Advertisement

- Canada

- /

- Residential REITs

- /

- TSX:MRG.UN

Exploring 3 Undervalued Small Caps In Global With Insider Buying

Simply Wall St

Reviewed by Simply Wall St

As global markets grapple with a range of challenges, including a record U.S. federal government shutdown and declining consumer sentiment, small-cap stocks have been under particular scrutiny amid these turbulent conditions. With the S&P 600 for small-cap stocks experiencing fluctuations, investors are increasingly looking at companies where insider buying may indicate confidence in long-term prospects despite broader market uncertainties. In such an environment, identifying stocks that show potential resilience and growth can be crucial for navigating the current economic landscape.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Bytes Technology Group | 16.0x | 3.9x | 25.24% | ★★★★★☆ |

| Speedy Hire | NA | 0.3x | 27.62% | ★★★★★☆ |

| Senior | 24.7x | 0.8x | 25.68% | ★★★★☆☆ |

| Hung Hing Printing Group | NA | 0.4x | 43.33% | ★★★★☆☆ |

| Sagicor Financial | 7.1x | 0.4x | -66.57% | ★★★★☆☆ |

| Bumitama Agri | 12.4x | 1.8x | 41.09% | ★★★☆☆☆ |

| Ever Sunshine Services Group | 7.0x | 0.4x | -464.01% | ★★★☆☆☆ |

| Eastnine | 11.8x | 7.5x | 49.13% | ★★★☆☆☆ |

| Chinasoft International | 24.3x | 0.8x | -1339.13% | ★★★☆☆☆ |

| GDI Integrated Facility Services | 16.5x | 0.3x | -15.91% | ★★★☆☆☆ |

Underneath we present a selection of stocks filtered out by our screen.

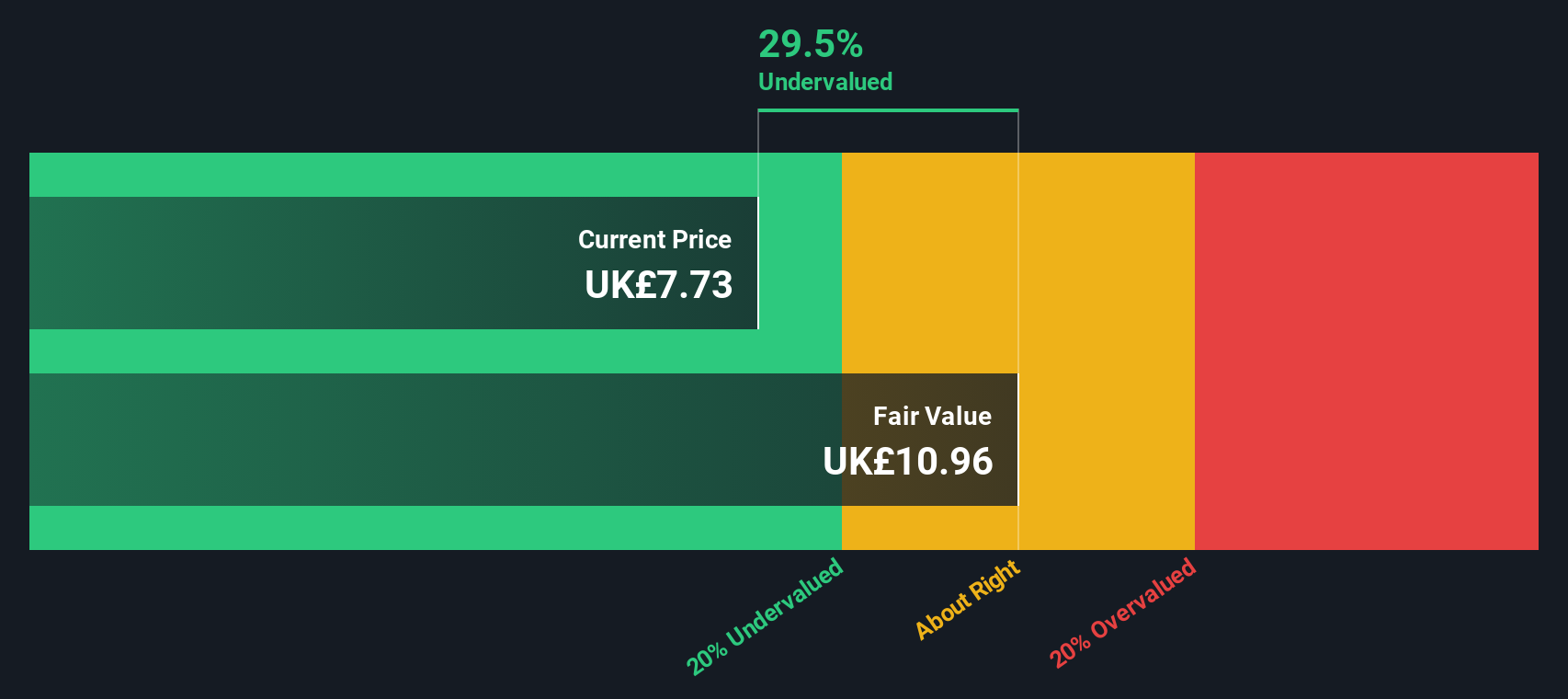

J D Wetherspoon (LSE:JDW)

Simply Wall St Value Rating: ★★★★☆☆

Overview: J D Wetherspoon operates a chain of pubs across the UK and Ireland, with a market cap of approximately £1.18 billion.

Operations: Revenue for JDW is primarily generated from its pubs, with the latest figures showing £2.13 billion. The company has seen fluctuations in its gross profit margin, which reached 11.96% in the most recent period. Operating expenses have been consistently significant, impacting net income margins, which recently stood at 3.20%.

PE: 10.3x

J D Wetherspoon, a smaller company in the hospitality sector, has shown promising sales growth with like-for-like sales up 3.7% for the recent 14-week period and total annual sales rising by 4.2%. The company reported an increase in net income to £67.99 million from £48.79 million last year, reflecting improved profitability despite higher risk funding through external borrowing. Insider confidence is evident with share purchases over the past year, suggesting potential value recognition within its current market position.

- Dive into the specifics of J D Wetherspoon here with our thorough valuation report.

Understand J D Wetherspoon's track record by examining our Past report.

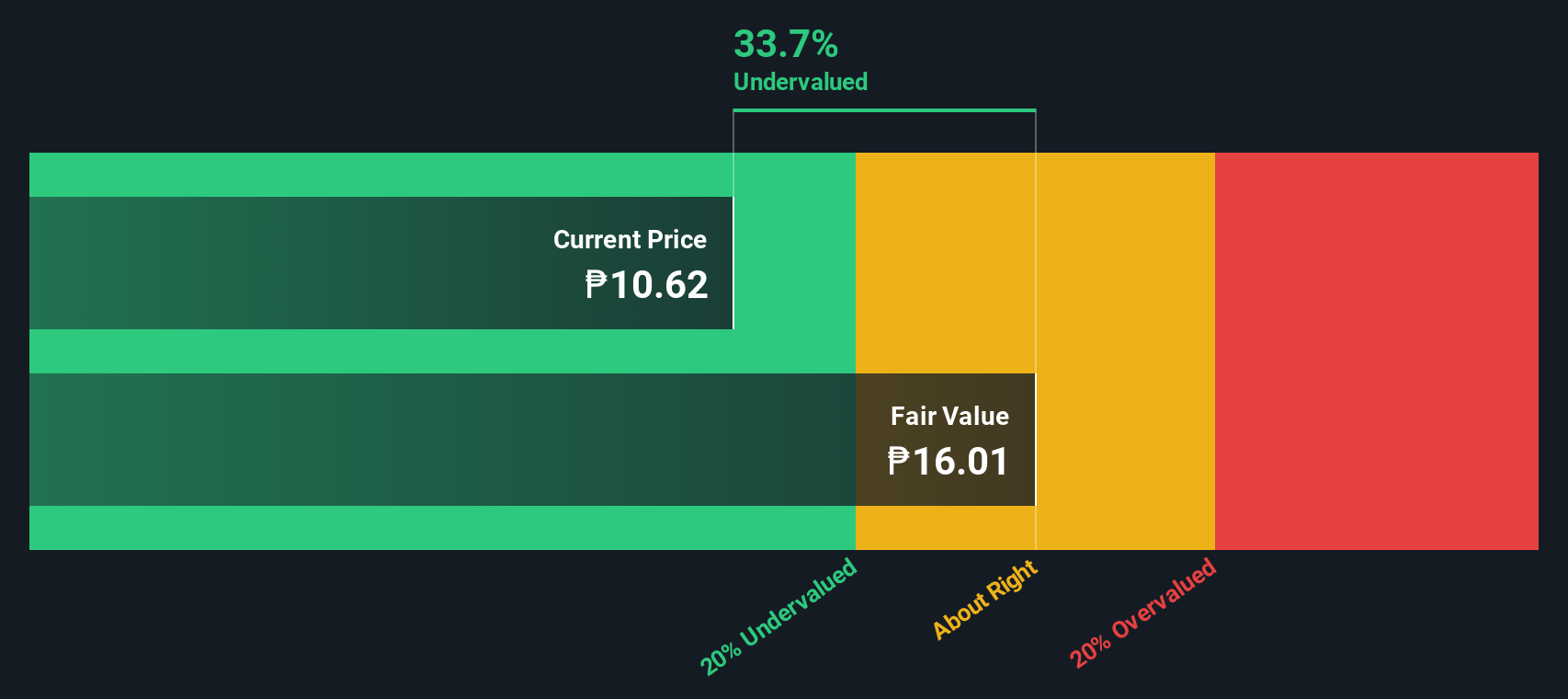

East West Banking (PSE:EW)

Simply Wall St Value Rating: ★★★★☆☆

Overview: East West Banking provides a range of financial services through its retail, consumer, and corporate banking segments, along with treasury and trust operations, with a market capitalization of ₱52.30 billion.

Operations: The primary revenue streams include retail banking, consumer banking, corporate banking, and treasury and trust operations. Over recent periods, the gross profit margin has been consistently high, with a notable figure of 98.96% as of June 2025. Operating expenses are largely driven by general and administrative costs, which reached ₱11.44 billion in the same period.

PE: 3.1x

East West Banking stands out in the small cap category with a forecasted annual earnings growth of 11.88%, suggesting potential for future gains. Despite this, the bank faces challenges with a high bad loans ratio of 4.4% and a low bad loan allowance at 66%. Recent insider confidence is evident as they have been purchasing shares, indicating belief in the company's prospects. The appointment of Ramon Vicente De Vera II as Chief Business Development Officer could drive strategic fintech advancements, enhancing growth opportunities.

- Click here and access our complete valuation analysis report to understand the dynamics of East West Banking.

Assess East West Banking's past performance with our detailed historical performance reports.

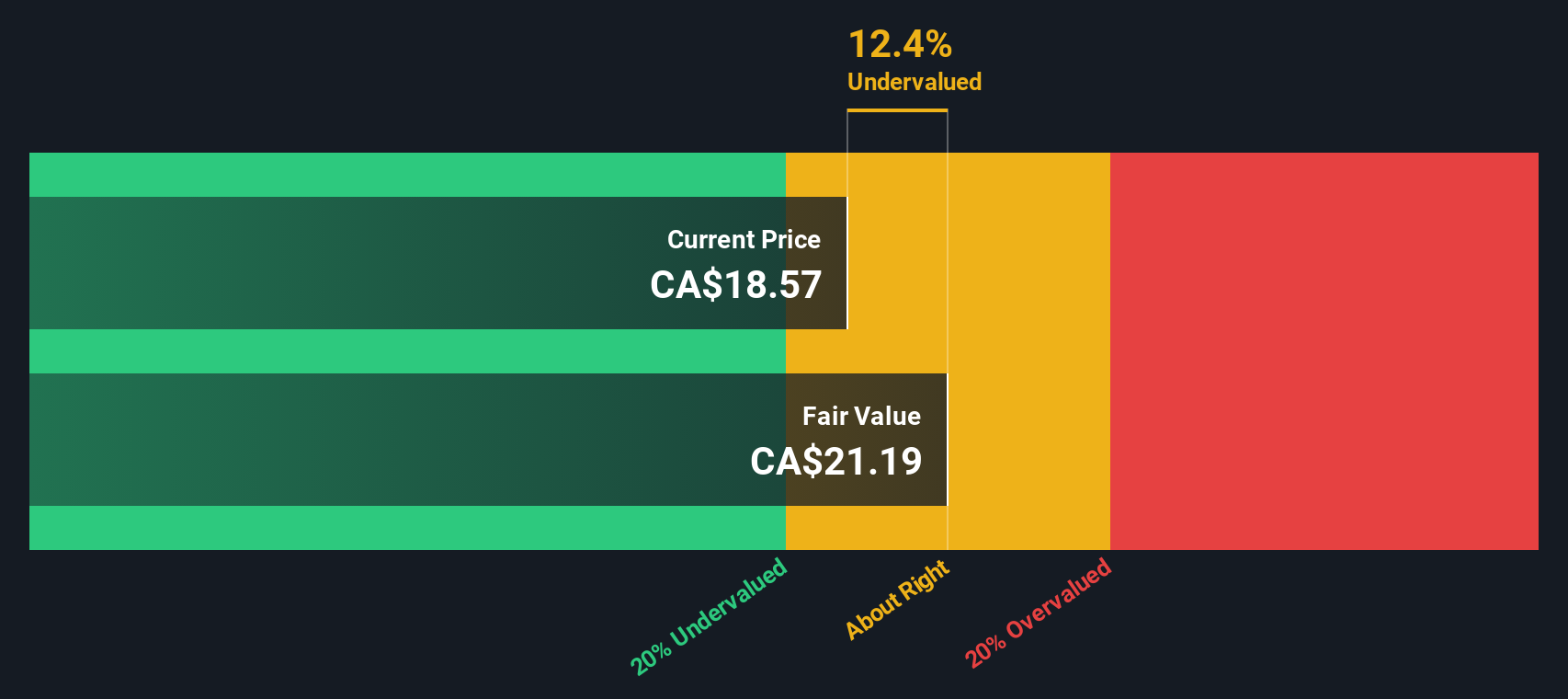

Morguard North American Residential Real Estate Investment Trust (TSX:MRG.UN)

Simply Wall St Value Rating: ★★★★★☆

Overview: Morguard North American Residential Real Estate Investment Trust is focused on owning and operating a diversified portfolio of multi-suite residential real estate properties, with a market cap of approximately CA$1.01 billion.

Operations: The primary revenue stream is from multi-suite residential real estate, generating CA$359.44 million. The gross profit margin has shown fluctuations, reaching 53.16% by the latest period. Operating expenses have been consistently around CA$23 million, impacting net income margins which have varied significantly over time.

PE: 4.9x

Morguard North American Residential Real Estate Investment Trust, a smaller player in the real estate sector, reported CAD 87.66 million in sales for Q3 2025, a slight increase from last year. Net income improved significantly to CAD 7.85 million from a net loss of CAD 20.79 million previously. Despite earnings being impacted by large one-off items and interest payments not fully covered by earnings, insider confidence is suggested through recent share purchases over the past months.

Where To Now?

- Click this link to deep-dive into the 120 companies within our Undervalued Global Small Caps With Insider Buying screener.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:MRG.UN

Morguard North American Residential Real Estate Investment Trust

The REIT is an unincorporated, open-ended real estate investment trust established under and governed by the laws of the Province of Ontario.

Undervalued established dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor