Advertisement

- Switzerland

- /

- Packaging

- /

- SWX:CPHN

CPH Chemie + Papier Holding AG (VTX:CPHN): Set To Experience A Decrease In Earnings?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

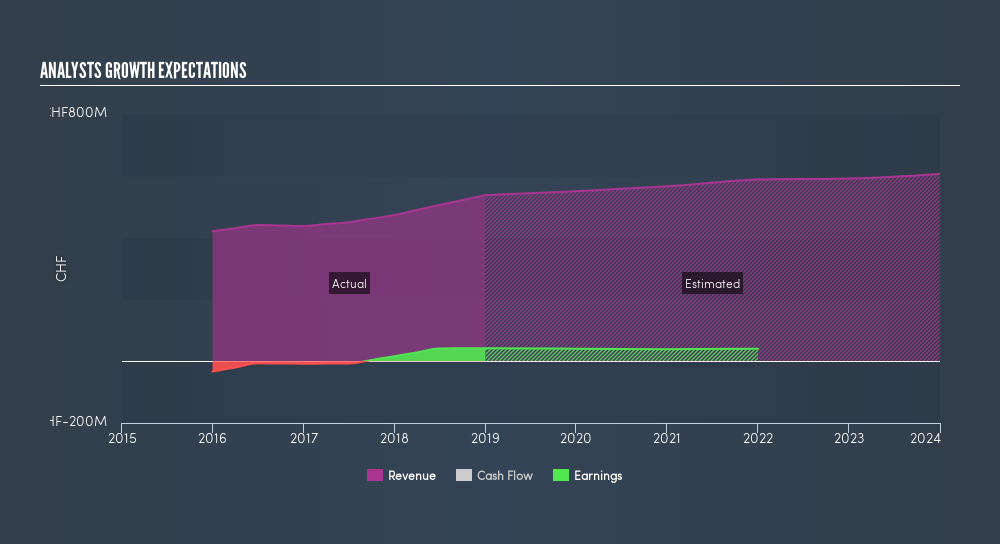

Looking at CPH Chemie + Papier Holding AG's (VTX:CPHN) earnings update in December 2018, it seems that analyst forecasts are fairly bearish, as a 4.7% fall in profits is expected in the upcoming year compared with the past 5-year average growth rate of 84%. Currently with a trailing-twelve-month profit of CHF42m, the consensus growth rate suggests that earnings will drop to CHF40m by 2020. In this article, I've outline a few earnings growth rates to give you a sense of the market sentiment for CPH Chemie + Papier Holding in the longer term. For those interested in more of an analysis of the company, you can research its fundamentals here.

See our latest analysis for CPH Chemie + Papier Holding

Can we expect CPH Chemie + Papier Holding to keep growing?

The longer term expectations from the 3 analysts of CPHN is tilted towards the negative sentiment. Since forecasting becomes more difficult further into the future, broker analysts generally project out to around three years. To reduce the year-on-year volatility of analyst earnings forecast, I've inserted a line of best fit through the expected earnings figures to determine the annual growth rate from the slope of the line.

This results in an annual growth rate of -2.1% based on the most recent earnings level of CHF42m to the final forecast of CHF40m by 2022. EPS reaches CHF6.73 in the final year of forecast compared to the current CHF7.05 EPS today. The primary reason for earnings contraction is due to cost growth exceeding top-line growth of 2.5% in the next three years. With this high cost growth, margins is expected to contract from 7.9% to 6.9% by the end of 2022.

Next Steps:

Future outlook is only one aspect when you're building an investment case for a stock. For CPH Chemie + Papier Holding, there are three essential factors you should further research:

- Financial Health: Does it have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

- Valuation: What is CPH Chemie + Papier Holding worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether CPH Chemie + Papier Holding is currently mispriced by the market.

- Other High-Growth Alternatives : Are there other high-growth stocks you could be holding instead of CPH Chemie + Papier Holding? Explore our interactive list of stocks with large growth potential to get an idea of what else is out there you may be missing!

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About SWX:CPHN

CPH Group

Develops, manufactures, and distributes chemical products and packaging solutions for pharmaceutical customers in Europe, Asia, and North and South America.

Excellent balance sheet, good value and pays a dividend.

Market Insights

Advertisement

Weekly Picks

CE

Ceazar on Sparc AI ·

When GPS fails: this small cap is fixing a $54B drone problem

Fair Value:CA$5.2533.3% undervalued

158 followersusers have followed this narrative

0 commentsusers have commented on this narrative

27 likesusers have liked this narrative

HA

HarishPK on Amdocs ·

Why Amdocs is a high conviction Buy for me?

Fair Value:US$82.0328.6% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

12 likesusers have liked this narrative

IV

Ivoed on SBM Offshore ·

Why SBM Offshore’s €30 Share Price May Be Too Harsh On Its Backlog

Fair Value:€44.527.2% undervalued

19 followersusers have followed this narrative

0 commentsusers have commented on this narrative

5 likesusers have liked this narrative

CL

Clive_Thompson on Green Tea Group ·

One of China's Fastest-Growing Restaurant Chains Trades on Just 7x Earnings and an 8% Dividend

Fair Value:HK$8.723.9% undervalued

47 followersusers have followed this narrative

3 commentsusers have commented on this narrative

20 likesusers have liked this narrative

Recently Updated Narratives

OL

OLetourneau on Texas Instruments ·

TXN — Fair Value $285

Fair Value:US$284.320.6% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

OL

OLetourneau on Otis Worldwide ·

OTIS — Fair Value $87

Fair Value:US$88.5816.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

OL

OLetourneau on Moody's ·

MCO — Fair Value $529

Fair Value:US$5299.7% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on NVIDIA ·

The company that went from selling GPUs to gamers to becoming the AI arms dealer of the 21st century.

Fair Value:US$28020.0% undervalued

279 followersusers have followed this narrative

9 commentsusers have commented on this narrative

16 likesusers have liked this narrative

CU

CubanEros on Microsoft ·

A wonderful business at reasonable price.

Fair Value:US$419.9119.1% overvalued

143 followersusers have followed this narrative

0 commentsusers have commented on this narrative

8 likesusers have liked this narrative

KI

KiwiInvest on Amazon.com ·

Amazon's high growth, high tech segments propel its profits, while traditional segments plod along

Fair Value:US$475.0942.2% undervalued

166 followersusers have followed this narrative

1 commentusers have commented on this narrative

8 likesusers have liked this narrative

Trending Discussion

YA

Yash_Upadhyaya on Reddit ·

Steve blamed "choppy" Google referral traffic for the miss on US daily active user (DAU) WHILST being in a standoff with Google on the AI licensing deal... hmm 🤔 One way or another a deal is happening. What's gonna be interesting is to see how good or bad (which the market is pricing in) would it be. PS - I don't own the stock but like the company.

1

|0