Advertisement

- China

- /

- Auto Components

- /

- SZSE:002920

Here's Why Huizhou Desay SV Automotive (SZSE:002920) Can Manage Its Debt Responsibly

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Huizhou Desay SV Automotive Co., Ltd. (SZSE:002920) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

Check out our latest analysis for Huizhou Desay SV Automotive

What Is Huizhou Desay SV Automotive's Debt?

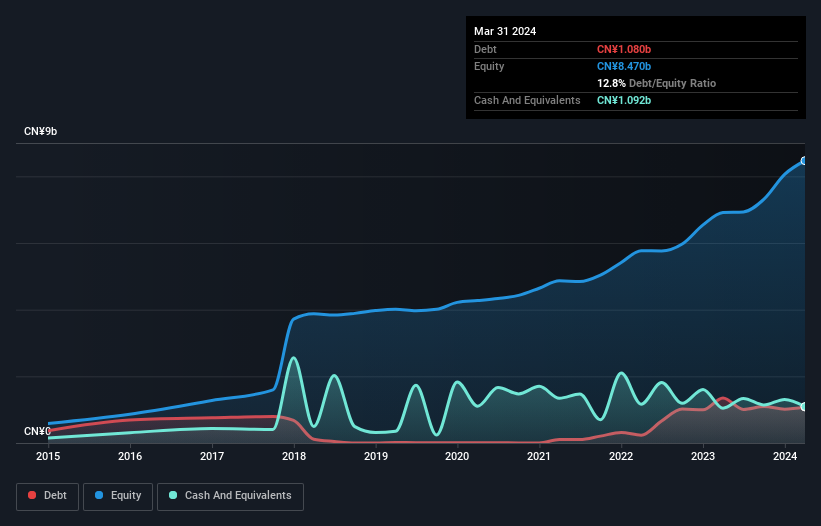

As you can see below, Huizhou Desay SV Automotive had CN¥1.08b of debt at March 2024, down from CN¥1.35b a year prior. However, it does have CN¥1.09b in cash offsetting this, leading to net cash of CN¥12.5m.

A Look At Huizhou Desay SV Automotive's Liabilities

We can see from the most recent balance sheet that Huizhou Desay SV Automotive had liabilities of CN¥8.78b falling due within a year, and liabilities of CN¥1.23b due beyond that. On the other hand, it had cash of CN¥1.09b and CN¥8.49b worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by CN¥429.0m.

This state of affairs indicates that Huizhou Desay SV Automotive's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the CN¥50.2b company is short on cash, but still worth keeping an eye on the balance sheet. Despite its noteworthy liabilities, Huizhou Desay SV Automotive boasts net cash, so it's fair to say it does not have a heavy debt load!

In addition to that, we're happy to report that Huizhou Desay SV Automotive has boosted its EBIT by 45%, thus reducing the spectre of future debt repayments. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Huizhou Desay SV Automotive can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. Huizhou Desay SV Automotive may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Over the last three years, Huizhou Desay SV Automotive recorded negative free cash flow, in total. Debt is usually more expensive, and almost always more risky in the hands of a company with negative free cash flow. Shareholders ought to hope for an improvement.

Summing Up

While it is always sensible to look at a company's total liabilities, it is very reassuring that Huizhou Desay SV Automotive has CN¥12.5m in net cash. And we liked the look of last year's 45% year-on-year EBIT growth. So we don't have any problem with Huizhou Desay SV Automotive's use of debt. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For instance, we've identified 2 warning signs for Huizhou Desay SV Automotive (1 is potentially serious) you should be aware of.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Huizhou Desay SV Automotive might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SZSE:002920

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|31.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|24.4% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|13.5% overvalued

DA

Community Contributor