As global markets navigate a landscape marked by volatile corporate earnings and competitive pressures in the AI sector, investors are closely watching central bank policies and economic indicators for signs of stability. Amidst this backdrop, stocks with high insider ownership can offer unique insights into potential growth opportunities, as insiders often have a deep understanding of their companies' prospects and challenges.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| Seojin SystemLtd (KOSDAQ:A178320) | 32.1% | 39.9% |

| Archean Chemical Industries (NSEI:ACI) | 22.9% | 41.2% |

| Clinuvel Pharmaceuticals (ASX:CUV) | 10.4% | 26.2% |

| SKS Technologies Group (ASX:SKS) | 29.7% | 24.8% |

| Laopu Gold (SEHK:6181) | 36.4% | 36.9% |

| Medley (TSE:4480) | 34.1% | 27.3% |

| Plenti Group (ASX:PLT) | 12.7% | 120.1% |

| Fine M-TecLTD (KOSDAQ:A441270) | 17.1% | 135% |

| HANA Micron (KOSDAQ:A067310) | 18.3% | 119.4% |

| Brightstar Resources (ASX:BTR) | 16.2% | 86% |

Underneath we present a selection of stocks filtered out by our screen.

Ningbo Jifeng Auto Parts (SHSE:603997)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Ningbo Jifeng Auto Parts Co., Ltd. manufactures automotive interior parts in China and has a market cap of CN¥15.65 billion.

Operations: The company's revenue segments include the production and sale of automotive interior components in China.

Insider Ownership: 25.7%

Revenue Growth Forecast: 16.1% p.a.

Ningbo Jifeng Auto Parts is trading at 64.1% below its estimated fair value, presenting a good relative value compared to peers. The company is expected to achieve revenue growth of 16.1% annually, outpacing the Chinese market's average growth rate. Earnings are forecasted to grow significantly by 112.94% per year, with profitability anticipated within three years—an above-average market performance expectation. No substantial insider trading activity has been reported recently.

- Click to explore a detailed breakdown of our findings in Ningbo Jifeng Auto Parts' earnings growth report.

- Our expertly prepared valuation report Ningbo Jifeng Auto Parts implies its share price may be lower than expected.

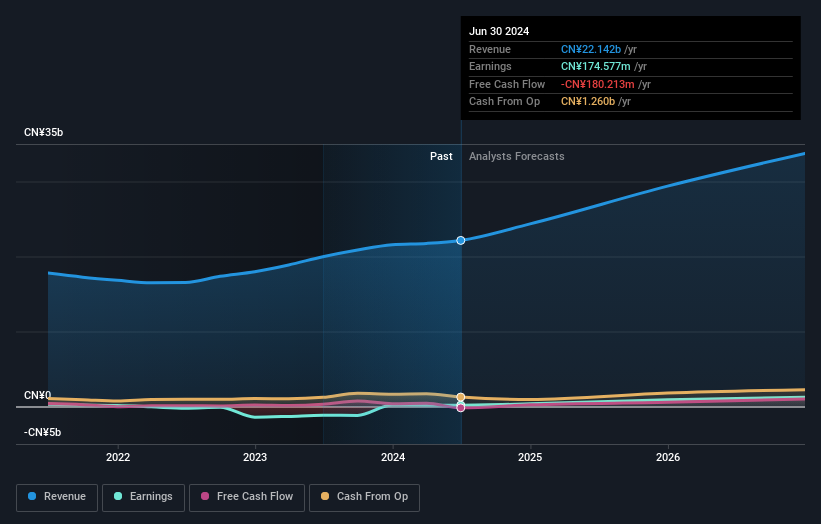

Shanghai Suochen Information TechnologyLtd (SHSE:688507)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Shanghai Suochen Information Technology Ltd (ticker: SHSE:688507) operates in the technology sector and has a market capitalization of CN¥6.14 billion.

Operations: Shanghai Suochen Information Technology Ltd (ticker: SHSE:688507) operates in the technology sector with a market capitalization of CN¥6.14 billion.

Insider Ownership: 26.9%

Revenue Growth Forecast: 35.3% p.a.

Shanghai Suochen Information Technology is anticipated to experience robust revenue growth of 35.3% annually, surpassing the Chinese market average. Despite this, the company's profit margins have decreased from 23% last year to 6.8%. Recent buybacks amounted to CNY 50.5 million for a total of 693,511 shares repurchased, indicating strong insider confidence but no substantial recent insider trading activity was noted. Earnings are expected to grow significantly at 55.8% per year despite low forecasted return on equity and high share price volatility recently impacting investor sentiment.

- Dive into the specifics of Shanghai Suochen Information TechnologyLtd here with our thorough growth forecast report.

- The valuation report we've compiled suggests that Shanghai Suochen Information TechnologyLtd's current price could be inflated.

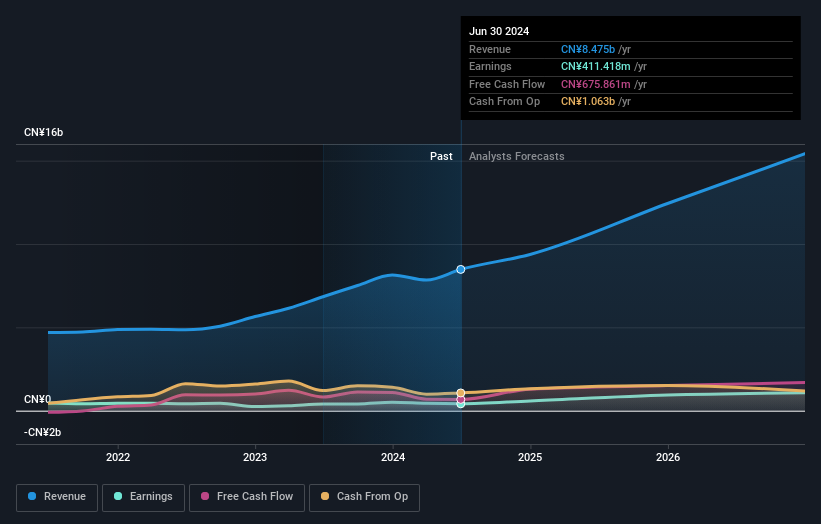

Kehua Data (SZSE:002335)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kehua Data Co., Ltd. offers integrated solutions for power protection and energy conservation globally, with a market cap of CN¥13.93 billion.

Operations: Kehua Data's revenue is derived from providing integrated solutions for power protection and energy conservation worldwide.

Insider Ownership: 21.5%

Revenue Growth Forecast: 18% p.a.

Kehua Data is positioned for significant earnings growth of 42.5% annually, outpacing the Chinese market's 25.1%. Despite a volatile share price and declining profit margins from 5.4% to 3.7%, the stock trades at a substantial discount of 34.5% below its estimated fair value, offering potential value for investors. Revenue is projected to grow at 18% per year, faster than the market average but below high-growth thresholds, with no recent insider trading activity noted.

- Unlock comprehensive insights into our analysis of Kehua Data stock in this growth report.

- According our valuation report, there's an indication that Kehua Data's share price might be on the expensive side.

Where To Now?

- Dive into all 1471 of the Fast Growing Companies With High Insider Ownership we have identified here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688507

Shanghai Suochen Information TechnologyLtd

Shanghai Suochen Information Technology Ltd.

High growth potential with mediocre balance sheet.

Market Insights

Community Narratives