Advertisement

How Financially Strong Is Comet Holding AG (VTX:COTN)?

While small-cap stocks, such as Comet Holding AG (VTX:COTN) with its market cap of CHF714m, are popular for their explosive growth, investors should also be aware of their balance sheet to judge whether the company can survive a downturn. Evaluating financial health as part of your investment thesis is crucial, since poor capital management may bring about bankruptcies, which occur at a higher rate for small-caps. We'll look at some basic checks that can form a snapshot the company’s financial strength. However, this is not a comprehensive overview, so I recommend you dig deeper yourself into COTN here.

Does COTN Produce Much Cash Relative To Its Debt?

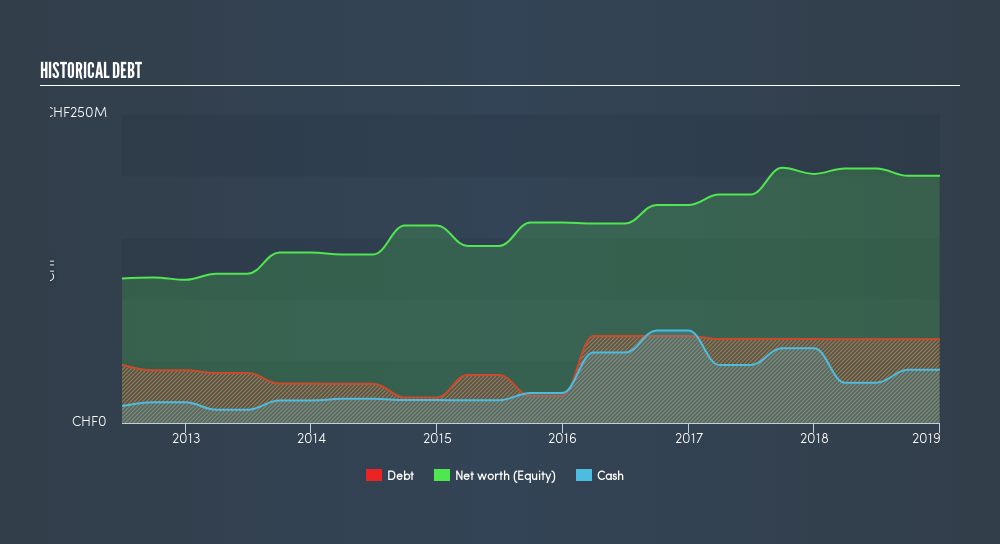

Over the past year, COTN has maintained its debt levels at around CHF68m – this includes long-term debt. At this constant level of debt, COTN's cash and short-term investments stands at CHF43m , ready to be used for running the business. On top of this, COTN has generated cash from operations of CHF22m over the same time period, leading to an operating cash to total debt ratio of 33%, signalling that COTN’s current level of operating cash is high enough to cover debt.

Can COTN pay its short-term liabilities?

With current liabilities at CHF94m, the company has been able to meet these obligations given the level of current assets of CHF206m, with a current ratio of 2.2x. The current ratio is the number you get when you divide current assets by current liabilities. For Electronic companies, this ratio is within a sensible range since there is a bit of a cash buffer without leaving too much capital in a low-return environment.

Is COTN’s debt level acceptable?

With debt at 34% of equity, COTN may be thought of as appropriately levered. This range is considered safe as COTN is not taking on too much debt obligation, which can be restrictive and risky for equity-holders. We can check to see whether COTN is able to meet its debt obligations by looking at the net interest coverage ratio. A company generating earnings before interest and tax (EBIT) at least three times its net interest payments is considered financially sound. In COTN's, case, the ratio of 35.65x suggests that interest is comfortably covered, which means that debtors may be willing to loan the company more money, giving COTN ample headroom to grow its debt facilities.

Next Steps:

COTN’s debt level is appropriate for a company its size, and it is also able to generate sufficient cash flow coverage, meaning it has been able to put its debt in good use. Furthermore, the company exhibits proper management of current assets and upcoming liabilities. Keep in mind I haven't considered other factors such as how COTN has been performing in the past. I recommend you continue to research Comet Holding to get a better picture of the stock by looking at:

- Future Outlook: What are well-informed industry analysts predicting for COTN’s future growth? Take a look at our free research report of analyst consensus for COTN’s outlook.

- Valuation: What is COTN worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether COTN is currently mispriced by the market.

- Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SWX:COTN

Comet Holding

Provides X-ray and radio frequency (RF) power technology solutions in Europe, North America, Asia, and internationally.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor