- Switzerland

- /

- Professional Services

- /

- SWX:ADEN

Adecco Group's (VTX:ADEN) Returns On Capital Tell Us There Is Reason To Feel Uneasy

Ignoring the stock price of a company, what are the underlying trends that tell us a business is past the growth phase? A business that's potentially in decline often shows two trends, a return on capital employed (ROCE) that's declining, and a base of capital employed that's also declining. This indicates the company is producing less profit from its investments and its total assets are decreasing. In light of that, from a first glance at Adecco Group (VTX:ADEN), we've spotted some signs that it could be struggling, so let's investigate.

What is Return On Capital Employed (ROCE)?

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. Analysts use this formula to calculate it for Adecco Group:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

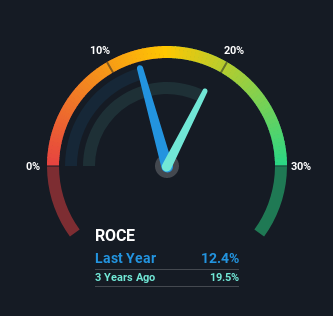

0.12 = €686m ÷ (€9.9b - €4.4b) (Based on the trailing twelve months to March 2021).

So, Adecco Group has an ROCE of 12%. In absolute terms, that's a pretty normal return, and it's somewhat close to the Professional Services industry average of 11%.

View our latest analysis for Adecco Group

In the above chart we have measured Adecco Group's prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Adecco Group here for free.

What The Trend Of ROCE Can Tell Us

In terms of Adecco Group's historical ROCE movements, the trend doesn't inspire confidence. About five years ago, returns on capital were 20%, however they're now substantially lower than that as we saw above. On top of that, it's worth noting that the amount of capital employed within the business has remained relatively steady. Companies that exhibit these attributes tend to not be shrinking, but they can be mature and facing pressure on their margins from competition. So because these trends aren't typically conducive to creating a multi-bagger, we wouldn't hold our breath on Adecco Group becoming one if things continue as they have.

Another thing to note, Adecco Group has a high ratio of current liabilities to total assets of 44%. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. While it's not necessarily a bad thing, it can be beneficial if this ratio is lower.

Our Take On Adecco Group's ROCE

All in all, the lower returns from the same amount of capital employed aren't exactly signs of a compounding machine. But investors must be expecting an improvement of sorts because over the last five yearsthe stock has delivered a respectable 46% return. Regardless, we don't feel too comfortable with the fundamentals so we'd be steering clear of this stock for now.

Like most companies, Adecco Group does come with some risks, and we've found 3 warning signs that you should be aware of.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

If you’re looking to trade Adecco Group, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SWX:ADEN

Adecco Group

Provides human resource services to businesses and organizations in Europe, North America, Asia Pacific, South America, and North Africa.

Very undervalued with mediocre balance sheet.