Air Canada (TSX:AC) shares have been catching the eye of investors once again. This movement has raised questions about whether the current price reflects underlying fundamentals or if the market is simply resetting expectations. For anyone considering buying or holding Air Canada, it is worth pausing to consider what is driving sentiment and whether the stock aligns with your outlook.

Over the last year, Air Canada’s performance has been a mixed bag. The stock has delivered a 25% total return for shareholders, a solid rebound after a difficult stretch previously. However, momentum is uneven, as shares are down 15% year to date, despite a slight gain over the past three months and some pressure in recent weeks. Broader headline trends like revenue growth and fluctuating profits continue to keep investors on their toes, so it makes sense to connect these results with longer-term prospects.

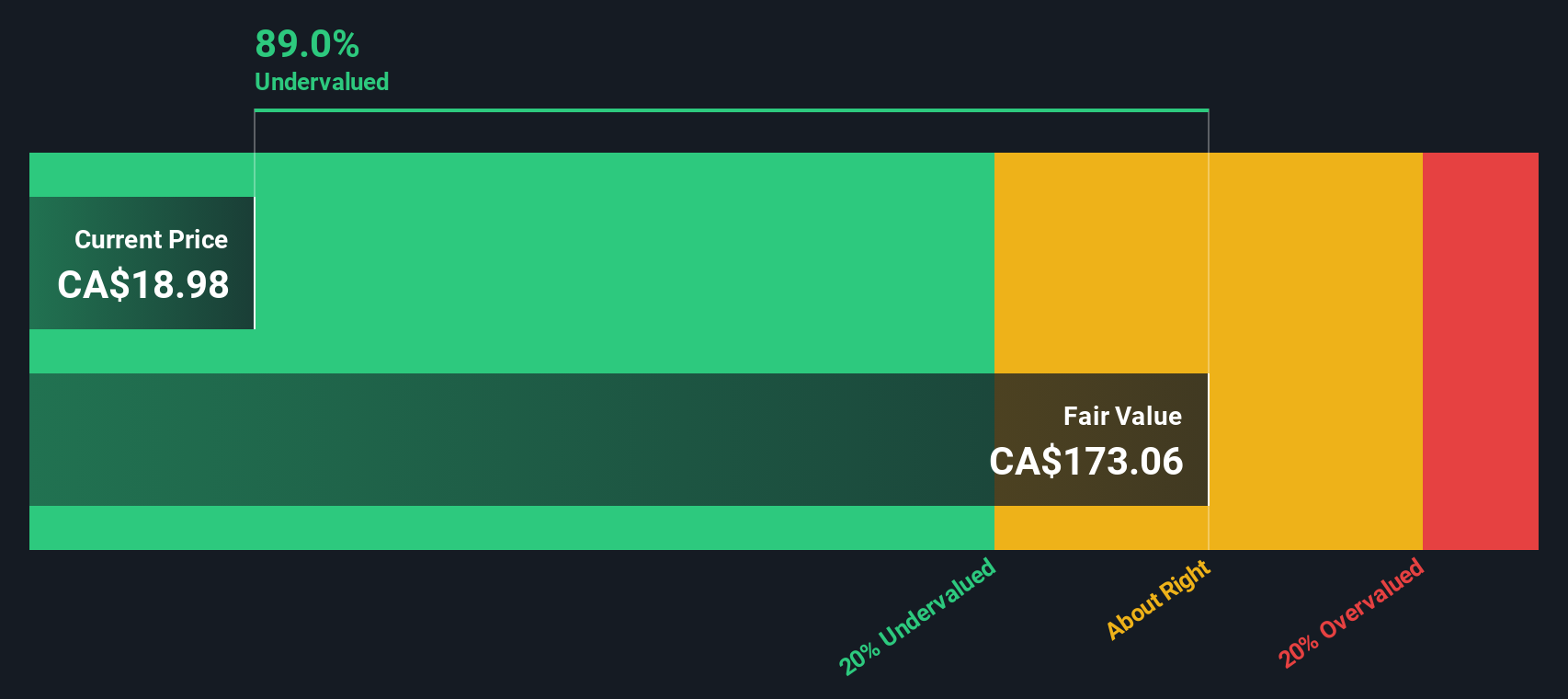

The real question now is whether the recent price action has created a genuine buying opportunity, or if the market is already looking ahead and pricing in all future growth for Air Canada.

Advertisement

Most Popular Narrative: 25% Undervalued

According to the most widely followed valuation narrative, Air Canada is currently trading at a significant discount to its fair value. This suggests that the market may be underestimating the company’s potential or overlooking key drivers of future growth.

Aggressive international long-haul network expansion, notably into Latin America, Europe, and Southeast Asia, along with successful development of sixth freedom traffic, positions Air Canada to capture a larger share of connecting global passengers. This supports both top-line growth and load factor resilience.

Curious what’s fueling such a bold fair value gap? Analysts’ projections rely on a growth blueprint that could drastically reshape Air Canada’s profit engine in a few short years. Interested in which pieces of the puzzle have the biggest impact on that price target? Find out what assumptions make this valuation stand out from the market’s view.

However, persistent labor cost increases and intense competition on international routes could quickly weaken the case for Air Canada being undervalued.

Looking at Air Canada through the lens of our DCF model paints an even starker picture of undervaluation. This approach weighs future cash flows rather than just today's multiples, which highlights what the market might be missing. Is the market mispricing Air Canada's potential, or does it know something the numbers don’t?

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Air Canada for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Air Canada Narrative

If you see things differently or want to put your own view to the test, you can craft a custom narrative using our simple tools in just a few minutes. Do it your way

Take the reins on your portfolio and access the market's next big winners. If you’re serious about staying ahead, these powerful screens are where you start:

Pinpoint undervalued opportunities by using our tool for undervalued stocks based on cash flows and ensure you never miss stocks trading below their real worth.

Target reliable income streams with dividend stocks with yields > 3% and spot companies offering strong dividend yields above 3 percent for your portfolio’s growth and stability.

Tap into the future of medicine with healthcare AI stocks, where innovation in healthcare meets artificial intelligence to reveal leaders in cutting-edge treatments.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks