Advertisement

- China

- /

- Communications

- /

- SHSE:688387

High Growth Tech Stocks To Watch In January 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets continue to navigate the evolving political landscape and economic indicators, U.S. stocks have been pushing toward record highs, fueled by optimism surrounding softer tariffs and advancements in artificial intelligence. This positive sentiment has particularly benefited growth stocks, which outperformed value shares recently, highlighting the potential for high-growth tech companies to thrive in such an environment. In this context, a good stock to watch would be one that is well-positioned within emerging sectors like AI or other technology-driven industries that are gaining momentum from current market trends and policy developments.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Shanghai Baosight SoftwareLtd | 21.82% | 25.22% | ★★★★★★ |

| eWeLLLtd | 26.41% | 28.82% | ★★★★★★ |

| Ascelia Pharma | 76.15% | 47.16% | ★★★★★★ |

| Waystream Holding | 22.09% | 113.25% | ★★★★★★ |

| Medley | 20.95% | 27.32% | ★★★★★★ |

| Pharma Mar | 25.50% | 55.11% | ★★★★★★ |

| Mental Health TechnologiesLtd | 25.83% | 113.12% | ★★★★★★ |

| Fine M-TecLTD | 36.52% | 135.02% | ★★★★★★ |

| Initiator Pharma | 73.95% | 31.67% | ★★★★★★ |

| Elliptic Laboratories | 61.01% | 121.13% | ★★★★★★ |

Click here to see the full list of 1225 stocks from our High Growth Tech and AI Stocks screener.

Let's review some notable picks from our screened stocks.

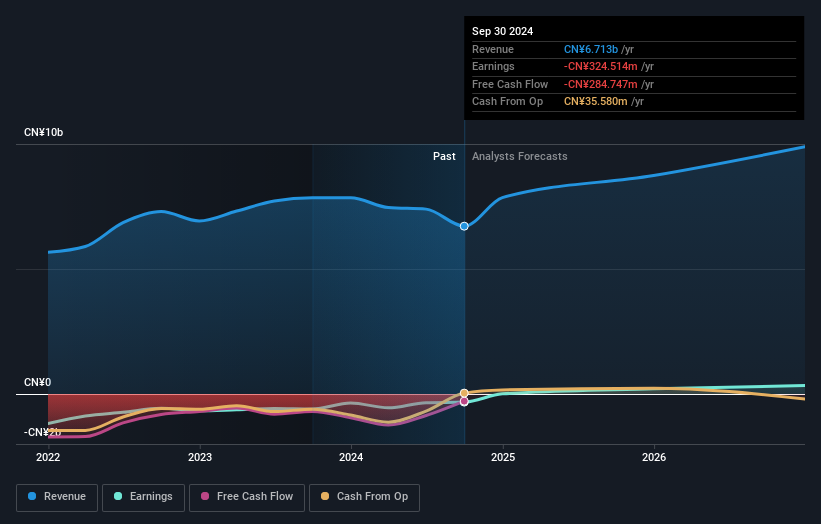

EmbedWay Technologies (Shanghai) (SHSE:603496)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: EmbedWay Technologies (Shanghai) Corporation operates as a network visibility infrastructure and intelligent system platform vendor in China with a market capitalization of CN¥7.05 billion.

Operations: The company generates revenue primarily from its Computer, Communication, and Other Electronic Equipment Manufacturing segment, totaling CN¥1.15 billion. Its operations focus on providing network visibility infrastructure and intelligent system platforms within China.

EmbedWay Technologies (Shanghai) has demonstrated robust financial performance, with a significant uptick in sales reaching CNY 880.94 million, a surge from the previous year's CNY 498.37 million. This growth is complemented by a net income increase to CNY 78.28 million from CNY 31.84 million, reflecting an earnings growth of 96.7%, which notably outpaces the Communications industry's decline of -3%. Looking ahead, EmbedWay is expected to maintain strong momentum with forecasted revenue and earnings growth at annual rates of 18.3% and 33.9%, respectively—both figures surpassing broader market averages in China. This trajectory suggests EmbedWay is not only growing but doing so at an accelerated pace compared to its market peers, underpinned by high-quality earnings that could position it favorably for future advancements within the tech sector.

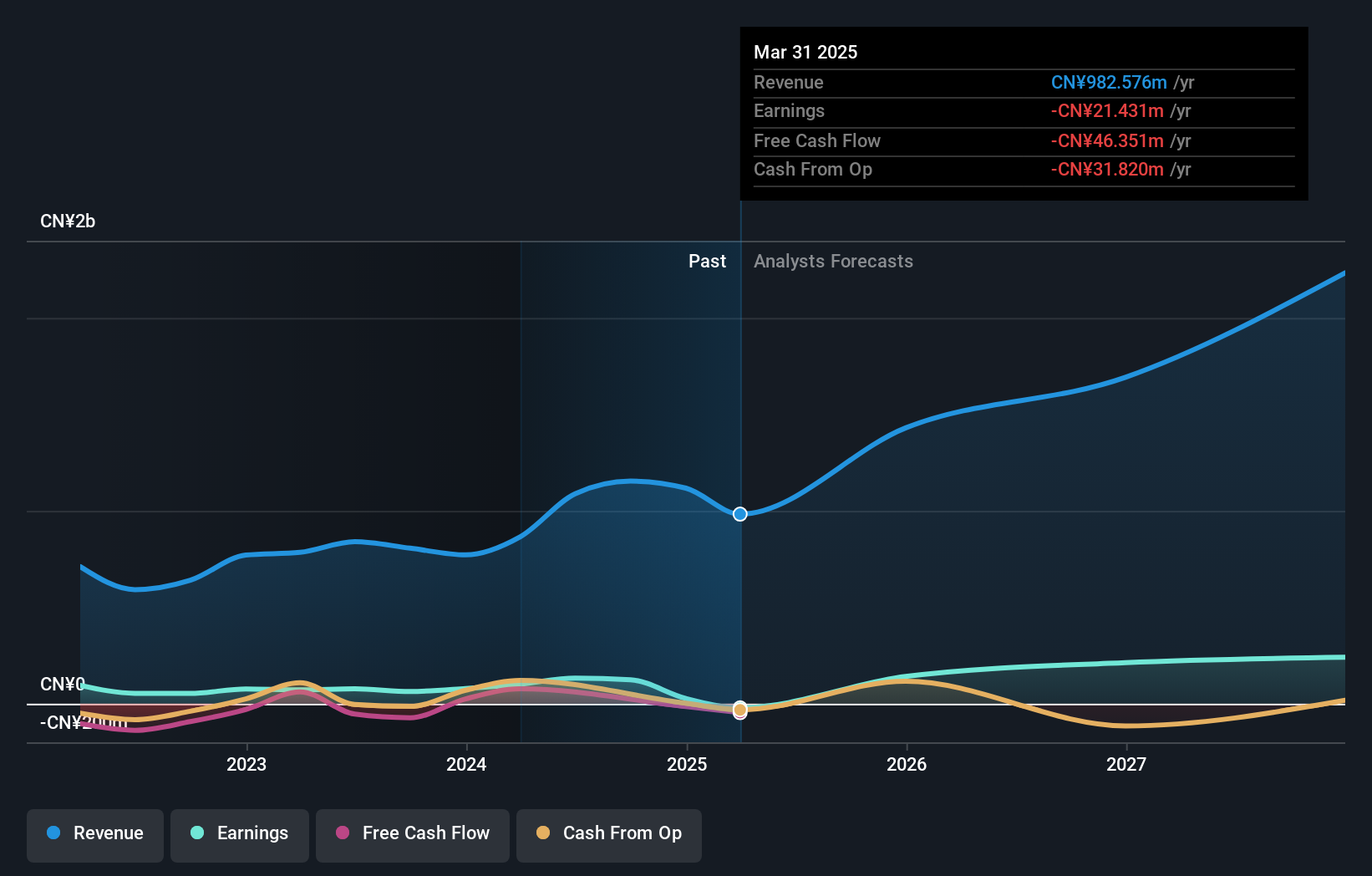

CICT Mobile Communication Technology (SHSE:688387)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: CICT Mobile Communication Technology Co., Ltd. operates in the mobile communication technology sector and has a market capitalization of CN¥19.01 billion.

Operations: CICT Mobile Communication Technology Co., Ltd. generates revenue primarily from its operations in the mobile communication technology sector, with a market capitalization of CN¥19.01 billion. The company's financial performance is characterized by its focus on technological advancements and market expansion within this industry.

CICT Mobile Communication Technology has been navigating a challenging landscape with an unprofitable status but is poised for significant changes. Forecasted to turn profitable within the next three years, the company is expected to outpace the average market growth with earnings projected to surge by 116.5% annually. Despite current challenges, its revenue growth at 15.3% per year exceeds China's market average of 13.4%, signaling potential resilience and upward trajectory in its sector. This growth is underpinned by strategic investments in R&D, crucial for maintaining competitive edge and innovation in high-growth tech environments.

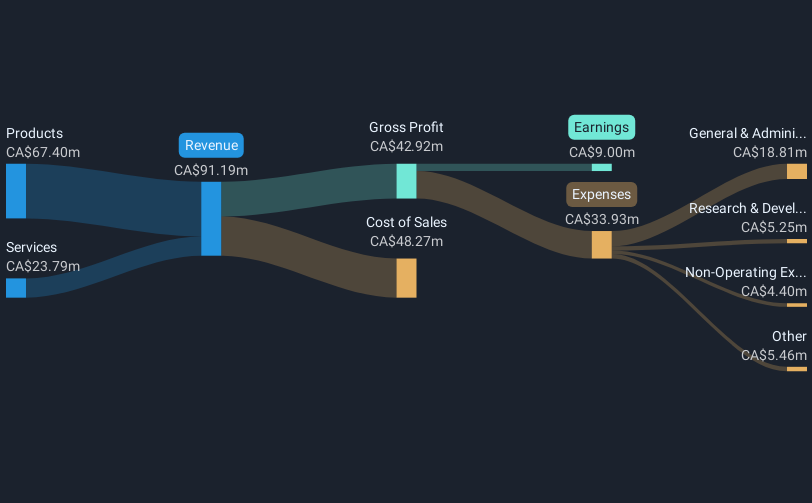

Kraken Robotics (TSXV:PNG)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Kraken Robotics Inc. is a marine technology company that designs, manufactures, and sells sonar and optical sensors, batteries, and underwater robotic equipment for unmanned underwater vehicles used in military and commercial applications worldwide, with a market cap of CA$754.17 million.

Operations: Kraken Robotics generates revenue primarily through its products and services, with CA$67.40 million from product sales and CA$23.79 million from service offerings. The company operates across various regions including Canada, Asia Pacific, Europe, the Middle East, Africa, and North America.

Kraken Robotics, despite a slight dip in quarterly revenue to CAD 19.55 million from CAD 20.34 million year-over-year, has demonstrated robust annual growth with nine-month revenues jumping from CAD 41.58 million to CAD 63.18 million, an indicator of significant market traction. This growth is coupled with a net income increase to CAD 6.42 million from CAD 2.96 million over the same period, reflecting a strong earnings surge by approximately 117%. The company's recent unveiling of its advanced Autonomous Launch and Recovery System (ALARS) for KATFISH™ highlights its commitment to innovation and positions it well within the naval tech sector, potentially enhancing future revenue streams as it begins deliveries to an Asia-Pacific naval customer by year-end.

- Unlock comprehensive insights into our analysis of Kraken Robotics stock in this health report.

Evaluate Kraken Robotics' historical performance by accessing our past performance report.

Taking Advantage

- Delve into our full catalog of 1225 High Growth Tech and AI Stocks here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:688387

CICT Mobile Communication Technology

CICT Mobile Communication Technology Co., Ltd.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|32.0% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|21.7% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|0.5% overvalued

DA

Community Contributor