Advertisement

CGI (TSX:GIB.A): Assessing Valuation after Major U.S. Public Sector Contract Wins

Kshitija Bhandaru

Reviewed by Simply Wall St

CGI (TSX:GIB.A) has just secured a 10-year deal with the State of New Jersey to continue supporting its disaster recovery system, along with a multi-year contract to overhaul Texas’ statewide enterprise financial platform. Both announcements reinforce CGI’s U.S. public sector momentum and signal that the company is strengthening its footprint in mission-critical projects with long-term revenue streams. For investors, this kind of contract pipeline not only boosts confidence in future cash flows but also points to how CGI’s solutions are becoming increasingly embedded in government infrastructure.

After these major wins, it is worth taking stock of how CGI shares have performed. Over the past year, CGI’s share price has declined 12%, in contrast to gains of 32% over three years and nearly 49% over five years. The trend has shifted downward in recent months, but these contracts suggest that underlying growth drivers remain in place, particularly in software and recurring public-sector services. Investors looking at the stock today may note the mix of short-term headwinds and signs of long-term stability taking shape.

Does the recent pullback mean there is a buying opportunity in CGI, or is the market already pricing in years of steady contract-driven growth ahead?

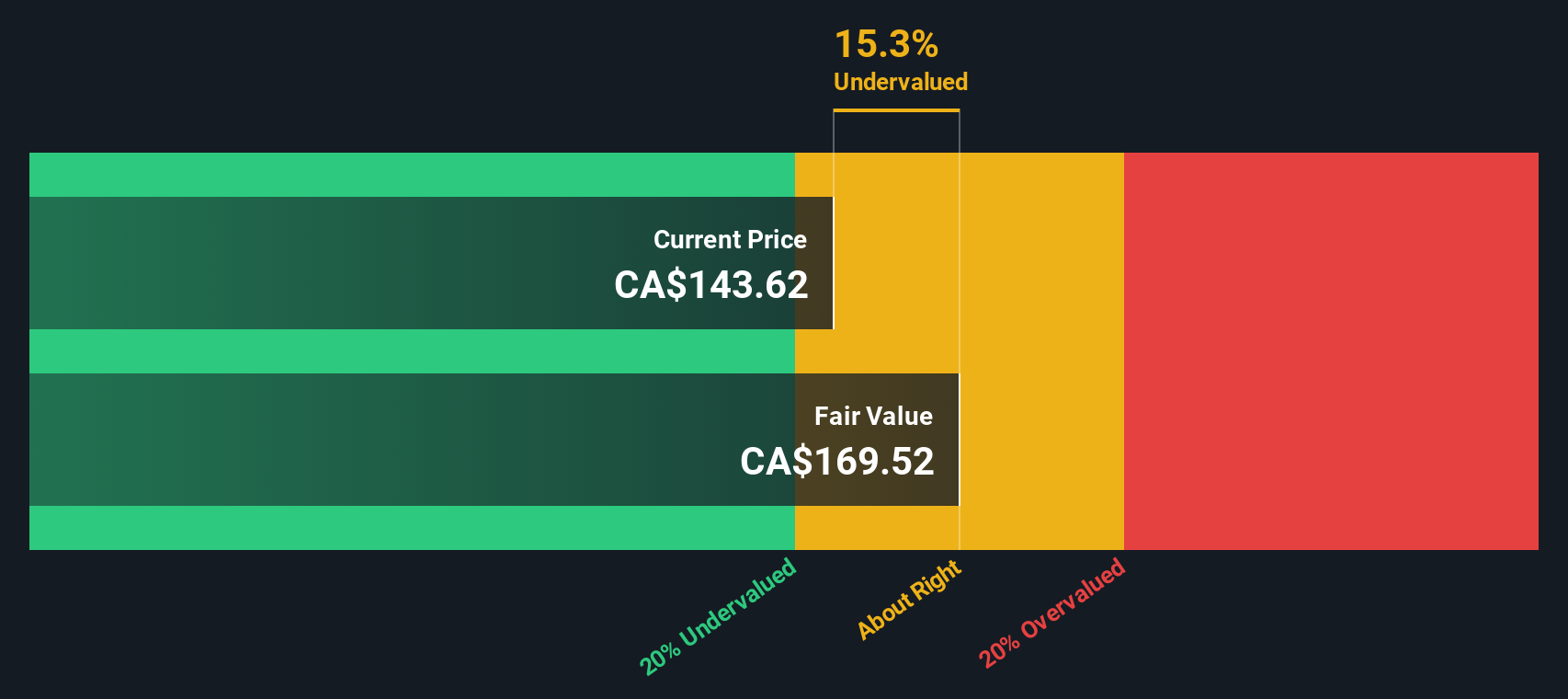

Most Popular Narrative: 22% Undervalued

According to the most widely followed narrative, CGI shares are considered significantly undervalued, trading well below the latest consensus estimate of fair value. Market observers see untapped long-term potential that is not yet fully reflected in today’s price.

Expanding integration of generative AI and automation not only enhances CGI's own IP solutions (now with 40% of IP revenue AI-enabled), but also enables more outcome-based client engagements. This approach leads to operational efficiencies, margin expansion, and improved earnings as AI adoption scales within both CGI and its clients.

How does CGI’s future earnings power support such a sizeable premium? The secret sauce in this valuation is hidden in bold profit margin targets, falling share counts, and a big bet on digital transformation. If you want to know how high analysts are projecting earnings to climb, and what kind of growth must materialize to justify the target, the full narrative reveals the numbers and logic that make this fair value stand out.

Result: Fair Value of $171.17 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, ongoing integration challenges from recent acquisitions and persistent macroeconomic uncertainty could limit CGI’s margin growth and earnings momentum in the near term.

Find out about the key risks to this CGI narrative.Another View: Discounted Cash Flow Model

Taking a different angle, our DCF model also finds CGI undervalued by looking at expected future cash flows rather than just today’s market multiples. Could this extra layer of analysis reveal hidden upside, or is it already priced in?

Look into how the SWS DCF model arrives at its fair value.

Build Your Own CGI Narrative

If you see the numbers differently or want to dig into the data on your own terms, it takes just a few minutes to build your own perspective. Do it your way.

A good starting point is our analysis highlighting 5 key rewards investors are optimistic about regarding CGI.

Looking for More Ways to Strengthen Your Portfolio?

Seize this moment to look beyond CGI and explore a range of investment opportunities designed to boost your returns and diversify your holdings. Here are three angles you will not want to miss:

- Target fast-growing AI disruptors who are shaping new markets by getting the edge with our AI penny stocks.

- Secure ongoing income potential by browsing through companies that offer appealing yields and solid fundamentals, available via our dividend stocks with yields > 3%.

- Spot untapped bargains before the crowd by using our powerful stock finder for those presently undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About TSX:GIB.A

CGI

Provides information technology and business process services in Western and Southern Europe, the United States, Canada, Scandinavia, Northwest and Central-East Europe, the United Kingdom, Australia, Germany, Finland, Poland, Baltics, and the Asia Pacific.

Undervalued with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.4% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.0% undervalued

EA

Community Contributor