Advertisement

- Switzerland

- /

- Medical Equipment

- /

- SWX:VBSN

3 Undiscovered Gems in Europe with Promising Potential

Simply Wall St

Reviewed by Simply Wall St

Amidst a backdrop of economic uncertainty and fresh trade tariffs impacting European markets, the STOXX Europe 600 Index recently ended about 1.4% lower. Despite these challenges, the eurozone's private sector has shown resilience with growth in both services and manufacturing, offering a glimmer of optimism for discerning investors seeking stocks with potential in this dynamic environment.

Top 10 Undiscovered Gems With Strong Fundamentals In Europe

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Nederman Holding | 69.60% | 11.43% | 16.35% | ★★★★★★ |

| Mirbud | 16.01% | 27.19% | 26.48% | ★★★★★★ |

| Caisse Regionale de Credit Agricole Mutuel Toulouse 31 | 14.94% | 0.59% | 5.95% | ★★★★★☆ |

| Moury Construct | 2.93% | 10.42% | 27.28% | ★★★★★☆ |

| Flügger group | 20.98% | 3.24% | -29.82% | ★★★★★☆ |

| Dekpol | 73.04% | 15.36% | 16.35% | ★★★★★☆ |

| ABG Sundal Collier Holding | 0.61% | -1.57% | -8.96% | ★★★★☆☆ |

| Prim | 10.72% | 10.36% | 0.14% | ★★★★☆☆ |

| Procimmo Group | 157.49% | 0.65% | 4.94% | ★★★★☆☆ |

| Grenobloise d'Electronique et d'Automatismes Société Anonyme | 0.01% | 5.17% | -13.11% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

Caisse Regionale de Credit Agricole Mutuel Toulouse 31 (ENXTPA:CAT31)

Simply Wall St Value Rating: ★★★★★☆

Overview: Caisse Regionale de Credit Agricole Mutuel Toulouse 31 operates as a cooperative bank in France, with a market capitalization of approximately €405.78 million.

Operations: The cooperative bank generates revenue primarily from its retail banking segment, amounting to €249.69 million.

CAT31 stands out with its robust financial structure, boasting total assets of €16.3B and equity of €2.0B. With deposits at €13.5B and loans totaling €12.0B, the bank's reliance on customer deposits for 95% of its funding underscores a low-risk profile. Earnings surged by 25%, surpassing the industry average growth of 3%. Trading at a discount of 41% below estimated fair value adds to its appeal, although an allowance for bad loans sits at a modest 85%. The non-performing loan ratio is well-managed at just 1.4%, reflecting prudent risk management practices in place.

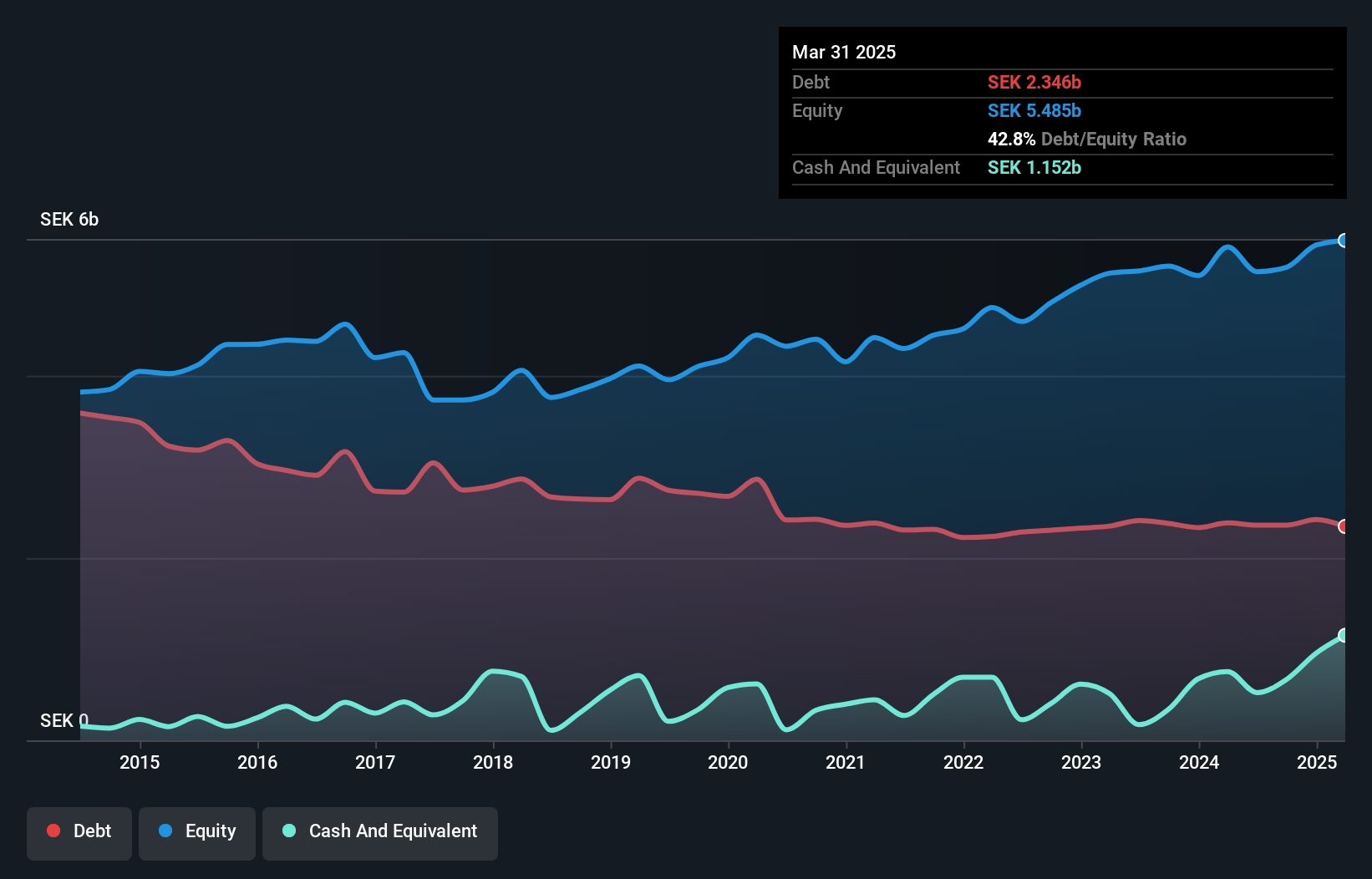

Cloetta (OM:CLA B)

Simply Wall St Value Rating: ★★★★★☆

Overview: Cloetta AB (publ) is a confectionery company with a market capitalization of approximately SEK8.20 billion.

Operations: Cloetta generates revenue primarily from two segments: Pick & mix at SEK2.39 billion and Packaged branded goods at SEK6.22 billion.

Cloetta, a notable player in the confectionery sector, showcases promising financial health. Its net debt to equity ratio stands at a satisfactory 27%, reflecting prudent financial management. The company reported SEK 8.61 billion in sales for 2024, up from SEK 8.30 billion the previous year, and net income rose to SEK 477 million from SEK 437 million. Earnings per share increased to SEK 1.67 from SEK 1.53, indicating solid profitability growth despite not outpacing industry earnings growth of 14.8%. With interest payments well-covered at an EBIT coverage of 5.2x and positive free cash flow, Cloetta appears undervalued by approximately half its fair value estimate.

- Click to explore a detailed breakdown of our findings in Cloetta's health report.

Gain insights into Cloetta's historical performance by reviewing our past performance report.

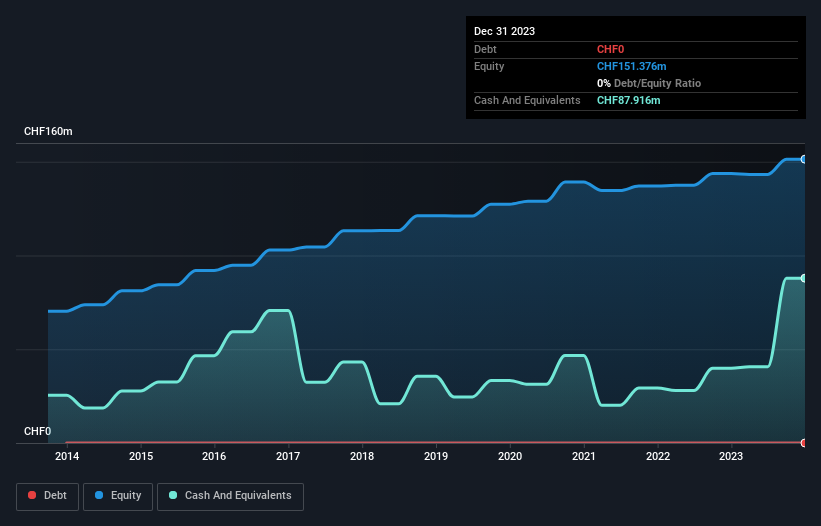

IVF Hartmann Holding (SWX:VBSN)

Simply Wall St Value Rating: ★★★★★★

Overview: IVF Hartmann Holding AG is a company that supplies medical consumer goods both in Switzerland and internationally, with a market capitalization of CHF383.40 million.

Operations: IVF Hartmann generates revenue primarily from Wound Care, Infection Management, and Incontinence Management segments, with Infection Management contributing CHF58.87 million. The company's financials reflect a focus on these core areas to drive its revenue streams.

IVF Hartmann, a nimble player in the medical equipment sector, has demonstrated robust financial health with no debt over the past five years. The company reported a notable earnings growth of 34% last year, outpacing its industry peers. With sales climbing to CHF 158.79 million from CHF 147.95 million and net income rising to CHF 20.3 million from CHF 15.15 million, it showcases strong operational performance. Its price-to-earnings ratio of 18.9x is below the Swiss market average, suggesting potential value for investors seeking opportunities in this space. An increased annual dividend of CHF 3.20 per share further highlights shareholder returns potential.

Seize The Opportunity

- Take a closer look at our European Undiscovered Gems With Strong Fundamentals list of 351 companies by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:VBSN

IVF Hartmann Holding

Provides medical consumer goods in Switzerland and internationally.

Flawless balance sheet with solid track record and pays a dividend.

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor