indicates Asian Star Anchor Chain Jiangsu may be undervalued.

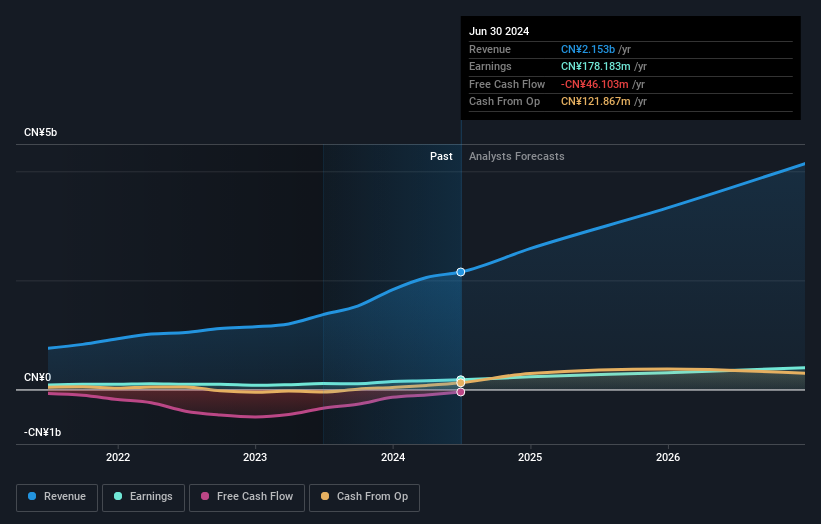

Miracle Automation EngineeringLtd (SZSE:002009)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Miracle Automation Engineering Co., Ltd specializes in providing intelligent equipment solutions and services both domestically and internationally, with a market capitalization of approximately CN¥4.23 billion.

Operations: The company generates its revenue through the provision of intelligent equipment solutions and services across both domestic and international markets.

Insider Ownership: 28.6%

Earnings Growth Forecast: 107.1% p.a.

Miracle Automation Engineering Ltd is poised for significant growth, with earnings expected to surge by 107.05% annually. The company's revenue growth at 33.1% per year also outstrips the broader Chinese market forecast of 13.6%. However, financial challenges persist as its debt is poorly covered by operating cash flow, and shareholder dilution occurred over the past year. Despite these concerns, the firm is trading at a good value relative to its peers and industry standards.

- Unlock comprehensive insights into our analysis of Miracle Automation EngineeringLtd stock in this growth report.

- The valuation report we've compiled suggests that Miracle Automation EngineeringLtd's current price could be quite moderate.

Wuxi Longsheng TechnologyLtd (SZSE:300680)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Wuxi Longsheng Technology Co., Ltd specializes in the production of auto parts in China, with a market capitalization of approximately CN¥4.46 billion.

Operations: The company generates its revenue primarily from the production of auto parts in China.

Insider Ownership: 35.2%

Earnings Growth Forecast: 31.2% p.a.

Wuxi Longsheng TechnologyLtd, despite its recent exclusion from the S&P Global BMI Index, shows promising financial prospects with expected earnings growth of 31.24% annually and revenue increases forecasted at 25% per year, outpacing the Chinese market average. However, its low forecasted return on equity of 14.4% and a dividend yield of 1.02% poorly covered by free cash flows signal potential concerns in capital management and shareholder returns amidst a highly volatile share price over the past three months.

- Navigate through the intricacies of Wuxi Longsheng TechnologyLtd with our comprehensive analyst estimates report here.

- The valuation report we've compiled suggests that Wuxi Longsheng TechnologyLtd's current price could be inflated.

Make It Happen

- Click this link to deep-dive into the 363 companies within our Fast Growing Chinese Companies With High Insider Ownership screener.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:601890

Asian Star Anchor Chain Jiangsu

Engages in the manufacture and sale of anchor chains, marine mooring chains, and related accessories worldwide.

High growth potential with excellent balance sheet and pays a dividend.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|7.3% undervalued

AN

Based on Analyst Price Targets