- Switzerland

- /

- Chemicals

- /

- SWX:SIKA

COLTENE Holding And 2 Other Stocks On SIX Swiss Exchange That May Be Trading Below Intrinsic Value

Reviewed by Simply Wall St

The Switzerland market shrugged off a mild mid-morning setback and moved higher on Tuesday to eventually end the day's session on a firm note. In this environment, identifying stocks that may be trading below their intrinsic value can offer significant opportunities for investors looking to capitalize on potential market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In Switzerland

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Sulzer (SWX:SUN) | CHF130.60 | CHF253.21 | 48.4% |

| LEM Holding (SWX:LEHN) | CHF1228.00 | CHF2020.31 | 39.2% |

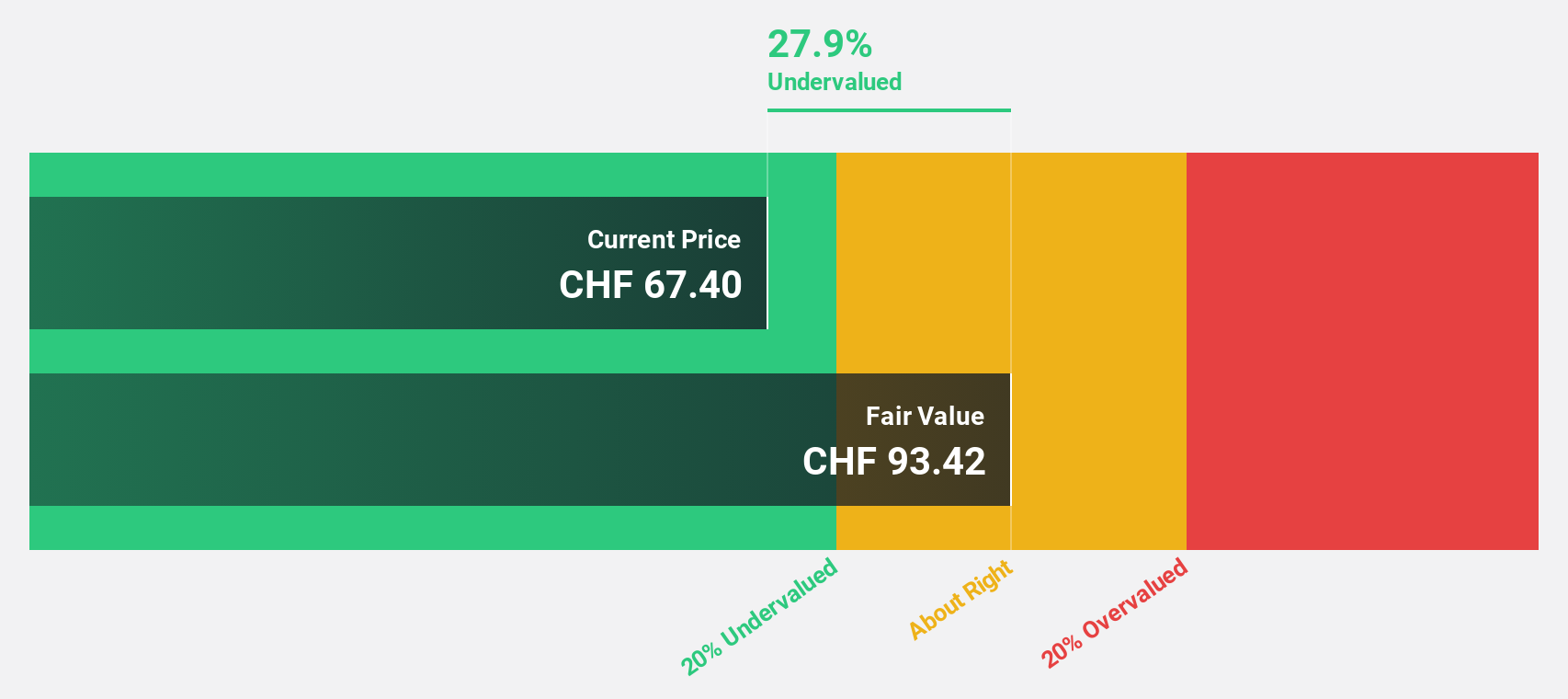

| COLTENE Holding (SWX:CLTN) | CHF47.20 | CHF74.80 | 36.9% |

| Burckhardt Compression Holding (SWX:BCHN) | CHF610.00 | CHF854.71 | 28.6% |

| Julius Bär Gruppe (SWX:BAER) | CHF47.84 | CHF89.85 | 46.8% |

| Georg Fischer (SWX:GF) | CHF64.75 | CHF99.89 | 35.2% |

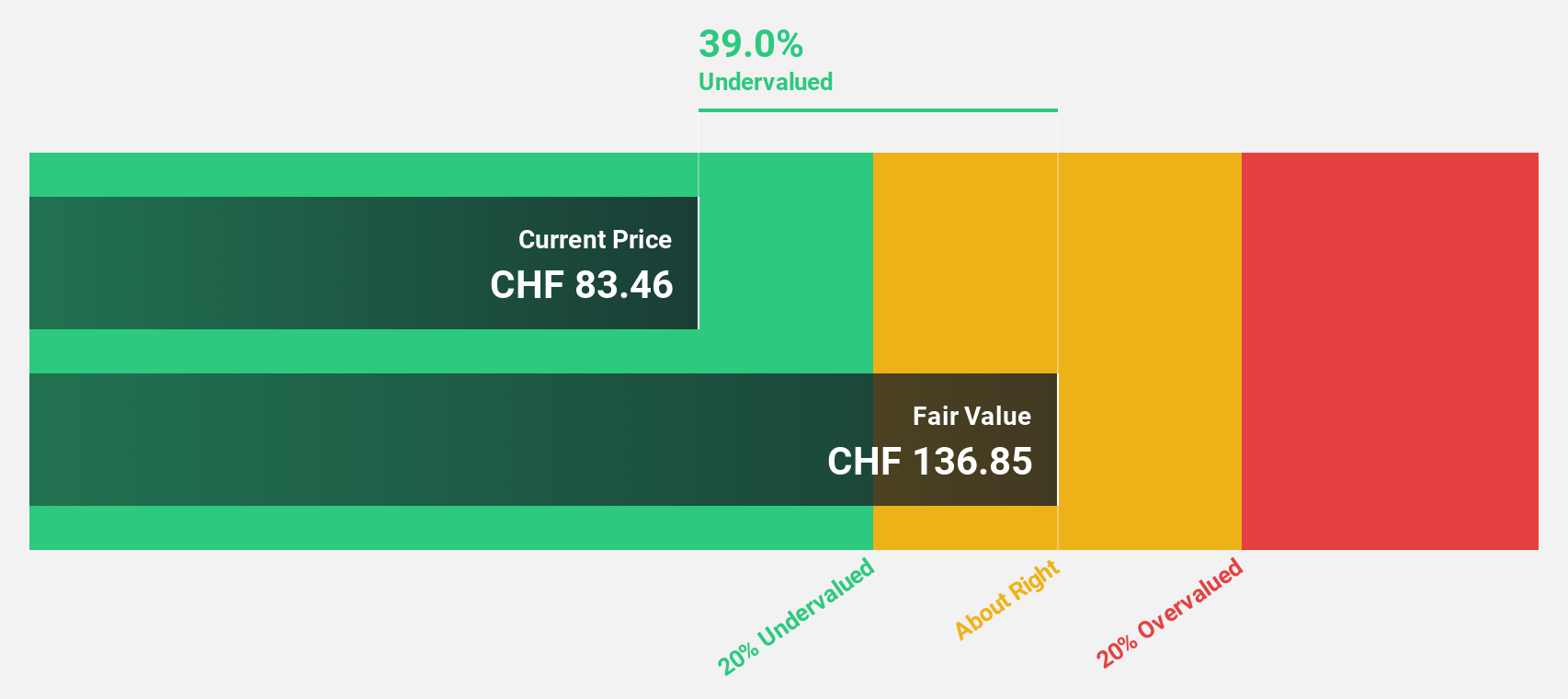

| SGS (SWX:SGSN) | CHF95.64 | CHF129.39 | 26.1% |

| Comet Holding (SWX:COTN) | CHF336.50 | CHF589.14 | 42.9% |

| Medartis Holding (SWX:MED) | CHF72.00 | CHF132.71 | 45.7% |

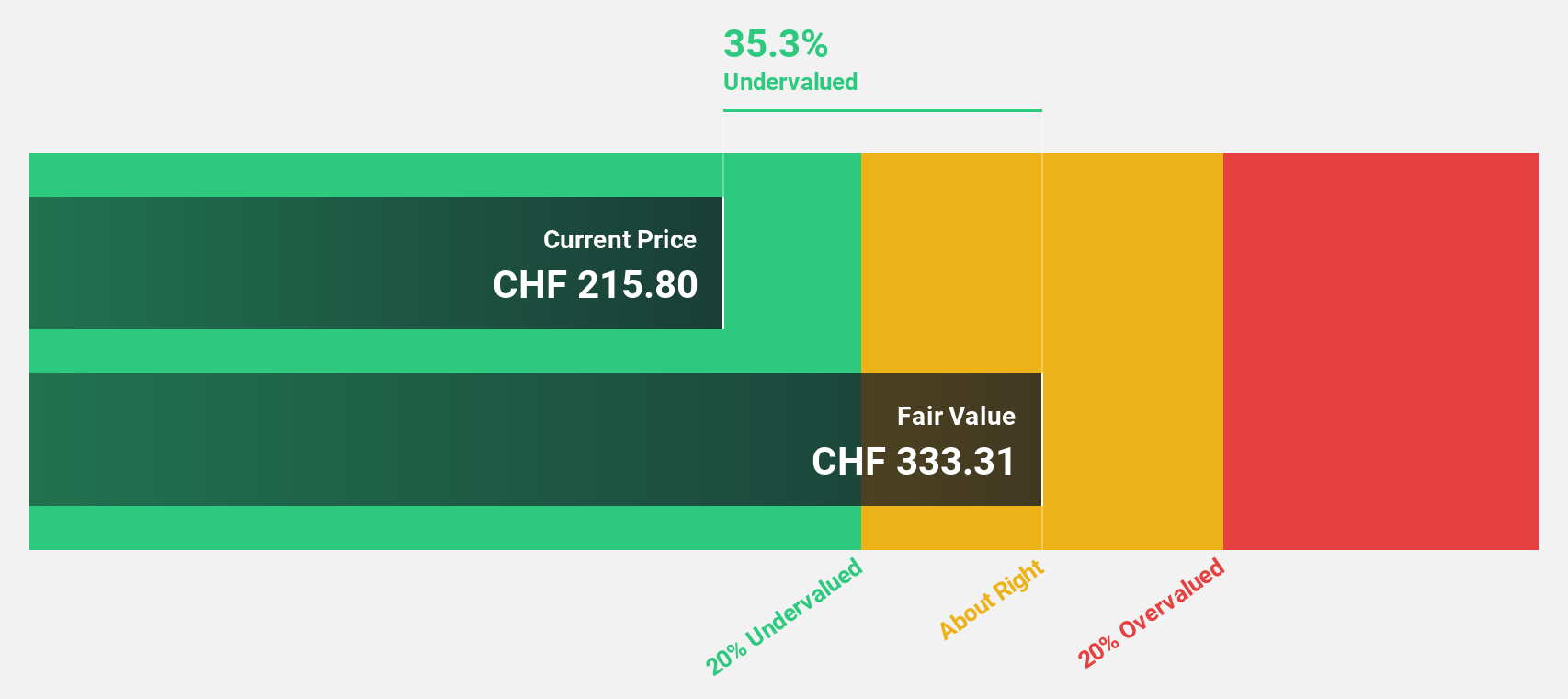

| Sika (SWX:SIKA) | CHF269.10 | CHF351.32 | 23.4% |

Below we spotlight a couple of our favorites from our exclusive screener.

COLTENE Holding (SWX:CLTN)

Overview: COLTENE Holding AG develops, manufactures, and sells disposables, tools, and equipment for dentists and dental laboratories across various regions worldwide with a market cap of CHF282.04 million.

Operations: The company's revenue is primarily generated from the sale of disposables, tools, and equipment for dentists and dental laboratories, amounting to CHF242.73 million.

Estimated Discount To Fair Value: 36.9%

COLTENE Holding is trading at CHF47.2, significantly below its estimated fair value of CHF74.8, making it highly undervalued based on discounted cash flow analysis. Despite a dividend yield of 4.24%, the payout isn't well covered by earnings. Profit margins have decreased from 9.7% to 4.9% over the past year, but earnings are forecast to grow significantly at 21% per year, outpacing the Swiss market's expected growth rate of 8.9%.

- The analysis detailed in our COLTENE Holding growth report hints at robust future financial performance.

- Click here to discover the nuances of COLTENE Holding with our detailed financial health report.

SGS (SWX:SGSN)

Overview: SGS SA offers inspection, testing, and verification services across Europe, Africa, the Middle East, the Americas, and the Asia Pacific with a market cap of CHF18.10 billion.

Operations: The company's revenue segments include Business Assurance, generating CHF755 million, and Segment Adjustment, contributing CHF5.92 billion.

Estimated Discount To Fair Value: 26.1%

SGS (CHF95.64) is trading 26.1% below its estimated fair value of CHF129.39, indicating it may be undervalued based on discounted cash flow analysis. The company's revenue growth forecast of 5.5% per year surpasses the Swiss market's 4.8%, and its earnings are expected to grow at 11.9% annually, outpacing the market's 8.9%. However, SGS has a high level of debt and its dividend yield of 3.35% is not well covered by earnings, which could pose risks for investors seeking income stability.

- Our expertly prepared growth report on SGS implies its future financial outlook may be stronger than recent results.

- Dive into the specifics of SGS here with our thorough financial health report.

Sika (SWX:SIKA)

Overview: Sika AG is a specialty chemicals company that develops, produces, and sells systems and products for bonding, sealing, damping, reinforcing, and protecting in the building sector and motor vehicle industry worldwide, with a market cap of CHF43.17 billion.

Operations: The company generates revenue from two main segments: Products for Construction Industry (CHF9.45 billion) and Products for Industrial Manufacturing (CHF1.78 billion).

Estimated Discount To Fair Value: 23.4%

Sika (CHF269.1) is trading 23.4% below its estimated fair value of CHF351.32, suggesting it may be undervalued based on discounted cash flow analysis. The company's earnings are forecast to grow at 13.1% annually, surpassing the Swiss market's 8.9%. Recent half-year results showed sales of CHF5.83 billion and net income of CHF575.9 million, both up from last year, reflecting strong financial performance despite a high level of debt and past shareholder dilution.

- Our earnings growth report unveils the potential for significant increases in Sika's future results.

- Navigate through the intricacies of Sika with our comprehensive financial health report here.

Where To Now?

- Discover the full array of 14 Undervalued SIX Swiss Exchange Stocks Based On Cash Flows right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:SIKA

Sika

A specialty chemicals company, develops, produces, and sells systems and products for bonding, sealing, damping, reinforcing, and protecting in the building sector and motor vehicle industry worldwide.

Solid track record with adequate balance sheet.

Similar Companies

Market Insights

Community Narratives