Advertisement

Lightspeed Commerce (TSX:LSPD) Is Down 9.5% After Forecasting 10-12% Revenue Growth With Wider Losses

Simply Wall St

Reviewed by Simply Wall St

- Lightspeed Commerce Inc. recently announced its first quarter results for fiscal 2026, reporting sales of US$304.94 million, up from US$266.09 million a year earlier, but with a net loss of US$49.57 million versus a loss of US$35.01 million last year.

- An interesting development is the company’s updated guidance, projecting second-quarter revenue of approximately US$305 million to US$310 million and full-year 2026 revenue growth of 10% to 12%.

- With the outlook now highlighting revenue growth alongside widening net losses, we’ll explore how this guidance shift may impact the investment narrative.

The end of cancer? These 25 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Lightspeed Commerce Investment Narrative Recap

To believe in Lightspeed Commerce as a shareholder, you need conviction in the company’s ability to translate its strong revenue momentum in North America and Europe into durable, profitable growth, despite consistent net losses and ongoing transformation efforts. The recent Q1 results reinforce revenue growth as the near-term catalyst while also spotlighting widening net losses, which remain the most important risk; these results do not materially alter that fundamental dynamic, so the short-term focus remains unchanged.

Among recent developments, the sizable share repurchase completed in May 2025 stands out. The board’s authorization and execution of a buyback, repurchasing over 9 million shares, occurred in parallel with ongoing loss-making quarters, bringing direct relevance to the current investment debate over value versus profitability as a catalyst.

On the other hand, investors should pay close attention to how continued losses could impact the company’s flexibility if...

Read the full narrative on Lightspeed Commerce (it's free!)

Lightspeed Commerce's outlook projects $1.5 billion in revenue and $19.2 million in earnings by 2028. This assumes annual revenue growth of 11.6% and a $686.4 million improvement in earnings from the current level of -$667.2 million.

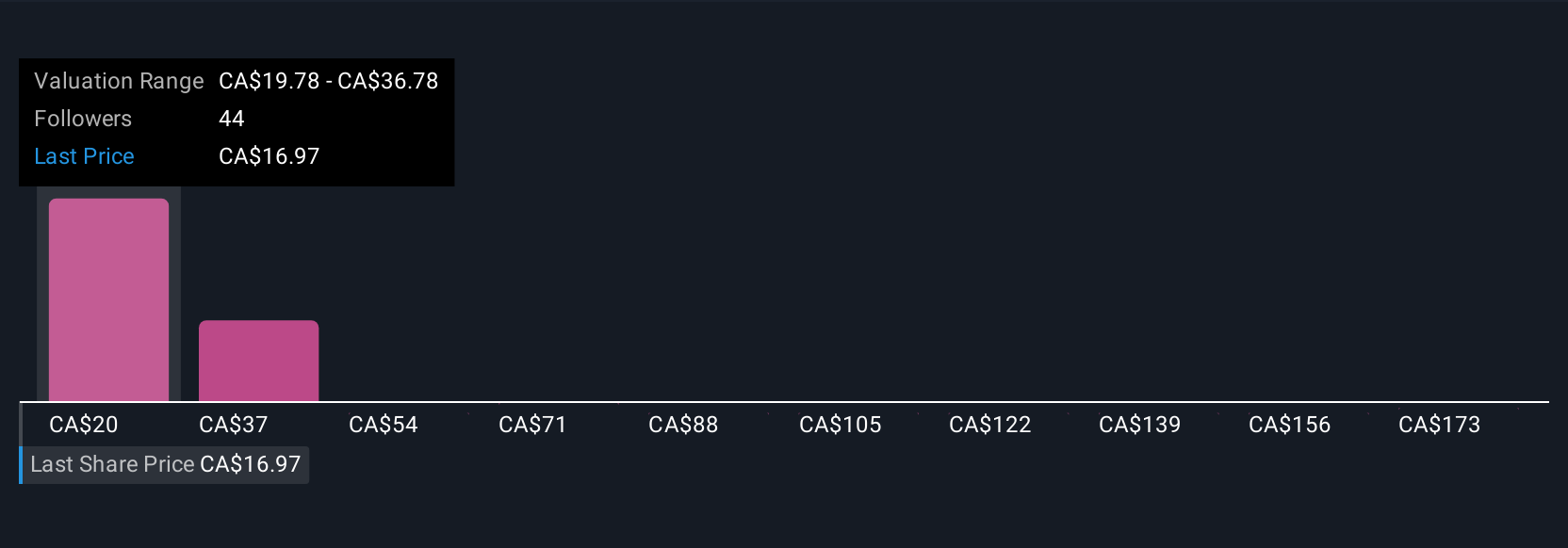

Uncover how Lightspeed Commerce's forecasts yield a CA$19.78 fair value, a 17% upside to its current price.

Exploring Other Perspectives

Nine private investors in the Simply Wall St Community estimate Lightspeed Commerce’s fair value between US$19.78 and US$189.71. While opinions vary, many are weighing recurring net losses against the company’s ongoing revenue growth plans, offering several viewpoints for you to consider.

Explore 9 other fair value estimates on Lightspeed Commerce - why the stock might be a potential multi-bagger!

Build Your Own Lightspeed Commerce Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Lightspeed Commerce research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Lightspeed Commerce research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Lightspeed Commerce's overall financial health at a glance.

No Opportunity In Lightspeed Commerce?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- These 18 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:LSPD

Lightspeed Commerce

Engages in sale of cloud-based software subscriptions and payments solutions for single and multi-location retailers, restaurants, golf course operators, and other businesses in the United States, Canada, the United Kingdom, Australia, and internationally.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor