Advertisement

- Switzerland

- /

- Capital Markets

- /

- SWX:EFGN

European Dividend Stocks To Consider Now

Simply Wall St

Reviewed by Simply Wall St

As the European market experiences a positive upswing, with the pan-European STOXX Europe 600 Index rising by 3.44% amid easing tariff concerns and stronger-than-expected economic growth in the eurozone, investors are increasingly looking towards dividend stocks as a potential source of steady income. In this environment of cautious optimism, selecting dividend stocks with strong fundamentals and a history of reliable payouts can be an effective strategy for those seeking to balance growth opportunities with income stability.

Top 10 Dividend Stocks In Europe

| Name | Dividend Yield | Dividend Rating |

| Julius Bär Gruppe (SWX:BAER) | 4.73% | ★★★★★★ |

| Zurich Insurance Group (SWX:ZURN) | 4.29% | ★★★★★★ |

| Bredband2 i Skandinavien (OM:BRE2) | 4.54% | ★★★★★★ |

| OVB Holding (XTRA:O4B) | 4.42% | ★★★★★★ |

| Rubis (ENXTPA:RUI) | 6.90% | ★★★★★★ |

| HEXPOL (OM:HPOL B) | 5.00% | ★★★★★★ |

| Deutsche Post (XTRA:DHL) | 4.99% | ★★★★★★ |

| S.N. Nuclearelectrica (BVB:SNN) | 9.65% | ★★★★★★ |

| Cembra Money Bank (SWX:CMBN) | 4.22% | ★★★★★★ |

| Banque Cantonale Vaudoise (SWX:BCVN) | 4.37% | ★★★★★★ |

Click here to see the full list of 237 stocks from our Top European Dividend Stocks screener.

Let's dive into some prime choices out of the screener.

Vicat (ENXTPA:VCT)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Vicat S.A., with a market cap of €2.31 billion, operates in the construction industry through its production and sale of cement, ready-mixed concrete, and aggregates.

Operations: Vicat S.A.'s revenue is primarily derived from its Cement segment, which accounts for €2.45 billion, and its Concrete & Aggregates segment, contributing €1.53 billion.

Dividend Yield: 3.9%

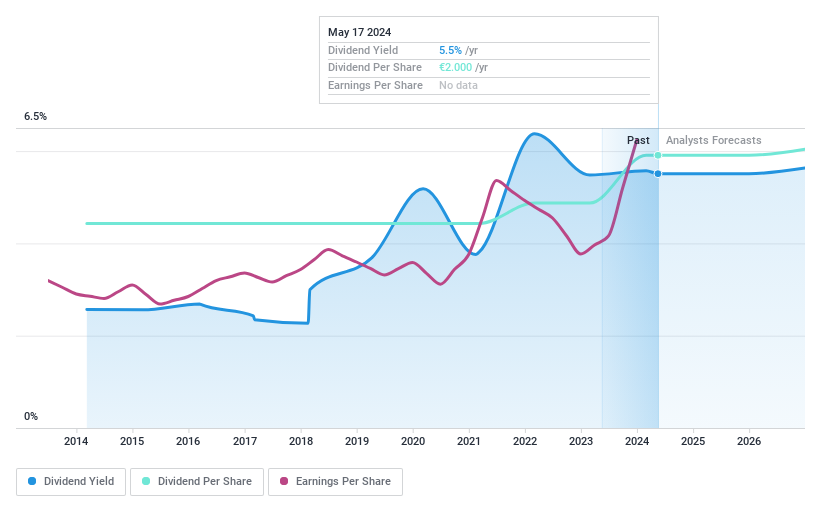

Vicat offers a stable dividend profile with a proposed €2.00 per share payout for the 2024 financial year, consistent with previous years. The company's dividends are well covered by earnings and cash flows, boasting a low payout ratio of 32.6% and cash payout ratio of 24.9%. Although its yield of 3.85% is below the top tier in France, Vicat's dividends have been reliable and steadily increasing over the past decade.

- Take a closer look at Vicat's potential here in our dividend report.

- According our valuation report, there's an indication that Vicat's share price might be on the cheaper side.

EFG International (SWX:EFGN)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: EFG International AG, with a market cap of CHF3.87 billion, operates through its subsidiaries to offer private banking, wealth management, and asset management services.

Operations: EFG International's revenue segments include Corporate (CHF53.60 million), Global Markets & Treasury (CHF94.70 million), Investment and Wealth Solutions (CHF124.90 million), and Private Banking and Wealth Management across various regions: Americas (CHF128.80 million), Asia Pacific (CHF195.50 million), United Kingdom (CHF192.30 million), Switzerland & Italy (CHF452.20 million), and Continental Europe & Middle East (CHF254.80 million).

