Advertisement

- Canada

- /

- Renewable Energy

- /

- TSX:BEPC

Brookfield Renewable (TSX:BEPC) Q2 Earnings Reveal Record Sales but Significant Net Loss; Dividend Affirmed

Simply Wall St

Reviewed by Simply Wall St

Brookfield Renewable(TSX:BEPC) is navigating a dynamic environment marked by both opportunities and challenges. Recent highlights include a record performance in funds from operations and strategic acquisitions, juxtaposed against regulatory impacts and forecasted earnings declines. In the discussion that follows, we will explore Brookfield Renewable's financial health, operational inefficiencies, strategic growth initiatives, and external threats to provide a comprehensive overview of the company's current business situation.

Explore the full analysis report here for a deeper understanding of Brookfield Renewable.

Strengths: Core Advantages Driving Sustained Success For Brookfield Renewable

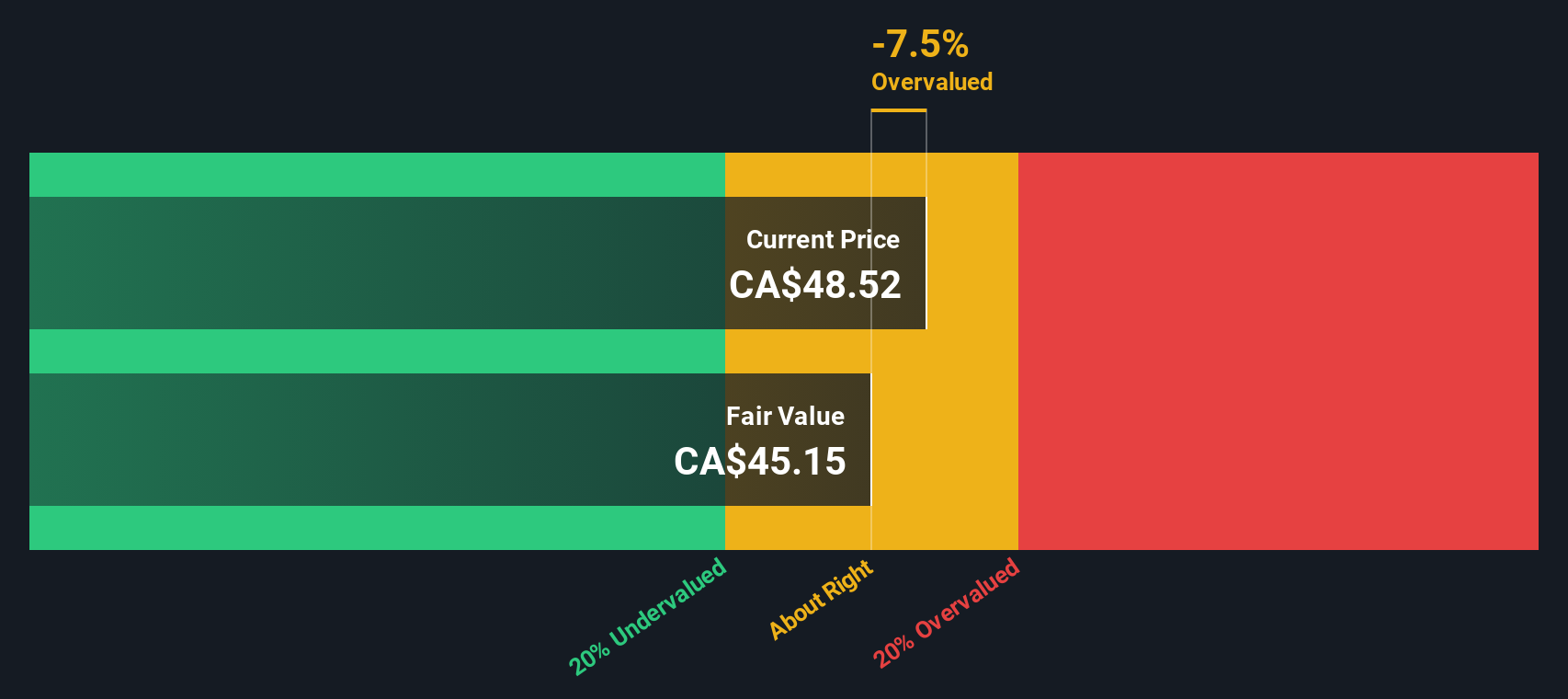

Brookfield Renewable has demonstrated strong financial health, evidenced by a record performance in funds from operations for the second quarter, as highlighted by CEO Connor Teskey. The company’s solid financial position, with $4.4 billion in available liquidity, allows it to seize growth opportunities in the current market, according to CFO Wyatt Hartley. The company’s leadership in the renewable sector is further solidified by its expansive operating fleet and development pipeline, contributing to its market differentiation. Additionally, the company’s successful acquisitions have bolstered its portfolio, enhancing its competitive edge. Notably, BEPC is trading at a Price-To-Earnings Ratio of 16x, significantly below the industry average of 21.1x and the peer average of 50.9x, indicating it is priced attractively compared to its fair value estimate of CA$264.56.

To explore how Brookfield Renewable's valuation metrics are shaping its market position, check out our detailed analysis of Brookfield Renewable's Valuation.

Weaknesses: Critical Issues Affecting Brookfield Renewable's Performance and Areas For Growth

Brookfield Renewable faces several challenges. Performance issues in Colombia, particularly with Isagen, were noted by CEO Connor Teskey, impacting the company’s overall performance. Regulatory impacts in Spain have also led to reduced revenue recognition, although these do not affect the returns from the underlying assets, as explained by CFO Wyatt Hartley. The company’s Return on Equity (6.9%) is considered low, and its earnings growth over the past year (12.6%) did not outperform the Renewable Energy industry. Furthermore, BEPC’s earnings are forecast to decline by 23.1% per year over the next three years, highlighting the need for strategic adjustments.

To gain deeper insights into Brookfield Renewable's historical performance, explore our detailed analysis of past performance.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

Brookfield Renewable has several growth opportunities on the horizon. The acquisition of a 53% stake in Neoen, the largest investment to date within its renewable power and transition business, is a significant strategic move, as noted by executive Ed Bayford. The growing demand for clean energy, particularly in regions where supply is outpaced, presents a valuable pipeline for the company, as highlighted by CEO Connor Teskey. Additionally, the company’s focus on deploying capital into battery energy storage solutions in select markets and expanding its development pipeline, which now stands at 200 gigawatts with 65 gigawatts in advanced stages, positions it well for future growth.

Threats: Key Risks and Challenges That Could Impact Brookfield Renewable's Success

Brookfield Renewable faces several threats that could impact its success. Market competition is intensifying, with auction prices hitting record highs, indicating challenging supply and demand dynamics, as noted by CEO Connor Teskey. Economic factors, including data center demand and broader electrification, are creating a highly competitive environment. Regulatory challenges also pose a risk, with potential measures needed to achieve approvals, as highlighted by Teskey. Additionally, operational risks, such as those related to the nuclear fuel business and new plant development, could impact long-term business outlook, according to CFO Wyatt Hartley. Furthermore, the company’s dividend payments, while stable, are not well covered by free cash flows, raising concerns about sustainability.

Conclusion

Brookfield Renewable's solid financial health, highlighted by a record performance in funds from operations and substantial liquidity of $4.4 billion, positions it to capitalize on growth opportunities in the renewable energy sector. However, challenges such as performance issues in Colombia, regulatory impacts in Spain, and a forecasted earnings decline necessitate strategic adjustments. The company's significant investments, including a 53% stake in Neoen and a focus on battery energy storage, align with the growing demand for clean energy and support future growth. Despite market competition and regulatory risks, the current Price-To-Earnings Ratio of 16x, well below the industry and peer averages, suggests that the stock is priced attractively relative to its fair value estimate of CA$264.56, indicating potential for future appreciation.

Make It Happen

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

Valuation is complex, but we're here to simplify it.

Discover if Brookfield Renewable might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About TSX:BEPC

Brookfield Renewable

Owns and operates a portfolio of renewable power and sustainable solution assets.

Very low risk and overvalued.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|72.3% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|16.8% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|35.5% undervalued

DA

Community Contributor

New Product Lines And Store Expansion Will Fuel Global Momentum

Fair Value US$270.82|37.9% undervalued

AN

Based on Analyst Price Targets