Advertisement

- Switzerland

- /

- Insurance

- /

- SWX:HELN

3 European Stocks That May Be Priced Below Their Estimated Value

Simply Wall St

Reviewed by Simply Wall St

Amid renewed worries about inflated AI stock valuations and receding expectations for a U.S. interest rate cut, European markets have experienced a downturn, with the pan-European STOXX Europe 600 Index ending 2.21% lower. Despite this challenging environment, opportunities may exist in stocks that are priced below their estimated value, offering potential for investors who focus on fundamental strengths such as solid business models and sustainable growth prospects.

Top 10 Undervalued Stocks Based On Cash Flows In Europe

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| YIT Oyj (HLSE:YIT) | €2.988 | €5.94 | 49.7% |

| Roche Bobois (ENXTPA:RBO) | €35.00 | €69.49 | 49.6% |

| KB Components (OM:KBC) | SEK42.30 | SEK83.54 | 49.4% |

| HMS Bergbau (XTRA:HMU) | €52.00 | €103.80 | 49.9% |

| Exel Composites Oyj (HLSE:EXL1V) | €0.392 | €0.78 | 49.8% |

| Esautomotion (BIT:ESAU) | €3.12 | €6.18 | 49.5% |

| EcoUp Oyj (HLSE:ECOUP) | €1.34 | €2.65 | 49.4% |

| cyan (XTRA:CYR) | €2.28 | €4.55 | 49.9% |

| Circle (BIT:CIRC) | €7.94 | €15.68 | 49.4% |

| Allcore (BIT:CORE) | €1.33 | €2.64 | 49.7% |

Below we spotlight a couple of our favorites from our exclusive screener.

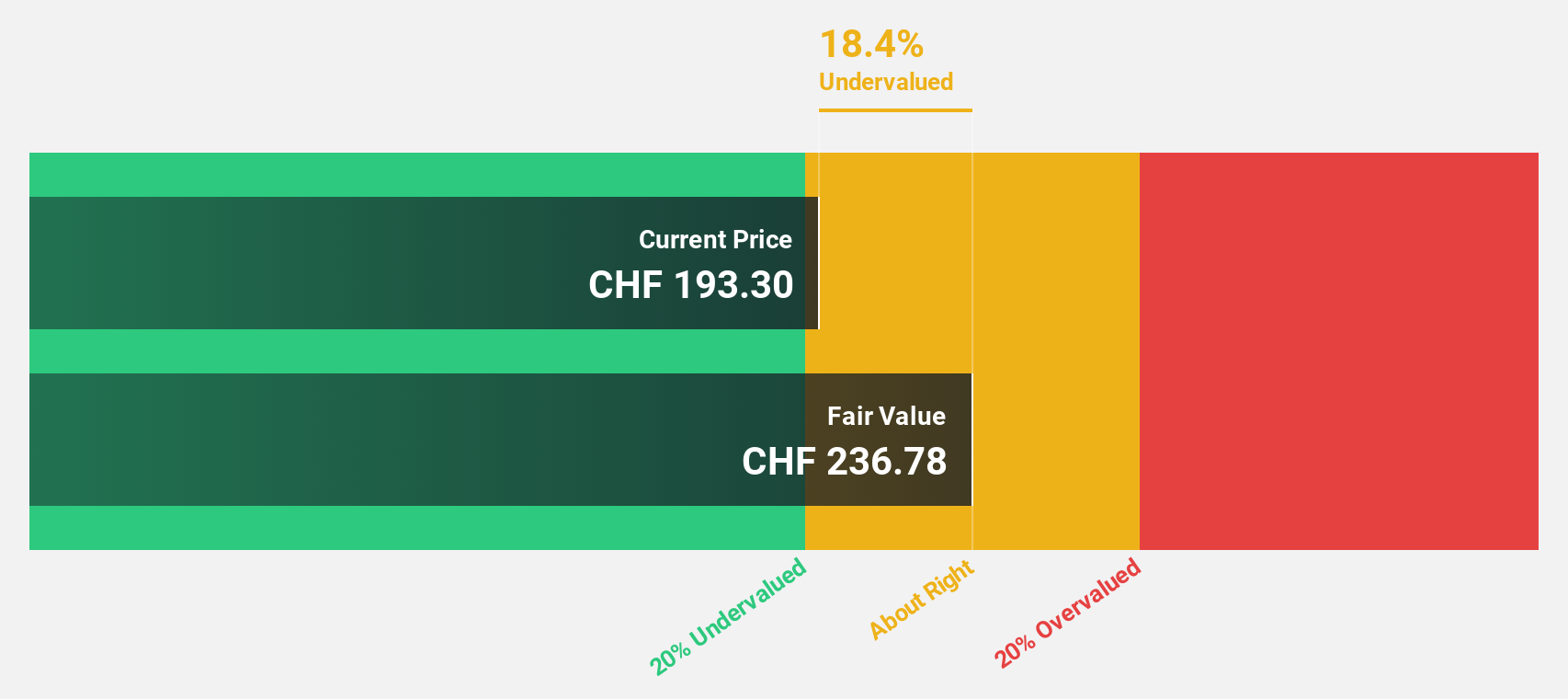

Helvetia Holding (SWX:HELN)

Overview: Helvetia Holding AG operates in life, non-life, and reinsurance sectors across Switzerland, Germany, Austria, Spain, Italy, France, and internationally with a market cap of CHF10.83 billion.

Operations: The company's revenue segments consist of CHF2.11 billion from life insurance, CHF7.26 billion from non-life insurance, and CHF391.90 million from reinsurance activities.

Estimated Discount To Fair Value: 17.7%

Helvetia Holding is trading at CHF204.8, which is 17.7% below its estimated fair value of CHF248.97, indicating potential undervaluation based on discounted cash flow analysis. The company reported a net income increase to CHF307.2 million for H1 2025 from CHF243.1 million the previous year, with earnings per share rising to CHF5.75 from CHF4.54, reflecting strong profit growth of 95.9% last year and forecasted annual earnings growth of 21.6%.

- Our expertly prepared growth report on Helvetia Holding implies its future financial outlook may be stronger than recent results.

- Unlock comprehensive insights into our analysis of Helvetia Holding stock in this financial health report.

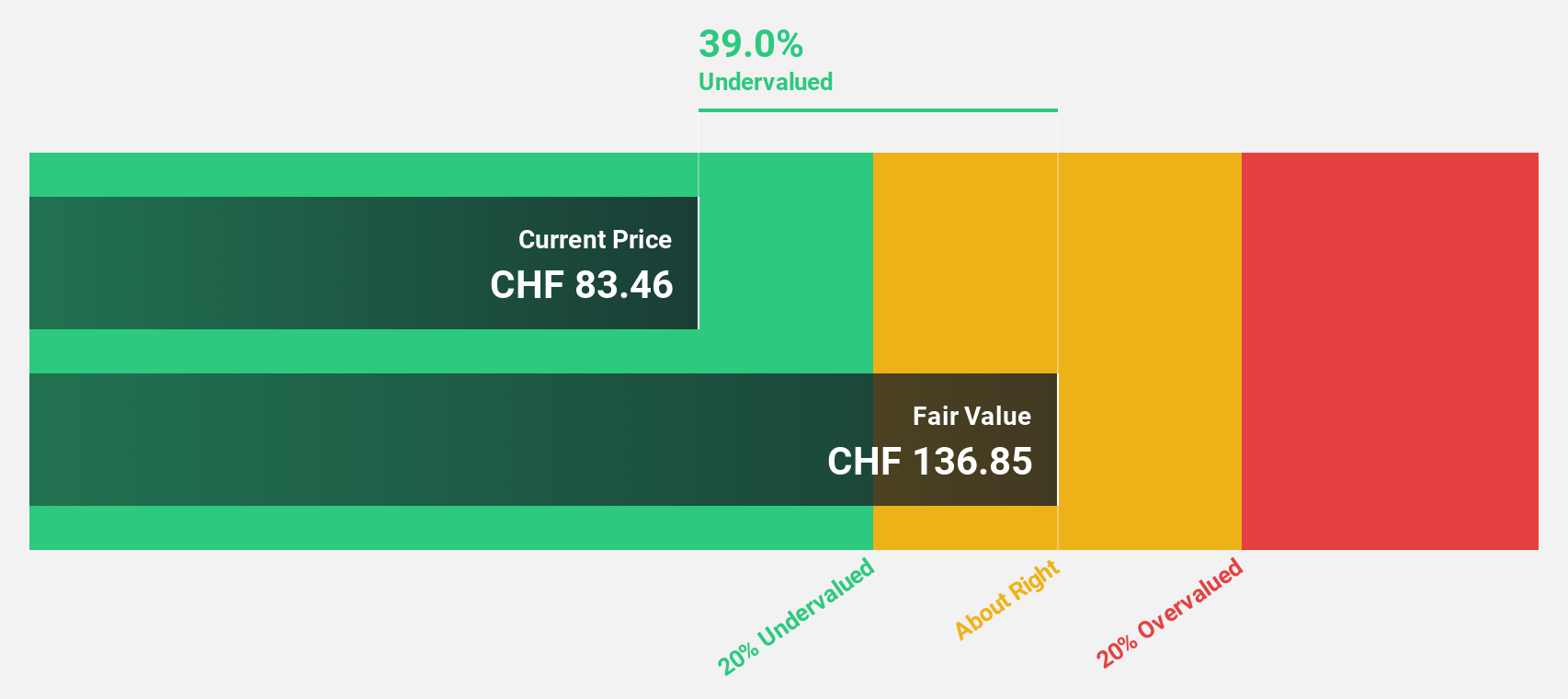

SGS (SWX:SGSN)

Overview: SGS SA offers inspection, testing, and certification services across Europe, Africa, the Middle East, Latin America, North America, and the Asia Pacific with a market cap of CHF17.39 billion.

Operations: The company's revenue segments include Business Assurance (CHF775 million), Testing & Inspection - Natural Resources (CHF1.59 billion), Testing & Inspection - Health & Nutrition (CHF915 million), Testing & Inspection - Industries & Environment (CHF2.29 billion), and Testing & Inspection - Connectivity & Products (CHF1.31 billion).

Estimated Discount To Fair Value: 34.2%

SGS, trading at CHF89.82, is significantly undervalued with a fair value estimate of CHF136.52. Despite high debt levels, SGS's earnings are forecast to grow 11% annually, outpacing the Swiss market's growth rate. Recent strategic partnerships with EcoVadis and Diginex enhance its ESG capabilities and global reach, potentially strengthening its financial position through expanded service offerings in sustainable finance and auditing services.

- The growth report we've compiled suggests that SGS' future prospects could be on the up.

- Get an in-depth perspective on SGS' balance sheet by reading our health report here.

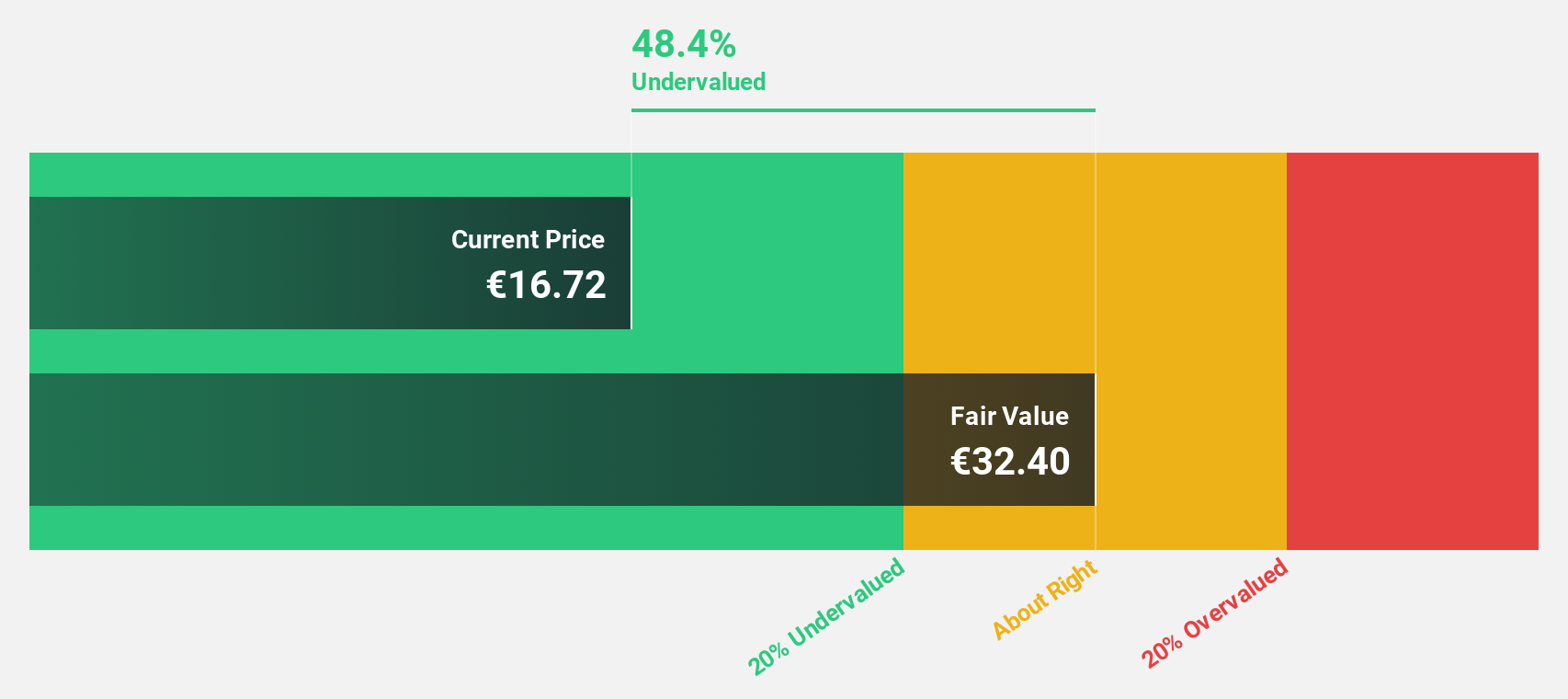

Delivery Hero (XTRA:DHER)

Overview: Delivery Hero SE operates in the online food ordering, quick commerce, and delivery services sector with a market cap of approximately €4.98 billion.

Operations: The company's revenue segments include Asia (€4.28 billion), Europe (€2.16 billion), Americas (€1.02 billion), Integrated Verticals (€2.95 billion), and MENA (Middle East and North Africa) (€3.89 billion).

Estimated Discount To Fair Value: 48.4%

Delivery Hero, trading at €16.72, is significantly undervalued with a fair value estimate of €32.4. Despite a net loss of €396.3 million for the half year ending June 2025, its earnings are expected to grow 88.33% annually, outpacing the German market's growth rate. Recent board changes include Warren Jenson joining as Deputy Chair following Naspers Group's decision to reduce its stake in Delivery Hero, potentially impacting strategic direction and investor sentiment.

- In light of our recent growth report, it seems possible that Delivery Hero's financial performance will exceed current levels.

- Take a closer look at Delivery Hero's balance sheet health here in our report.

Taking Advantage

- Click through to start exploring the rest of the 197 Undervalued European Stocks Based On Cash Flows now.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready To Venture Into Other Investment Styles?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Helvetia Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SWX:HELN

Helvetia Holding

Engages in life and non-life insurance, and reinsurance business in Switzerland, Germany, Austria, Spain, Italy, France, and internationally.

Solid track record established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.6% undervalued

TI

Community Contributor

Recently Updated Narratives

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6928.0% undervalued

44 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8149.5% undervalued

7 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

AU

AuCA on Nova Ljubljanska Banka d.d ·

Nova Ljubljanska Banka d.d will expect a 11.2% revenue boost driving future growth

Fair Value:€20916.3% undervalued

23 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3404.9% undervalued

134 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

83 followersusers have followed this narrative

11 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7923.6% undervalued

923 followersusers have followed this narrative

5 commentsusers have commented on this narrative

22 likesusers have liked this narrative