Advertisement

Celestica (TSX:CLS) Is Up 15.2% After Raising 2025 Revenue Guidance and Posting Strong Q2 Results – Has The Bull Case Changed?

Simply Wall St

Reviewed by Simply Wall St

- Celestica recently announced strong second-quarter results, with sales rising to US$2.89 billion and net income reaching US$211 million, while also raising its full-year revenue guidance for 2025 to US$11.55 billion.

- This growth in revenue and earnings, combined with new board expertise and continued share buybacks, signals positive momentum amid robust demand for Celestica’s technology solutions.

- We will explore how Celestica’s raised revenue outlook and earnings growth enhance its investment narrative and future growth potential.

Explore 26 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Celestica Investment Narrative Recap

To be a shareholder in Celestica, you need to believe that ongoing demand for advanced networking and AI infrastructure among hyperscalers will result in sustained revenue and earnings growth, while the company continues to navigate its high customer concentration risk. Recent strong Q2 results and the appointment of Chris Colpitts to the board reinforce Celestica’s focus on scale and expertise, but these changes do not materially shift the near-term catalyst, which remains tied to large customer spending and AI-related demand, nor do they significantly alter the main risk: exposure to top customer order patterns.

The most interesting recent announcement is Celestica’s completion of a 1.2 million share buyback for US$115.97 million. This move may enhance shareholder returns, but its significance as a catalyst is limited when compared to the underlying drivers of future revenue growth, namely, the pace of hyperscaler investment, AI infrastructure adoption, and program ramps.

However, investors should be aware that if one of Celestica's largest customers reduces orders or switches vendors, revenue...

Read the full narrative on Celestica (it's free!)

Celestica's outlook projects $15.7 billion in revenue and $817.8 million in earnings by 2028. This requires 13.9% annual revenue growth and a $279.4 million increase in earnings from the current $538.4 million level.

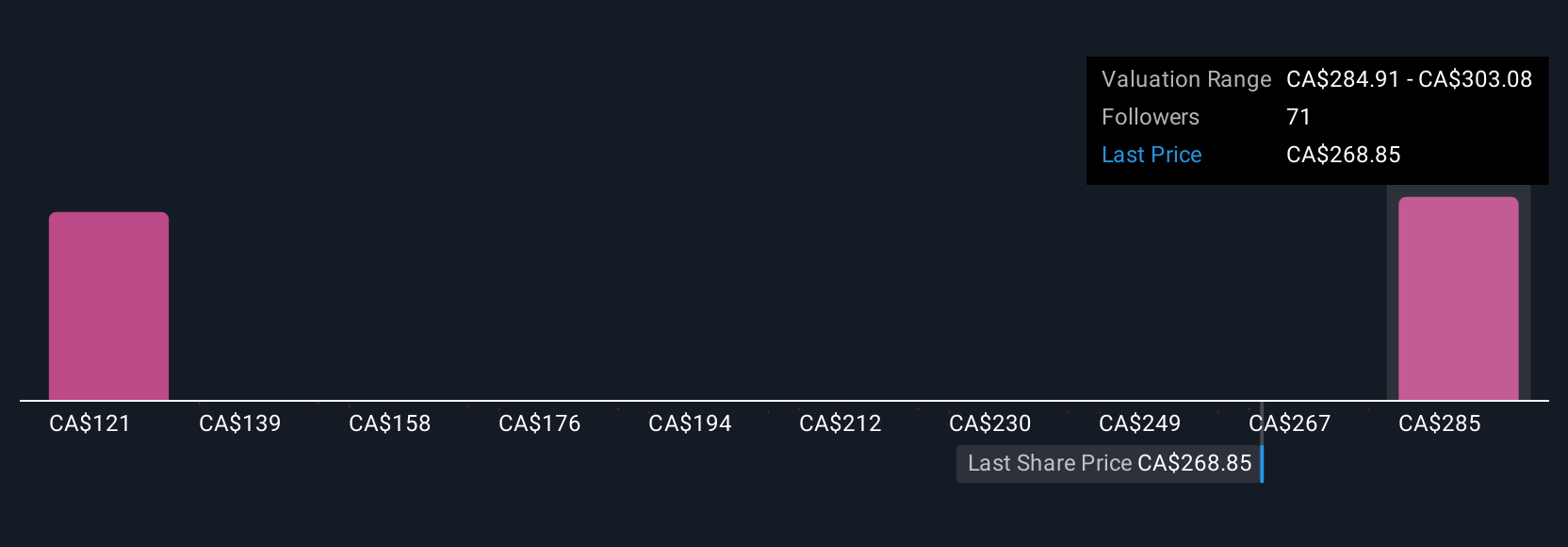

Uncover how Celestica's forecasts yield a CA$303.08 fair value, a 13% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members have set fair value estimates for Celestica ranging from US$121.31 to US$303.08 across 12 analyses. While some see considerable upside, the persistent risk of revenue concentration means a single customer decision could carry broader implications for the company’s performance. Explore these varied perspectives to get a fuller picture of what might come next.

Explore 12 other fair value estimates on Celestica - why the stock might be worth as much as 13% more than the current price!

Build Your Own Celestica Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Celestica research is our analysis highlighting 2 key rewards that could impact your investment decision.

- Our free Celestica research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Celestica's overall financial health at a glance.

Interested In Other Possibilities?

Opportunities like this don't last. These are today's most promising picks. Check them out now:

- Find companies with promising cash flow potential yet trading below their fair value.

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CLS

Celestica

Provides supply chain solutions in Asia, North America, and internationally.

Outstanding track record with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor