Advertisement

- China

- /

- Electrical

- /

- SHSE:688663

Undiscovered Gems in Asia February 2025

Simply Wall St

Reviewed by Simply Wall St

As we navigate the complexities of the Asian markets in February 2025, investors are keenly observing how geopolitical tensions and economic indicators impact small-cap stocks. With major indices experiencing volatility amid global uncertainties, identifying promising opportunities requires a focus on companies that demonstrate resilience and adaptability. In this context, undiscovered gems in Asia may offer potential for growth as they leverage unique market positions and innovative strategies to thrive amidst broader market challenges.

Top 10 Undiscovered Gems With Strong Fundamentals In Asia

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Intelligent Wave | NA | 7.78% | 15.50% | ★★★★★★ |

| AOKI Holdings | 27.05% | 3.74% | 52.54% | ★★★★★★ |

| Macnica Galaxy | 52.99% | 8.23% | 18.45% | ★★★★★★ |

| Korea Airport ServiceLtd | NA | 7.52% | 53.96% | ★★★★★★ |

| DorightLtd | 0.56% | 14.02% | 7.14% | ★★★★★★ |

| Xuchang Yuandong Drive ShaftLtd | 0.38% | -11.74% | -29.32% | ★★★★★★ |

| Grade Upon Technology | 4.99% | 7.57% | 67.08% | ★★★★★★ |

| Suzhou Nanomicro Technology | 6.31% | 23.88% | -2.17% | ★★★★★★ |

| Chongqing Changjiang River Moulding Material (Group) | 7.05% | 4.22% | 14.03% | ★★★★★☆ |

| Keli Motor Group | 21.66% | 9.99% | -12.19% | ★★★★★☆ |

Here's a peek at a few of the choices from the screener.

Paradise Entertainment (SEHK:1180)

Simply Wall St Value Rating: ★★★★★☆

Overview: Paradise Entertainment Limited is an investment holding company that primarily offers casino management services in Macau, the People's Republic of China, and the United States, with a market capitalization of approximately HK$1.99 billion.

Operations: The company generates revenue primarily from casino management services, contributing HK$681.22 million, and gaming systems, which add HK$121.46 million. An additional revenue stream comes from innovative and renewable energy solutions business at HK$10.15 million.

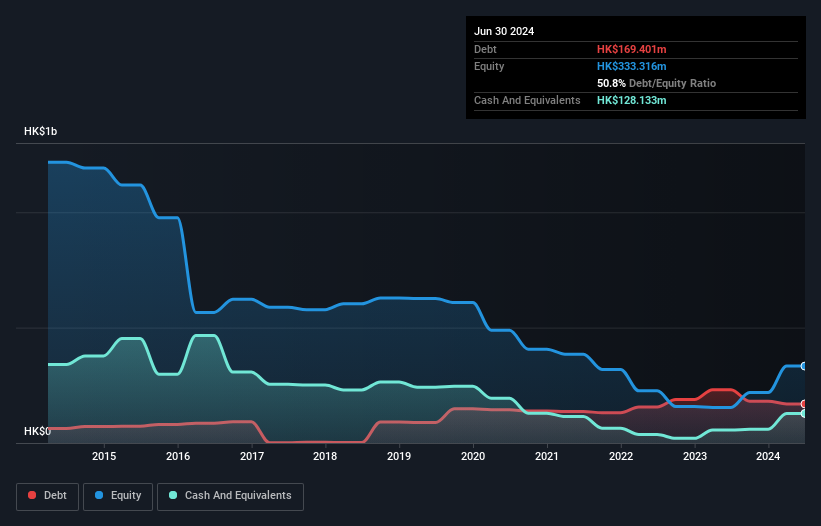

Paradise Entertainment, a smaller player in the gaming industry, has shown notable financial movements recently. The company became profitable last year, outperforming its peers with high-quality earnings and an EBIT covering interest payments 13.9 times over. Trading at 46.8% below fair value estimates, it presents an intriguing valuation opportunity despite a debt-to-equity ratio that climbed from 14.2% to 50.8% over five years. Recent changes in company bylaws indicate strategic shifts potentially aimed at streamlining operations or governance structures, which might influence future growth prospects positively as earnings are forecasted to rise by 14%.

WindSun Science&TechnologyLtd (SHSE:688663)

Simply Wall St Value Rating: ★★★★★★

Overview: WindSun Science&Technology Co., Ltd. focuses on the research, development, production, sale, and service of power electronic energy-saving control technology and related products in China with a market cap of CN¥3.68 billion.

Operations: WindSun Science&Technology Co., Ltd. generates revenue primarily through the sale of power electronic energy-saving control products. The company has a market capitalization of CN¥3.68 billion, reflecting its valuation in the industry.

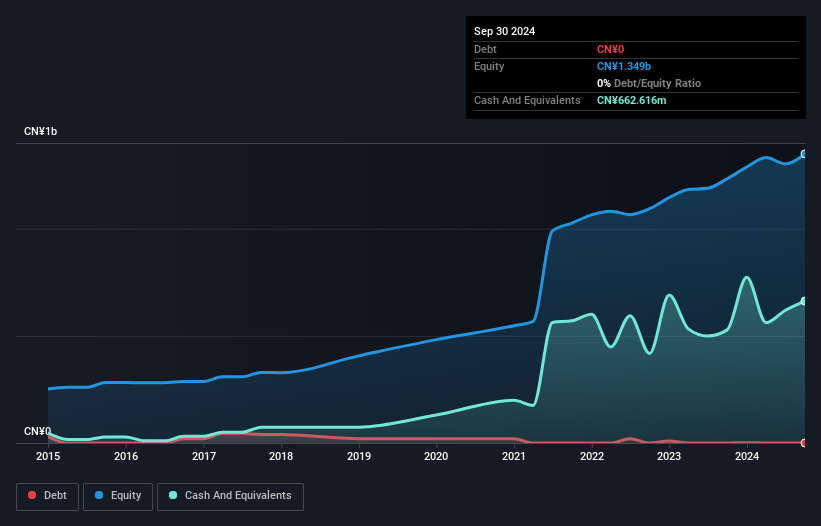

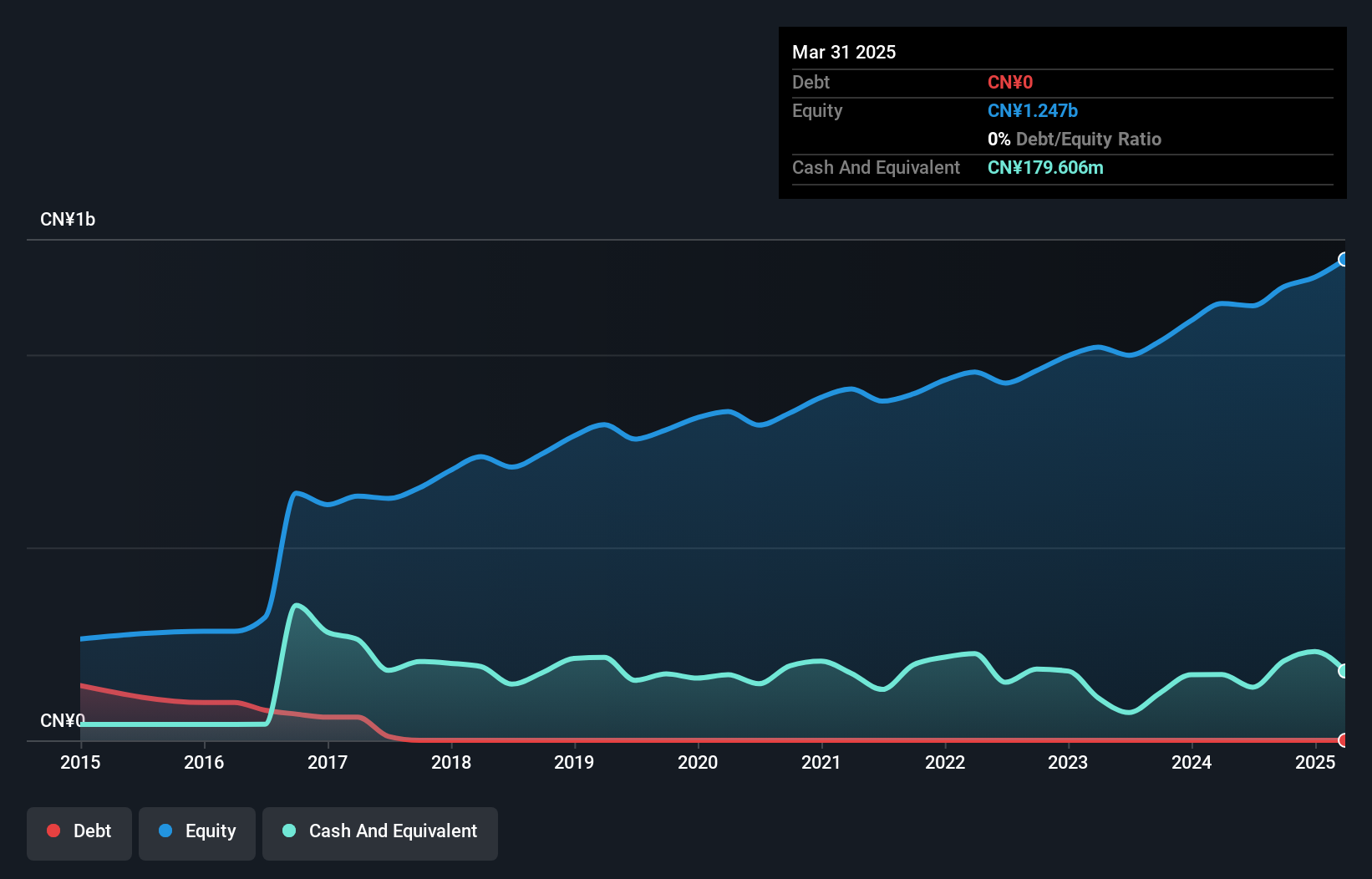

WindSun Science & Technology Ltd. showcases a promising profile with earnings growth of 2.8%, outpacing the Electrical industry's 0.8% rise, and trades at a significant discount of 32.7% below its estimated fair value. The company is debt-free, enhancing its financial stability compared to five years ago when it had a debt-to-equity ratio of 4.3%. Recent earnings reported sales of CNY 1,894 million and net income reached CNY 170 million, reflecting steady performance over the past year. With high-quality earnings and no concerns about cash runway due to profitability, WindSun appears well-positioned for continued growth in its sector.

- Click to explore a detailed breakdown of our findings in WindSun Science&TechnologyLtd's health report.

Gain insights into WindSun Science&TechnologyLtd's past trends and performance with our Past report.

Sichuan Chuanhuan TechnologyLtd (SZSE:300547)

Simply Wall St Value Rating: ★★★★★★

Overview: Sichuan Chuanhuan Technology Co., Ltd. specializes in the research, development, production, and sale of automotive rubber hose products in China, with a market capitalization of CN¥9.18 billion.

Operations: Sichuan Chuanhuan Technology generates revenue primarily from its non-tire rubber products segment, amounting to CN¥1.30 billion. The company's financial performance can be analyzed through its net profit margin, which reflects the efficiency of converting revenue into actual profit after all expenses.

Chuanhuan Tech, a nimble player in the auto components sector, showcases robust financial health with no debt over the past five years and high-quality earnings. The company has maintained positive free cash flow, recently hitting US$120.38M, while capex stands at US$56.06M. Despite its volatile share price in recent months, Chuanhuan's earnings growth of 37% last year outpaced the industry average of 11%. Looking ahead, earnings are projected to grow by 21% annually. These figures suggest a promising outlook for this small yet dynamic enterprise within its industry landscape.

- Navigate through the intricacies of Sichuan Chuanhuan TechnologyLtd with our comprehensive health report here.

Learn about Sichuan Chuanhuan TechnologyLtd's historical performance.

Next Steps

- Access the full spectrum of 2563 Asian Undiscovered Gems With Strong Fundamentals by clicking on this link.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if WindSun Science&TechnologyLtd might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688663

WindSun Science&TechnologyLtd

Engages in the research and development, production, sale, and service of power electronic energy-saving control technology and related products in China.

Flawless balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor