- China

- /

- Auto Components

- /

- SZSE:300547

3 Growth Companies With High Insider Ownership Boasting 35% ROE

Reviewed by Simply Wall St

As global markets rally in response to anticipated interest rate cuts from the Federal Reserve, investors are turning their attention to growth companies with strong fundamentals. In this article, we will explore three such companies that not only boast impressive growth but also have high insider ownership and a remarkable 35% return on equity (ROE).

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Atlas Energy Solutions (NYSE:AESI) | 29.1% | 42.7% |

| Hartshead Resources (ASX:HHR) | 13.9% | 102.6% |

| People & Technology (KOSDAQ:A137400) | 16.5% | 35.6% |

| Seojin SystemLtd (KOSDAQ:A178320) | 30.9% | 52.1% |

| Gaming Innovation Group (OB:GIG) | 26.7% | 37.4% |

| On Holding (NYSE:ONON) | 28.4% | 24.4% |

| Adveritas (ASX:AV1) | 21.1% | 103.9% |

| HANA Micron (KOSDAQ:A067310) | 21.3% | 97.4% |

| UTI (KOSDAQ:A179900) | 33.1% | 122.7% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 77% |

Below we spotlight a couple of our favorites from our exclusive screener.

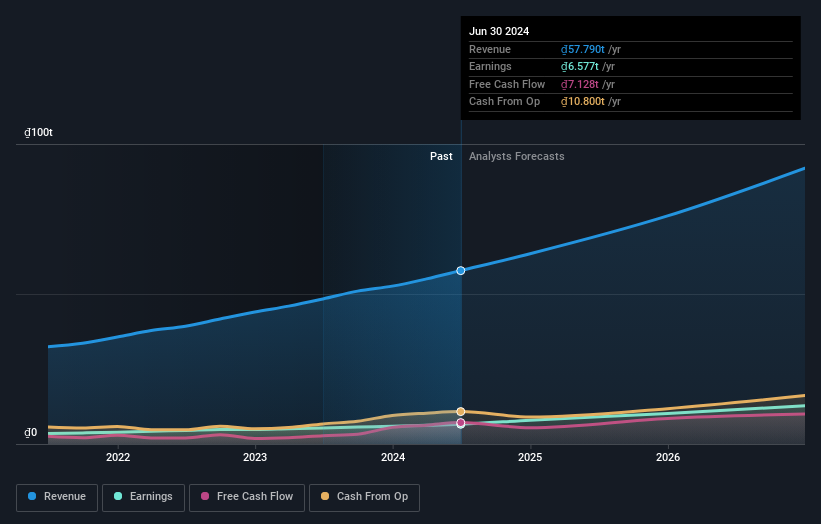

FPT (HOSE:FPT)

Simply Wall St Growth Rating: ★★★★★☆

Overview: FPT Corporation offers IT and telecommunication products and services both in Vietnam and internationally, with a market cap of ₫194.39 trillion.

Operations: The company's revenue segments include ₫63.95 billion from Digital Content, ₫15.73 billion from Telecommunication, ₫27.63 billion from Global IT Services, and ₫7.70 billion from Software Solutions, System Integration, and Informatics Services.

Insider Ownership: 12.2%

Return On Equity Forecast: 29% (2027 estimate)

FPT Corporation's earnings grew 22.7% over the past year and are forecast to grow 25.86% annually, outpacing the VN market's growth rate of 20.2%. Recent Q2 results showed revenue of VND 15.25 trillion (up from VND 12.48 trillion) and net income of VND 1.87 trillion (up from VND 1.51 trillion). FPT recently expanded its presence in Malaysia, enhancing its delivery capabilities and aiming to add up to 500 experts within three years, focusing on emerging technologies like AI.

- Dive into the specifics of FPT here with our thorough growth forecast report.

- In light of our recent valuation report, it seems possible that FPT is trading behind its estimated value.

Perfect Presentation for Commercial Services (SASE:7204)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Perfect Presentation for Commercial Services Company (SASE:7204) is an ICT services and technology solutions provider in Saudi Arabia with a market cap of SAR4.63 billion.

Operations: Perfect Presentation for Commercial Services Company (SASE:7204) generates revenue from Management Services (SAR70.60 million), Call Centre Services (SAR312.70 million), Operation and Maintenance Services (SAR376.09 million), and Software Licenses and Development Services (SAR398.64 million).

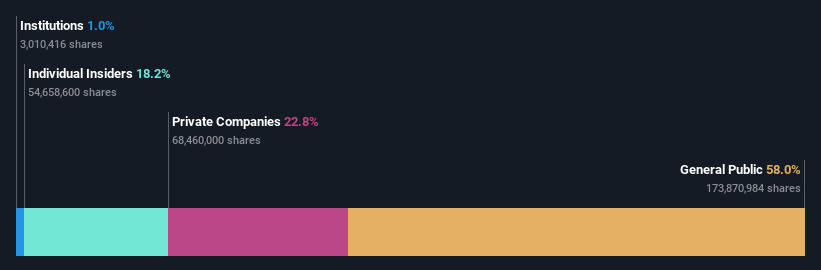

Insider Ownership: 18.2%

Return On Equity Forecast: 35% (2027 estimate)

Perfect Presentation for Commercial Services has shown strong earnings growth, with a 24.1% annual increase over the past five years and is expected to grow at 20.34% per year. Recent Q2 results reported sales of SAR 287.14 million and net income of SAR 58.77 million, both up from the previous year. The company also secured significant contracts, including a SAR 51.74 million project with Prince Muhammad bin Abdulaziz Hospital in Riyadh, positively impacting future financials through 2027.

- Take a closer look at Perfect Presentation for Commercial Services' potential here in our earnings growth report.

- The analysis detailed in our Perfect Presentation for Commercial Services valuation report hints at an inflated share price compared to its estimated value.

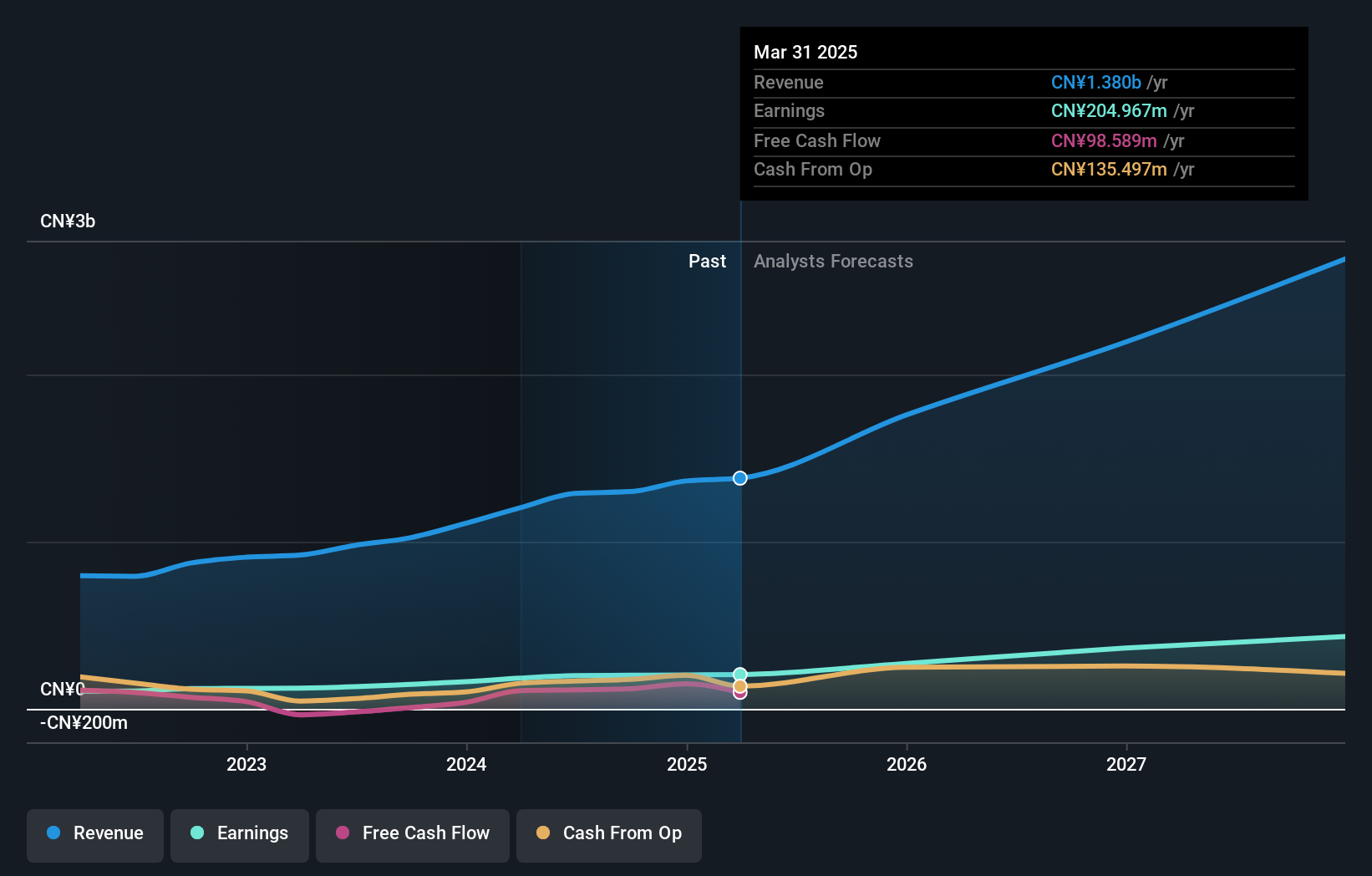

Sichuan Chuanhuan TechnologyLtd (SZSE:300547)

Simply Wall St Growth Rating: ★★★★★★

Overview: Sichuan Chuanhuan Technology Ltd (SZSE:300547) specializes in the research, development, production, and sale of automotive rubber hose series products in China and has a market cap of CN¥2.96 billion.

Operations: Revenue from non-tire rubber products amounts to CN¥1.20 billion.

Insider Ownership: 33.9%

Return On Equity Forecast: 21% (2027 estimate)

Sichuan Chuanhuan Technology Ltd. presents a compelling growth story with its earnings forecast to grow at 24.1% annually, outpacing the CN market's 22%. The company's revenue is also expected to increase by 23.3% per year, surpassing the market average of 13.4%. Despite a highly volatile share price and an unstable dividend track record, it trades at a good value with a Price-To-Earnings ratio of 18.8x compared to the CN market's 26.1x.

- Get an in-depth perspective on Sichuan Chuanhuan TechnologyLtd's performance by reading our analyst estimates report here.

- Our expertly prepared valuation report Sichuan Chuanhuan TechnologyLtd implies its share price may be lower than expected.

Turning Ideas Into Actions

- Click this link to deep-dive into the 1496 companies within our Fast Growing Companies With High Insider Ownership screener.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300547

Sichuan Chuanhuan TechnologyLtd

Engages in the research, development, production, and sale of automotive rubber hose series products in China.

Flawless balance sheet with solid track record.