Advertisement

- Chile

- /

- Wireless Telecom

- /

- SNSE:ENTEL

Is Empresa Nacional de Telecomunicaciones (SNSE:ENTEL) Using Too Much Debt?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Empresa Nacional de Telecomunicaciones S.A. (SNSE:ENTEL) does have debt on its balance sheet. But is this debt a concern to shareholders?

When Is Debt A Problem?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Empresa Nacional de Telecomunicaciones

How Much Debt Does Empresa Nacional de Telecomunicaciones Carry?

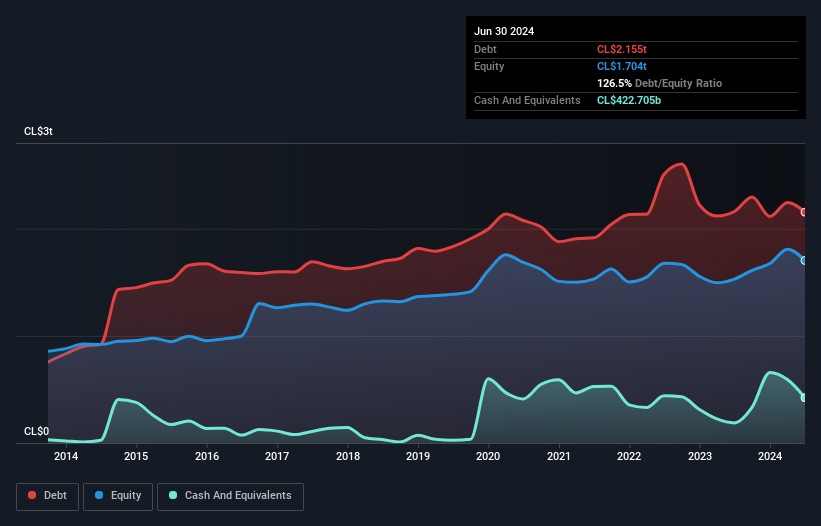

The chart below, which you can click on for greater detail, shows that Empresa Nacional de Telecomunicaciones had CL$2.15t in debt in June 2024; about the same as the year before. However, it does have CL$422.7b in cash offsetting this, leading to net debt of about CL$1.73t.

How Healthy Is Empresa Nacional de Telecomunicaciones' Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Empresa Nacional de Telecomunicaciones had liabilities of CL$1.23t due within 12 months and liabilities of CL$2.79t due beyond that. On the other hand, it had cash of CL$422.7b and CL$649.8b worth of receivables due within a year. So its liabilities total CL$2.95t more than the combination of its cash and short-term receivables.

The deficiency here weighs heavily on the CL$916.4b company itself, as if a child were struggling under the weight of an enormous back-pack full of books, his sports gear, and a trumpet. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Empresa Nacional de Telecomunicaciones would probably need a major re-capitalization if its creditors were to demand repayment.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Empresa Nacional de Telecomunicaciones's debt is 3.1 times its EBITDA, and its EBIT cover its interest expense 4.5 times over. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Importantly, Empresa Nacional de Telecomunicaciones grew its EBIT by 56% over the last twelve months, and that growth will make it easier to handle its debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Empresa Nacional de Telecomunicaciones can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. During the last three years, Empresa Nacional de Telecomunicaciones generated free cash flow amounting to a very robust 85% of its EBIT, more than we'd expect. That puts it in a very strong position to pay down debt.

Our View

While Empresa Nacional de Telecomunicaciones's level of total liabilities has us nervous. To wit both its conversion of EBIT to free cash flow and EBIT growth rate were encouraging signs. Looking at all the angles mentioned above, it does seem to us that Empresa Nacional de Telecomunicaciones is a somewhat risky investment as a result of its debt. That's not necessarily a bad thing, since leverage can boost returns on equity, but it is something to be aware of. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 5 warning signs for Empresa Nacional de Telecomunicaciones that you should be aware of before investing here.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

Valuation is complex, but we're here to simplify it.

Discover if Empresa Nacional de Telecomunicaciones might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SNSE:ENTEL

Empresa Nacional de Telecomunicaciones

Empresa Nacional de Telecomunicaciones S.A.

Good value with proven track record.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor