Advertisement

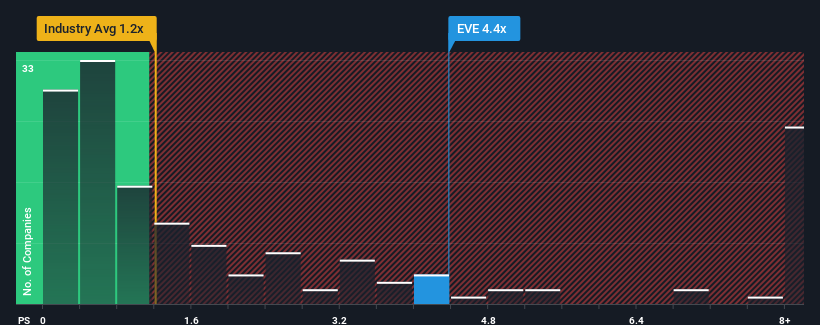

There wouldn't be many who think Evolva Holding SA's (VTX:EVE) price-to-sales (or "P/S") ratio of 4.4x is worth a mention when the median P/S for the Chemicals industry in Switzerland is similar at about 4.1x. While this might not raise any eyebrows, if the P/S ratio is not justified investors could be missing out on a potential opportunity or ignoring looming disappointment.

Check out our latest analysis for Evolva Holding

How Has Evolva Holding Performed Recently?

Recent times have been advantageous for Evolva Holding as its revenues have been rising faster than most other companies. One possibility is that the P/S ratio is moderate because investors think this strong revenue performance might be about to tail off. If the company manages to stay the course, then investors should be rewarded with a share price that matches its revenue figures.

Want the full picture on analyst estimates for the company? Then our free report on Evolva Holding will help you uncover what's on the horizon.How Is Evolva Holding's Revenue Growth Trending?

The only time you'd be comfortable seeing a P/S like Evolva Holding's is when the company's growth is tracking the industry closely.

Taking a look back first, we see that the company grew revenue by an impressive 57% last year. The strong recent performance means it was also able to grow revenue by 34% in total over the last three years. Therefore, it's fair to say the revenue growth recently has been superb for the company.

Turning to the outlook, the next three years should generate growth of 46% per year as estimated by the sole analyst watching the company. Meanwhile, the rest of the industry is forecast to only expand by 7.1% per year, which is noticeably less attractive.

With this in consideration, we find it intriguing that Evolva Holding's P/S is closely matching its industry peers. It may be that most investors aren't convinced the company can achieve future growth expectations.

The Final Word

Using the price-to-sales ratio alone to determine if you should sell your stock isn't sensible, however it can be a practical guide to the company's future prospects.

Looking at Evolva Holding's analyst forecasts revealed that its superior revenue outlook isn't giving the boost to its P/S that we would've expected. Perhaps uncertainty in the revenue forecasts are what's keeping the P/S ratio consistent with the rest of the industry. It appears some are indeed anticipating revenue instability, because these conditions should normally provide a boost to the share price.

Before you take the next step, you should know about the 5 warning signs for Evolva Holding (1 is concerning!) that we have uncovered.

If these risks are making you reconsider your opinion on Evolva Holding, explore our interactive list of high quality stocks to get an idea of what else is out there.

Valuation is complex, but we're here to simplify it.

Discover if Evolva Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:EVE

Evolva Holding

Evolva Holding SA discovers, researches, develops, and commercializes nature-based ingredients for use in flavor and fragrances, health ingredients, health protection, and other sectors in Switzerland, the United States, and internationally.

Excellent balance sheet with weak fundamentals.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.2% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|25.1% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.04% overvalued

LI

Community Contributor