Advertisement

VP Bank AG (VTX:VPBN) has announced that on 2nd of May, it will be paying a dividend ofCHF4.00, which a reduction from last year's comparable dividend. However, the dividend yield of 5.1% is still a decent boost to shareholder returns.

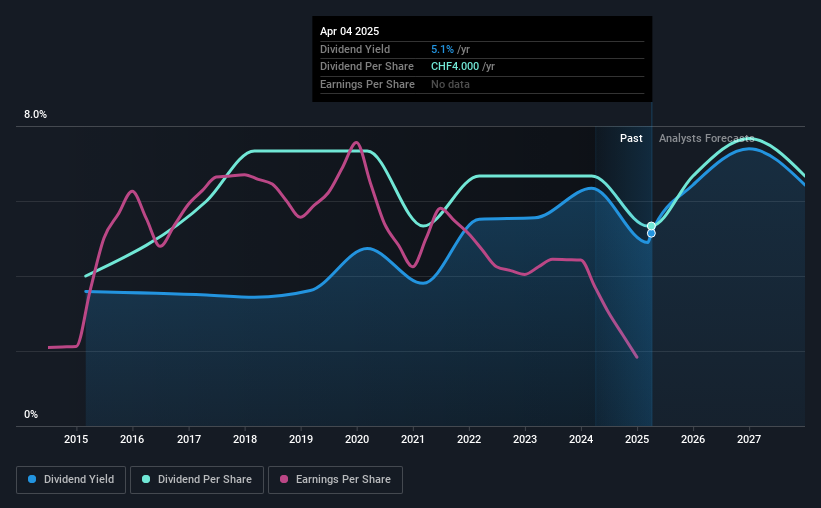

VP Bank's Payment Expected To Have Solid Earnings Coverage

We like to see robust dividend yields, but that doesn't matter if the payment isn't sustainable.

Having distributed dividends for at least 10 years, VP Bank has a long history of paying out a part of its earnings to shareholders. Past distributions unfortunately do not guarantee future ones, and VP Bank's last earnings report actually showed that the company went over its net earnings in its total dividend distribution. This is an alarming sign that could mean that VP Bank's dividend at its current rate may no longer be sustainable for longer.

According to analysts, EPS should be several times higher in the next 3 years. They also estimate that the future payout ratio could reach 49% in the same time horizon, which is in a comfortable range for us.

See our latest analysis for VP Bank

Dividend Volatility

The company's dividend history has been marked by instability, with at least one cut in the last 10 years. The annual payment during the last 10 years was CHF3.00 in 2015, and the most recent fiscal year payment was CHF4.00. This works out to be a compound annual growth rate (CAGR) of approximately 2.9% a year over that time. Modest growth in the dividend is good to see, but we think this is offset by historical cuts to the payments. It is hard to live on a dividend income if the company's earnings are not consistent.

Dividend Growth Potential Is Shaky

Growing earnings per share could be a mitigating factor when considering the past fluctuations in the dividend. VP Bank's earnings per share has shrunk at 25% a year over the past five years. Such rapid declines definitely have the potential to constrain dividend payments if the trend continues into the future. It's not all bad news though, as the earnings are predicted to rise over the next 12 months - we would just be a bit cautious until this becomes a long term trend.

VP Bank's Dividend Doesn't Look Sustainable

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The track record isn't great, and the payments are a bit high to be considered sustainable. We would probably look elsewhere for an income investment.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Taking the debate a bit further, we've identified 3 warning signs for VP Bank that investors need to be conscious of moving forward. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SWX:VPBN

VP Bank

Provides wealth management and investment advisory services for private and institutional investors in Liechtenstein, rest of Europe, and internationally.

Excellent balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|26.1% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|21.3% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|61.2% undervalued

ME

Community Contributor