Advertisement

- China

- /

- Auto Components

- /

- SHSE:603767

Zhejiang Zomax Transmission Co., Ltd. (SHSE:603767) Stock Rockets 35% As Investors Are Less Pessimistic Than Expected

Zhejiang Zomax Transmission Co., Ltd. (SHSE:603767) shareholders would be excited to see that the share price has had a great month, posting a 35% gain and recovering from prior weakness. The last month tops off a massive increase of 112% in the last year.

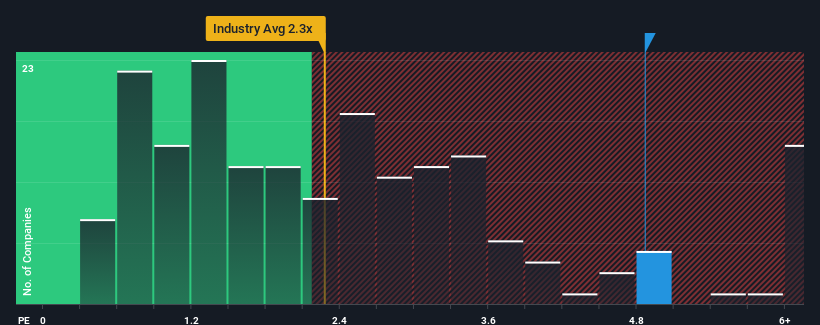

Since its price has surged higher, given around half the companies in China's Auto Components industry have price-to-sales ratios (or "P/S") below 2.3x, you may consider Zhejiang Zomax Transmission as a stock to avoid entirely with its 4.9x P/S ratio. However, the P/S might be quite high for a reason and it requires further investigation to determine if it's justified.

View our latest analysis for Zhejiang Zomax Transmission

How Has Zhejiang Zomax Transmission Performed Recently?

It looks like revenue growth has deserted Zhejiang Zomax Transmission recently, which is not something to boast about. Perhaps the market believes that revenue growth will improve markedly over current levels, inflating the P/S ratio. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Zhejiang Zomax Transmission's earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Zhejiang Zomax Transmission?

Zhejiang Zomax Transmission's P/S ratio would be typical for a company that's expected to deliver very strong growth, and importantly, perform much better than the industry.

If we review the last year of revenue, the company posted a result that saw barely any deviation from a year ago. The longer-term trend has been no better as the company has no revenue growth to show for over the last three years either. So it seems apparent to us that the company has struggled to grow revenue meaningfully over that time.

Comparing that to the industry, which is predicted to deliver 26% growth in the next 12 months, the company's momentum is weaker, based on recent medium-term annualised revenue results.

With this information, we find it concerning that Zhejiang Zomax Transmission is trading at a P/S higher than the industry. It seems most investors are ignoring the fairly limited recent growth rates and are hoping for a turnaround in the company's business prospects. There's a good chance existing shareholders are setting themselves up for future disappointment if the P/S falls to levels more in line with recent growth rates.

The Final Word

Shares in Zhejiang Zomax Transmission have seen a strong upwards swing lately, which has really helped boost its P/S figure. Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

The fact that Zhejiang Zomax Transmission currently trades on a higher P/S relative to the industry is an oddity, since its recent three-year growth is lower than the wider industry forecast. When we see slower than industry revenue growth but an elevated P/S, there's considerable risk of the share price declining, sending the P/S lower. Unless there is a significant improvement in the company's medium-term performance, it will be difficult to prevent the P/S ratio from declining to a more reasonable level.

Having said that, be aware Zhejiang Zomax Transmission is showing 3 warning signs in our investment analysis, and 2 of those are potentially serious.

If you're unsure about the strength of Zhejiang Zomax Transmission's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Zomax Transmission might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SHSE:603767

Zhejiang Zomax Transmission

Engages in the research and development, production, and sale of automotive transmissions and vehicle gears in China and internationally.

Flawless balance sheet slight.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|48.9% undervalued

TO

Community Contributor