Advertisement

- Switzerland

- /

- Real Estate

- /

- SWX:MOBN

Mobimo Holding AG's (VTX:MOBN) Financial Prospects Don't Look Very Positive: Could It Mean A Stock Price Drop In The Future?

Mobimo Holding's (VTX:MOBN) stock up by 5.0% over the past three months. However, in this article, we decided to focus on its weak financials, as long-term fundamentals ultimately dictate market outcomes. Specifically, we decided to study Mobimo Holding's ROE in this article.

Return on equity or ROE is an important factor to be considered by a shareholder because it tells them how effectively their capital is being reinvested. In simpler terms, it measures the profitability of a company in relation to shareholder's equity.

How Do You Calculate Return On Equity?

The formula for return on equity is:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Mobimo Holding is:

6.5% = CHF125m ÷ CHF1.9b (Based on the trailing twelve months to December 2024).

The 'return' is the income the business earned over the last year. That means that for every CHF1 worth of shareholders' equity, the company generated CHF0.07 in profit.

Check out our latest analysis for Mobimo Holding

What Has ROE Got To Do With Earnings Growth?

We have already established that ROE serves as an efficient profit-generating gauge for a company's future earnings. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Mobimo Holding's Earnings Growth And 6.5% ROE

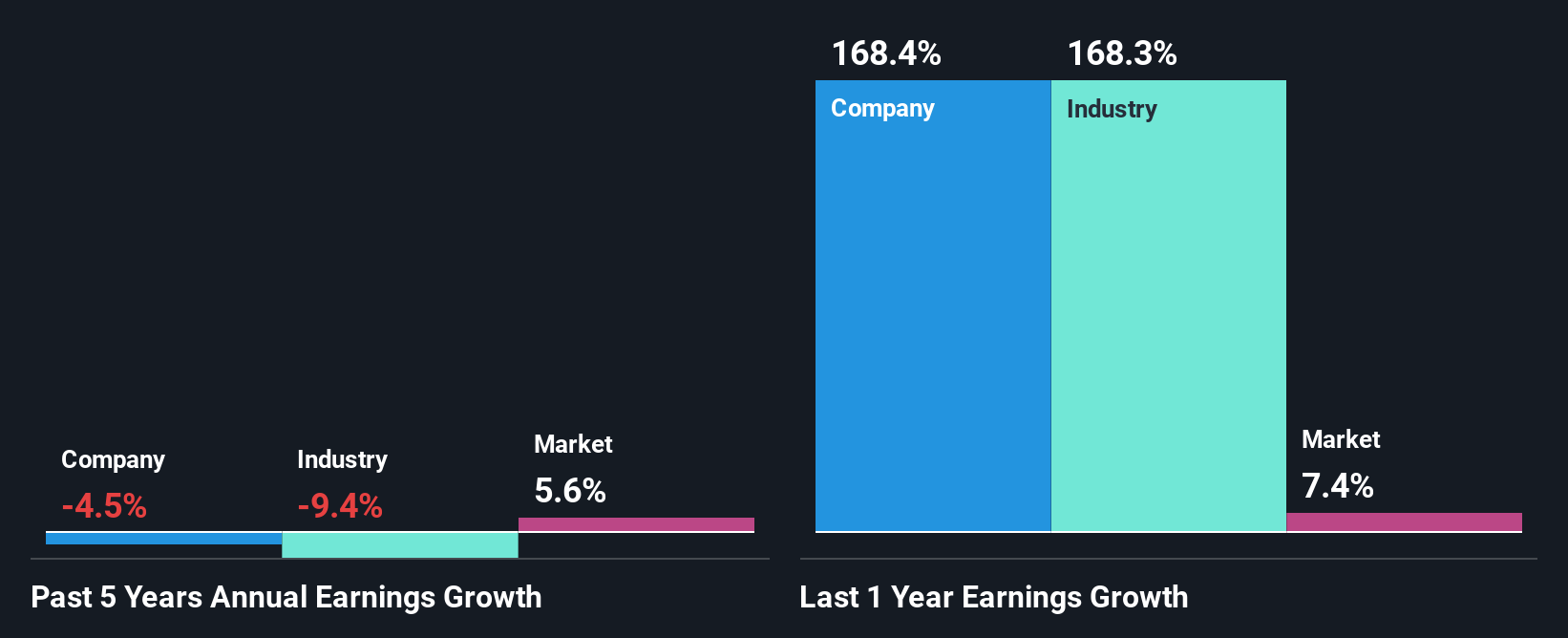

At first glance, Mobimo Holding's ROE doesn't look very promising. Yet, a closer study shows that the company's ROE is similar to the industry average of 6.3%. But Mobimo Holding saw a five year net income decline of 4.5% over the past five years. Remember, the company's ROE is a bit low to begin with. Hence, this goes some way in explaining the shrinking earnings.

Next, we compared Mobimo Holding's performance against the industry and found that the industry shrunk its earnings at 9.4% in the same period, which suggests that the company's earnings have been shrinking at a slower rate than its industry, While this is not particularly good, its not particularly bad either.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. One good indicator of expected earnings growth is the P/E ratio which determines the price the market is willing to pay for a stock based on its earnings prospects. So, you may want to check if Mobimo Holding is trading on a high P/E or a low P/E, relative to its industry.

Is Mobimo Holding Making Efficient Use Of Its Profits?

Mobimo Holding's declining earnings is not surprising given how the company is spending most of its profits in paying dividends, judging by its three-year median payout ratio of 60% (or a retention ratio of 40%). With only very little left to reinvest into the business, growth in earnings is far from likely. To know the 3 risks we have identified for Mobimo Holding visit our risks dashboard for free.

In addition, Mobimo Holding has been paying dividends over a period of at least ten years suggesting that keeping up dividend payments is way more important to the management even if it comes at the cost of business growth. Upon studying the latest analysts' consensus data, we found that the company's future payout ratio is expected to rise to 75% over the next three years. Accordingly, the expected increase in the payout ratio explains the expected decline in the company's ROE to 5.0%, over the same period.

Conclusion

On the whole, Mobimo Holding's performance is quite a big let-down. The company has seen a lack of earnings growth as a result of retaining very little profits and whatever little it does retain, is being reinvested at a very low rate of return. Further, on studying current analyst estimates, we found that the company's earnings growth is expected to be pretty much the same. To know more about the latest analysts predictions for the company, check out this visualization of analyst forecasts for the company.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:MOBN

Mobimo Holding

Engages in the buying, planning, building, maintenance, and sale of real estate properties to private individuals, institutional investors, and companies in Switzerland.

Established dividend payer with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets