Advertisement

- China

- /

- Auto Components

- /

- SZSE:300473

Exploring Three Promising Stocks with Strong Potential

Simply Wall St

Reviewed by Simply Wall St

In a week marked by cautious sentiment following the Federal Reserve's rate cuts and hawkish forecasts, global markets experienced notable declines, with smaller-cap indexes like the S&P 600 facing particular pressure. As investors navigate these turbulent waters, identifying stocks with strong fundamentals and growth potential becomes crucial for those seeking resilience amid economic uncertainties.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Lion Rock Group | 16.91% | 14.33% | 10.15% | ★★★★★★ |

| PW Medtech Group | 0.06% | 22.33% | -17.56% | ★★★★★★ |

| E-Commodities Holdings | 21.33% | 9.04% | 28.46% | ★★★★★★ |

| Natural Food International Holding | NA | 2.49% | 20.35% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| Lee's Pharmaceutical Holdings | 14.22% | -1.39% | -14.93% | ★★★★★☆ |

| Baoding Technology | 64.72% | 34.64% | 46.42% | ★★★★☆☆ |

| A2B Australia | 15.83% | -7.78% | 25.44% | ★★★★☆☆ |

| Time Interconnect Technology | 151.14% | 24.74% | 19.78% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

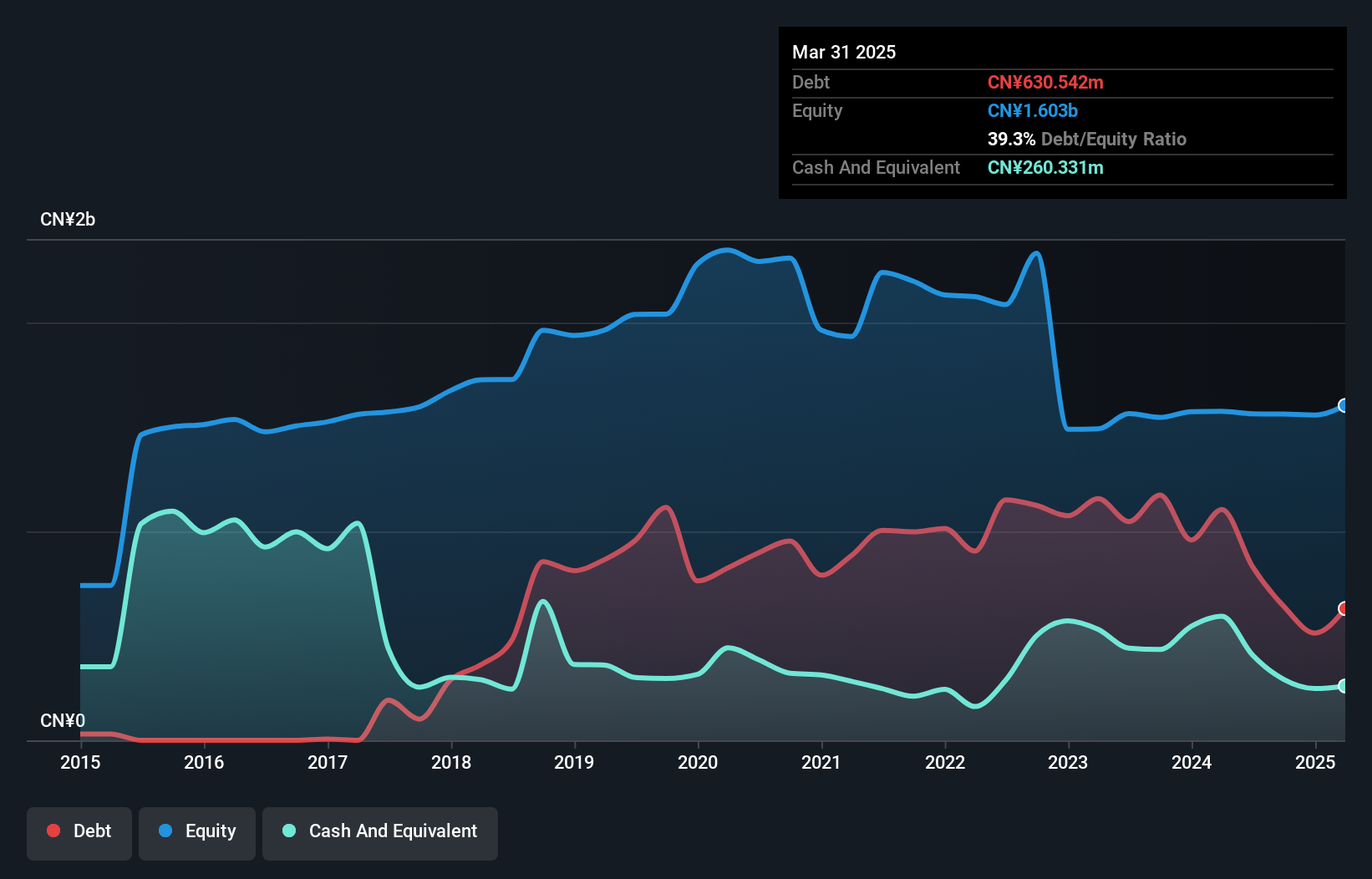

Fuxin Dare Automotive Parts (SZSE:300473)

Simply Wall St Value Rating: ★★★★★☆

Overview: Fuxin Dare Automotive Parts Co., Ltd. focuses on the research, development, manufacture, and sale of automotive components both in China and internationally, with a market cap of CN¥3.65 billion.

Operations: The company generates revenue primarily through the sale of automotive components. A notable aspect of its financial performance is the trend in gross profit margin, which has shown variability over recent periods.

Fuxin Dare Automotive Parts is carving out its niche in the auto components sector, having recently turned profitable. The company is trading at 76.1% below its estimated fair value, suggesting potential undervaluation. Over the past five years, Fuxin Dare has effectively reduced its debt to equity ratio from 54.6% to 41.1%, with a satisfactory net debt to equity ratio of 22.4%. Despite high-quality earnings and positive free cash flow, interest coverage remains a challenge at just 1.5 times EBIT, indicating room for improvement in financial health management as it navigates market volatility and growth opportunities.

- Click here to discover the nuances of Fuxin Dare Automotive Parts with our detailed analytical health report.

Gain insights into Fuxin Dare Automotive Parts' past trends and performance with our Past report.

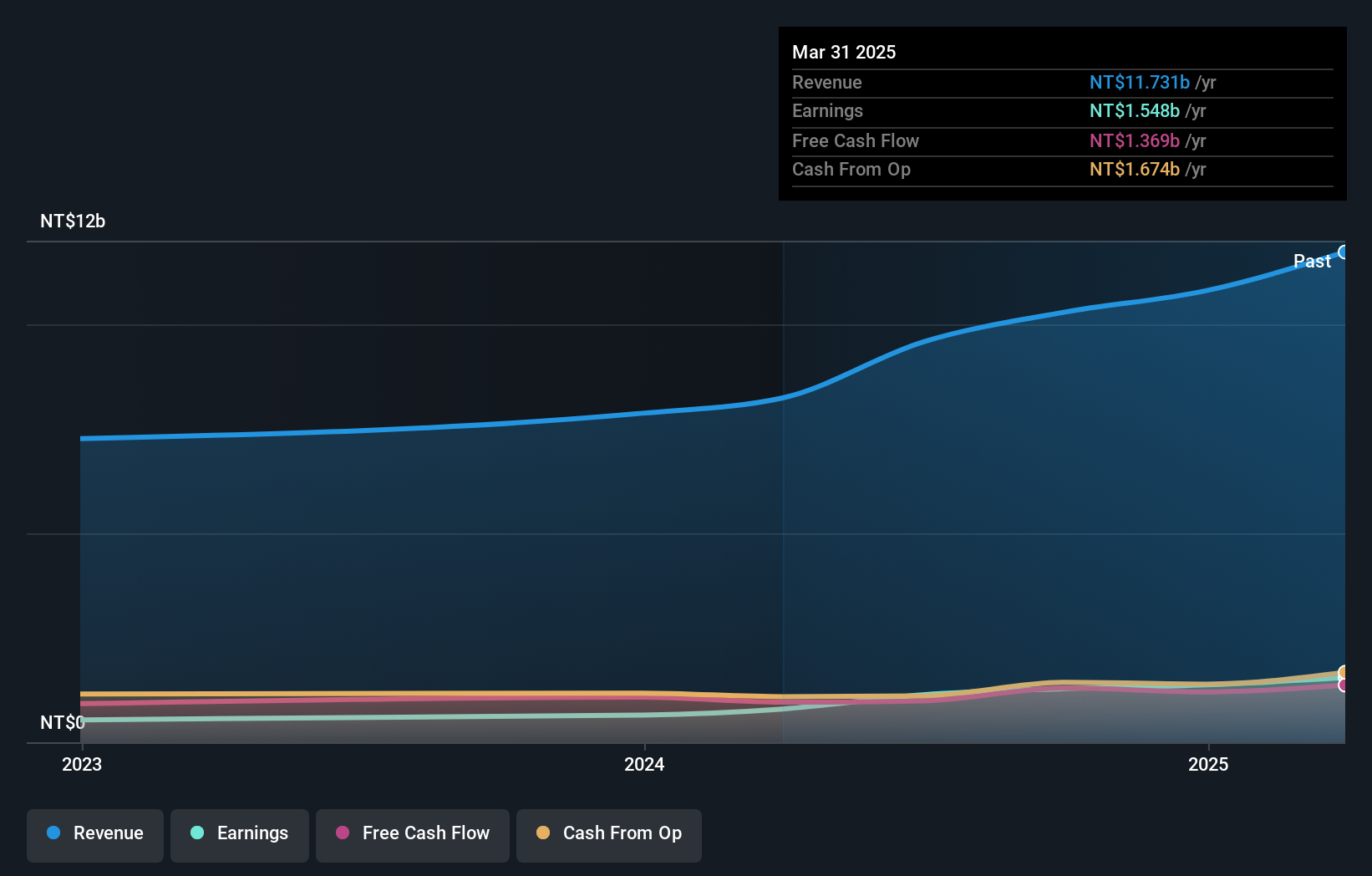

Syntec Technology (TPEX:7750)

Simply Wall St Value Rating: ★★★★★☆

Overview: Syntec Technology Co., Ltd. manufactures PC-based digital controllers specializing in machine tools, with a market capitalization of NT$31.39 billion.

Operations: Syntec Technology generates revenue primarily from the Machinery & Industrial Equipment segment, amounting to NT$9.58 billion.

Earnings for Syntec Technology soared by 91% over the past year, significantly outpacing the Machinery industry's 15% growth. The company exhibits robust financial health with interest payments on its debt well-covered at 86 times by EBIT, indicating strong operational efficiency. Syntec's profitability ensures a stable cash runway, while its cash position surpasses total debt levels. Recent inclusion in the S&P Global BMI Index highlights growing recognition in financial markets. Despite insufficient data on long-term debt reduction trends, high-quality earnings and positive free cash flow underscore Syntec's potential as an attractive investment prospect.

- Delve into the full analysis health report here for a deeper understanding of Syntec Technology.

Understand Syntec Technology's track record by examining our Past report.

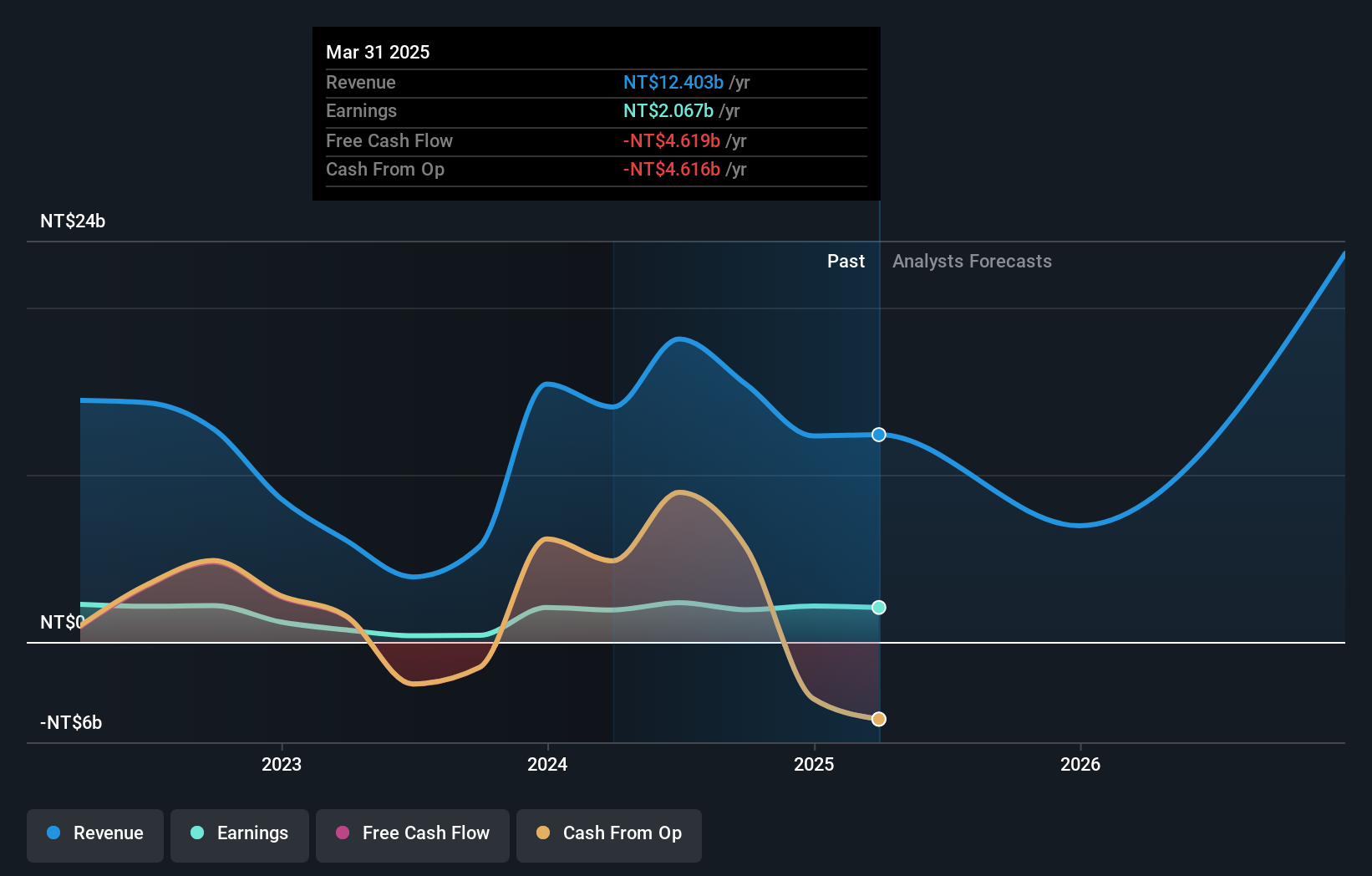

Da-Li DevelopmentLtd (TWSE:6177)

Simply Wall St Value Rating: ★★★★★☆

Overview: Da-Li Development Co., Ltd., along with its subsidiaries, engages in the construction business in Taiwan and the United States, with a market capitalization of NT$18.68 billion.

Operations: Da-Li Development generates revenue primarily from its Construction Department and Construction Segment, with figures amounting to NT$14.61 billion and NT$4.36 billion, respectively. The company experiences financial adjustments and write-offs totaling -NT$3.77 billion.

Da-Li Development, a notable player in the real estate sector, has shown impressive earnings growth of 388.5% over the past year, outpacing its industry peers. Despite this growth, the company faces challenges with a high net debt to equity ratio of 215.8%, although it has improved from 282.8% five years ago. Recently reported earnings for Q3 revealed sales at TWD 568.87 million compared to TWD 3,293.31 million last year and net income at TWD 11.65 million versus TWD 430.07 million previously, reflecting significant shifts in financial performance amidst ongoing business expansions like their joint land acquisition in Taipei City valued at approximately TWD 5.75 billion.

- Dive into the specifics of Da-Li DevelopmentLtd here with our thorough health report.

Evaluate Da-Li DevelopmentLtd's historical performance by accessing our past performance report.

Key Takeaways

- Navigate through the entire inventory of 4620 Undiscovered Gems With Strong Fundamentals here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300473

Fuxin Dare Automotive Parts

Engages in the research, development, manufacture, and sale of automotive components in China and internationally.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor