Advertisement

- Canada

- /

- Telecom Services and Carriers

- /

- TSX:BCE

Here's Why We're Wary Of Buying BCE Inc.'s (TSE:BCE) For Its Upcoming Dividend

Some investors rely on dividends for growing their wealth, and if you're one of those dividend sleuths, you might be intrigued to know that BCE Inc. (TSE:BCE) is about to go ex-dividend in just 4 days. If you purchase the stock on or after the 13th of March, you won't be eligible to receive this dividend, when it is paid on the 15th of April.

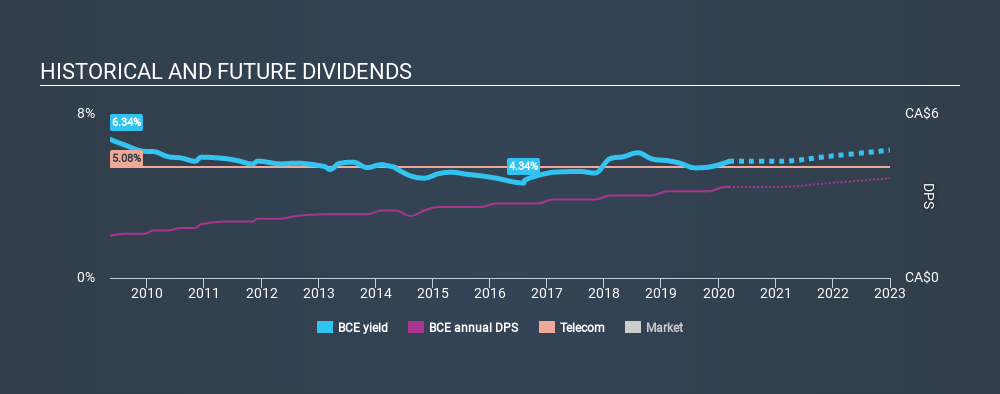

BCE's upcoming dividend is CA$0.83 a share, following on from the last 12 months, when the company distributed a total of CA$3.33 per share to shareholders. Calculating the last year's worth of payments shows that BCE has a trailing yield of 5.3% on the current share price of CA$62.39. We love seeing companies pay a dividend, but it's also important to be sure that laying the golden eggs isn't going to kill our golden goose! That's why we should always check whether the dividend payments appear sustainable, and if the company is growing.

Check out our latest analysis for BCE

Dividends are usually paid out of company profits, so if a company pays out more than it earned then its dividend is usually at greater risk of being cut. Last year, BCE paid out 94% of its income as dividends, which is above a level that we're comfortable with, especially if the company needs to reinvest in its business. A useful secondary check can be to evaluate whether BCE generated enough free cash flow to afford its dividend. Over the last year it paid out 75% of its free cash flow as dividends, within the usual range for most companies.

It's good to see that while BCE's dividends were not well covered by profits, at least they are affordable from a cash perspective. Still, if this were to happen repeatedly, we'd be concerned about whether the dividend is sustainable in a downturn.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with strong growth prospects usually make the best dividend payers, because it's easier to grow dividends when earnings per share are improving. Investors love dividends, so if earnings fall and the dividend is reduced, expect a stock to be sold off heavily at the same time. This is why it's a relief to see BCE earnings per share are up 2.5% per annum over the last five years.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. In the past ten years, BCE has increased its dividend at approximately 8.0% a year on average. It's encouraging to see the company lifting dividends while earnings are growing, suggesting at least some corporate interest in rewarding shareholders.

Final Takeaway

Is BCE worth buying for its dividend? Earnings per share have not grown all that much, and the company is paying out an uncomfortably high percentage of its income. Fortunately it paid out a lower percentage of its cash flow. It's not the most attractive proposition from a dividend perspective, and we'd probably give this one a miss for now.

With that being said, if you're still considering BCE as an investment, you'll find it beneficial to know what risks this stock is facing. Every company has risks, and we've spotted 2 warning signs for BCE (of which 1 shouldn't be ignored!) you should know about.

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSX:BCE

BCE

A communications company, provides wireless, wireline, internet, streaming services, and television (TV) services to residential, business, and wholesale customers in Canada.

Undervalued with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor