Advertisement

- Switzerland

- /

- Hospitality

- /

- SWX:LMN

One Forecaster Is Now More Bearish On lastminute.com N.V. (VTX:LMN) Than They Used To Be

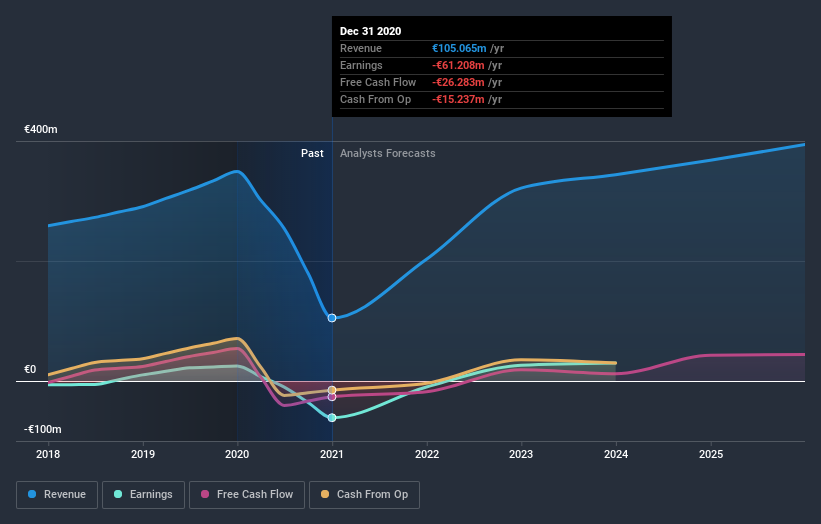

The latest analyst coverage could presage a bad day for lastminute.com N.V. (VTX:LMN), with the covering analyst making across-the-board cuts to their statutory estimates that might leave shareholders a little shell-shocked. Both revenue and earnings per share (EPS) forecasts went under the knife, suggesting the analyst has soured majorly on the business. Bidders are definitely seeing a different story, with the stock price of CHF38.80 reflecting a 15% rise in the past week. It will be interesting to see if the downgrade has an impact on buying demand for the company's shares.

After this downgrade, lastminute.com's lone analyst is now forecasting revenues of €203m in 2021. This would be a sizeable 93% improvement in sales compared to the last 12 months. The loss per share is anticipated to greatly reduce in the near future, narrowing 84% to €0.92. Previously, the analyst had been modelling revenues of €229m and earnings per share (EPS) of €0.77 in 2021. There looks to have been a major change in sentiment regarding lastminute.com's prospects, with a substantial drop in revenues and the analyst now forecasting a loss instead of a profit.

Check out our latest analysis for lastminute.com

The consensus price target lifted 37% to €37.96, clearly signalling that the weaker revenue and EPS outlook are not expected to weigh on the stock over the longer term.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. One thing stands out from these estimates, which is that lastminute.com is forecast to grow faster in the future than it has in the past, with revenues expected to display 93% annualised growth until the end of 2021. If achieved, this would be a much better result than the 1.1% annual decline over the past five years. Compare this against analyst estimates for the broader industry, which suggest that (in aggregate) industry revenues are expected to grow 21% annually. So it looks like lastminute.com is expected to grow faster than its competitors, at least for a while.

The Bottom Line

The most important thing to take away is that the analyst is expecting lastminute.com to become unprofitable this year. While the analyst did downgrade their revenue estimates, these forecasts still imply revenues will perform better than the wider market. The rising price target is a puzzle, but still - with a serious cut to this year's outlook, we wouldn't be surprised if investors were a bit wary of lastminute.com.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At least one analyst has provided forecasts out to 2025, which can be seen for free on our platform here.

Another way to search for interesting companies that could be reaching an inflection point is to track whether management are buying or selling, with our free list of growing companies that insiders are buying.

If you decide to trade lastminute.com, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if lastminute.com might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SWX:LMN

lastminute.com

Operates in the online travel industry providing dynamic holiday packages in Italy, Spain, the United Kingdom, France, Germany, and internationally.

Undervalued with high growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CE

cementafriend on Constellation Energy ·

Constellation Energy Dividends and Growth

Fair Value:US$348.054.7% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KH

Khagani on CoreWeave ·

CoreWeave's Revenue Expected to Rocket 77.88% in 5-Year Forecast

Fair Value:US$11033.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PO

PortfolioPlus on Bisalloy Steel Group ·

Bisalloy Steel Group will shine with a projected profit margin increase of 12.8%

Fair Value:AU$6.7118.0% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

935 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

140 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative