Advertisement

Here's Why Kraken Robotics (CVE:PNG) Might Be Better Off Without Debt

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. As with many other companies. Kraken Robotics Inc. (CVE:PNG) makes use of debt. But is this debt a concern to shareholders?

What Risk Does Debt Bring?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we think about a company's use of debt, we first look at cash and debt together.

Check out our latest analysis for Kraken Robotics

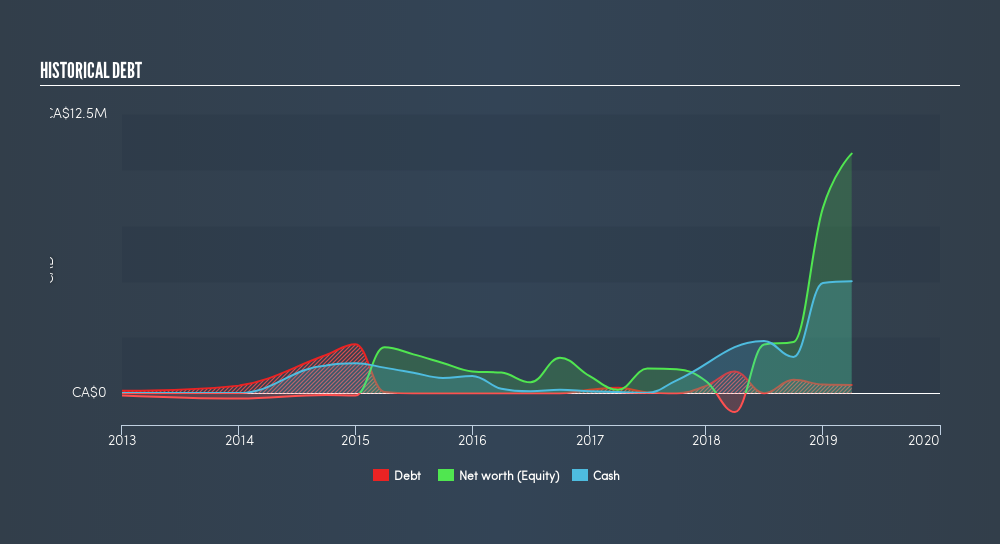

What Is Kraken Robotics's Net Debt?

As you can see below, Kraken Robotics had CA$371.0k of debt at March 2019, down from CA$966.7k a year prior. However, it does have CA$5.01m in cash offsetting this, leading to net cash of CA$4.64m.

How Strong Is Kraken Robotics's Balance Sheet?

We can see from the most recent balance sheet that Kraken Robotics had liabilities of CA$5.72m falling due within a year, and liabilities of CA$2.28m due beyond that. Offsetting these obligations, it had cash of CA$5.01m as well as receivables valued at CA$2.97m due within 12 months. So its total liabilities are just about perfectly matched by its shorter-term, liquid assets.

This state of affairs indicates that Kraken Robotics's balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So it's very unlikely that the CA$83.2m company is short on cash, but still worth keeping an eye on the balance sheet. Kraken Robotics boasts net cash, so it's fair to say it does not have a heavy debt load! When analysing debt levels, the balance sheet is the obvious place to start. But it is future earnings, more than anything, that will determine Kraken Robotics's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Over 12 months, Kraken Robotics reported revenue of CA$8.1m, which is a gain of 146%. So there's no doubt that shareholders are cheering for growth

So How Risky Is Kraken Robotics?

We have no doubt that loss making companies are, in general, riskier than profitable ones. Anf the fact is that over the last twelve months Kraken Robotics lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of CA$7.3m and booked a CA$2.0m accounting loss. With only CA$5.0m on the balance sheet, it would appear that its going to need to raise capital again soon. The good news for shareholders is that Kraken Robotics has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. High growth pre-profit companies may well be risky, but they can also offer great rewards. When I consider a company to be a bit risky, I think it is responsible to check out whether insiders have been reporting any share sales. Luckily, you can click here ito see our graphic depicting Kraken Robotics insider transactions.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSXV:PNG

Kraken Robotics

A marine technology company, engages in the design, manufacture, and sale of sonar and optical sensors, batteries, and underwater robotic equipment for unmanned underwater vehicles used in military and commercial applications in Canada, the Asia Pacific, Europe, the Middle East, Africa, North America, and internationally.

Proven track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|8.8% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.1% undervalued

BL

Community Contributor