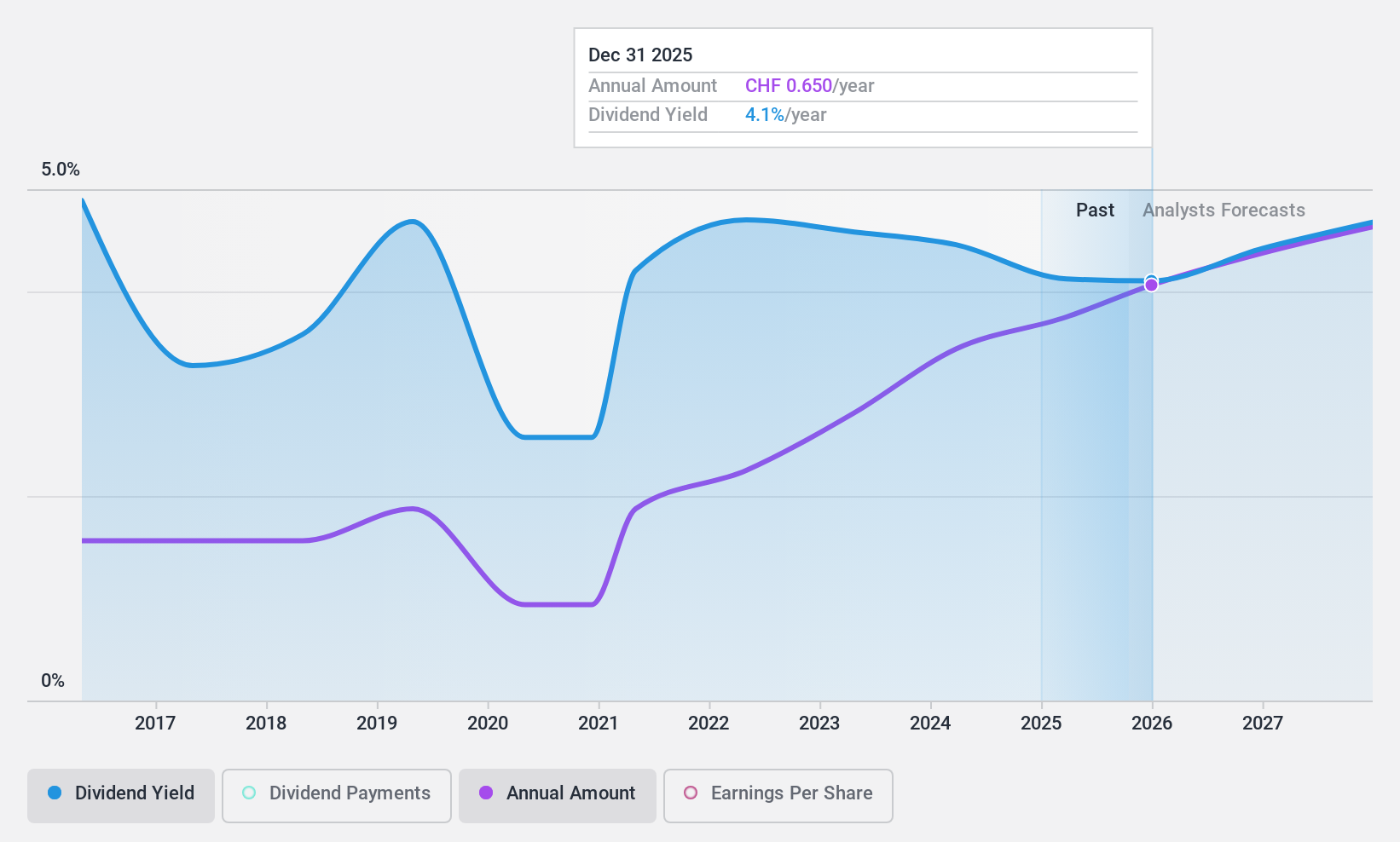

Dividend Yield: 4.6%

EFG International's dividend yield of 4.64% ranks in the top 25% of Swiss dividend payers, though its track record is unstable with past volatility. Despite this, dividends are currently covered by earnings with a payout ratio of 59.9%, and future coverage is forecasted at 58.2%. Recent executive changes and strategic focus on M&A may influence growth prospects. The stock trades at a discount to its estimated fair value, suggesting potential relative value for investors.

- Dive into the specifics of EFG International here with our thorough dividend report.

- Insights from our recent valuation report point to the potential undervaluation of EFG International shares in the market.

Swiss Re (SWX:SREN)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Swiss Re AG, with a market cap of CHF44.79 billion, operates globally providing reinsurance, insurance, other insurance-based risk transfer solutions, and related services.

Operations: Swiss Re AG's revenue is primarily derived from Property & Casualty Reinsurance ($19.55 billion), Life & Health Reinsurance ($17.62 billion), and Corporate Solutions ($6.57 billion).

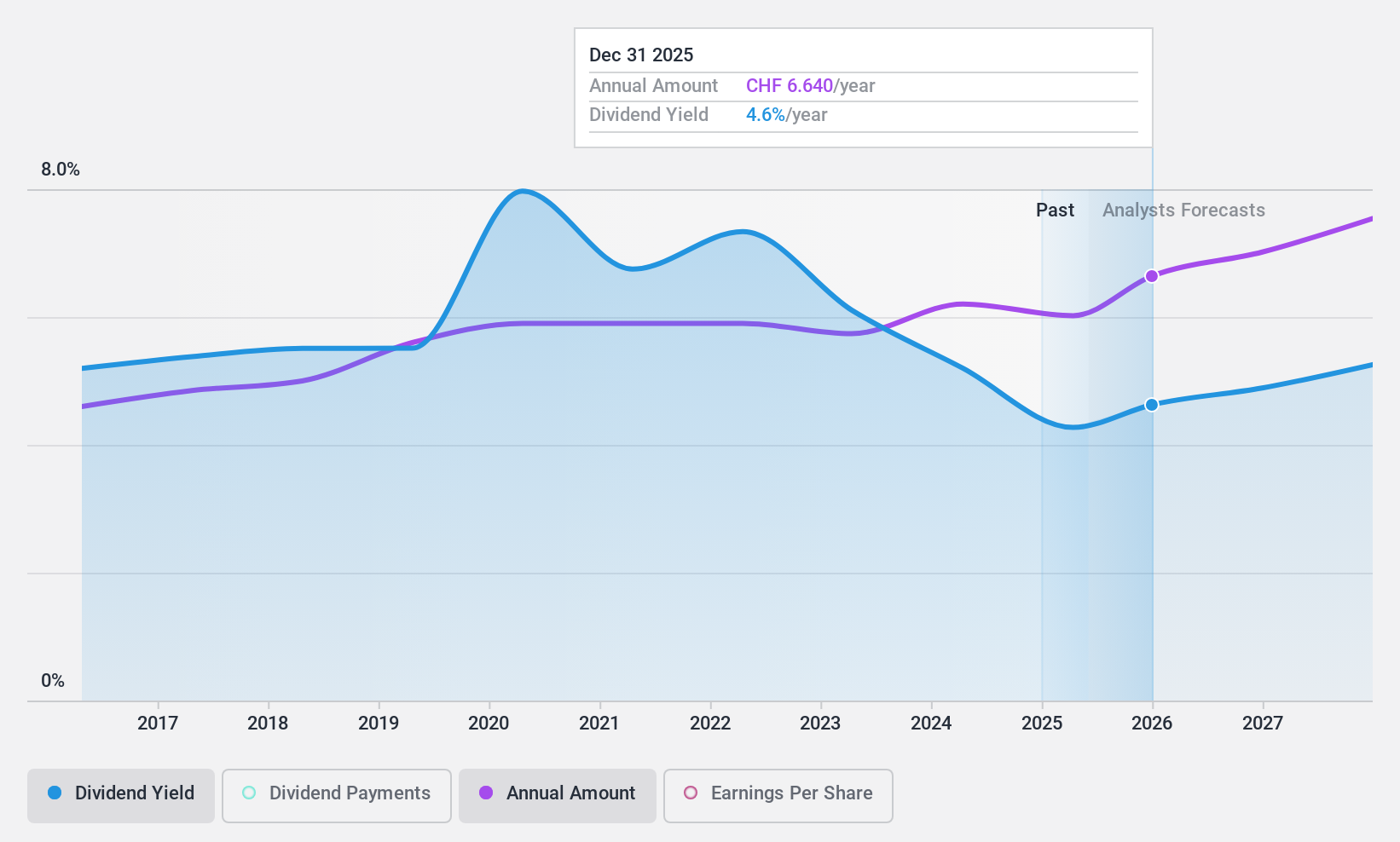

Dividend Yield: 4%

Swiss Re's dividend payments are supported by earnings and cash flows, with payout ratios of 67.5% and 69.1%, respectively, indicating sustainability despite past volatility. The recent approval of a US$7.35 per share dividend underscores its strong capital position, although the yield remains modest compared to top Swiss payers. Recent executive changes might impact future performance, but the stock trades significantly below estimated fair value, potentially offering relative value to investors seeking dividends.

- Get an in-depth perspective on Swiss Re's performance by reading our dividend report here.

- The analysis detailed in our Swiss Re valuation report hints at an deflated share price compared to its estimated value.

Where To Now?

- Explore the 237 names from our Top European Dividend Stocks screener here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if EFG International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:EFGN

EFG International

Provides private banking, wealth management, and asset management services.

Excellent balance sheet established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor