Advertisement

Despite Lacking Profits ProMIS Neurosciences (TSE:PMN) Seems To Be On Top Of Its Debt

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that ProMIS Neurosciences, Inc. (TSE:PMN) does have debt on its balance sheet. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Of course, plenty of companies use debt to fund growth, without any negative consequences. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for ProMIS Neurosciences

What Is ProMIS Neurosciences's Net Debt?

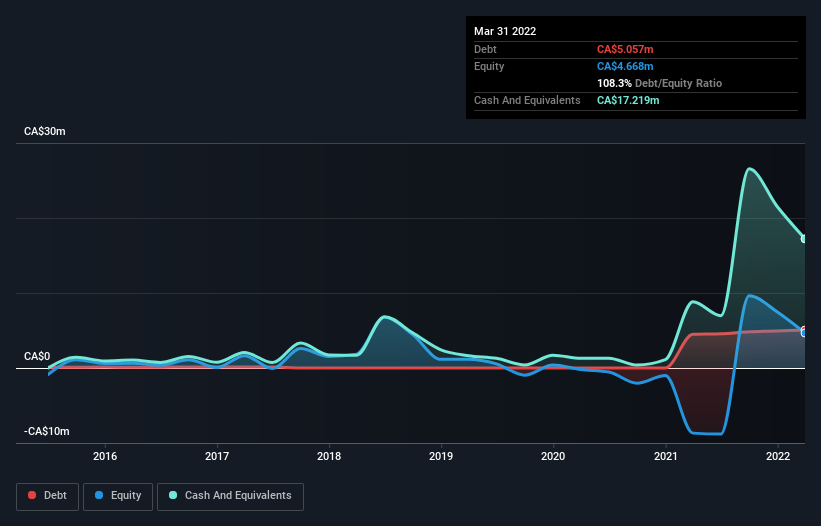

As you can see below, at the end of March 2022, ProMIS Neurosciences had CA$5.06m of debt, up from CA$4.50m a year ago. Click the image for more detail. But on the other hand it also has CA$17.2m in cash, leading to a CA$12.2m net cash position.

How Strong Is ProMIS Neurosciences' Balance Sheet?

According to the last reported balance sheet, ProMIS Neurosciences had liabilities of CA$1.74m due within 12 months, and liabilities of CA$11.6m due beyond 12 months. Offsetting this, it had CA$17.2m in cash and CA$125.9k in receivables that were due within 12 months. So it can boast CA$3.98m more liquid assets than total liabilities.

This surplus suggests that ProMIS Neurosciences has a conservative balance sheet, and could probably eliminate its debt without much difficulty. Succinctly put, ProMIS Neurosciences boasts net cash, so it's fair to say it does not have a heavy debt load! The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine ProMIS Neurosciences's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Since ProMIS Neurosciences doesn't have significant operating revenue, shareholders may be hoping it comes up with a great new product, before it runs out of money.

So How Risky Is ProMIS Neurosciences?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year ProMIS Neurosciences had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of CA$15m and booked a CA$7.3m accounting loss. With only CA$12.2m on the balance sheet, it would appear that its going to need to raise capital again soon. Importantly, ProMIS Neurosciences's revenue growth is hot to trot. High growth pre-profit companies may well be risky, but they can also offer great rewards. There's no doubt that we learn most about debt from the balance sheet. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 6 warning signs for ProMIS Neurosciences you should be aware of, and 3 of them are a bit unpleasant.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:PMN

ProMIS Neurosciences

ProMIS Neurosciences, Inc. discovers and develops antibody therapies and therapeutic vaccines neurodegenerative diseases and other misfolded protein diseases in Canada.

Slightly overvalued with worrying balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|37.1% undervalued

UN

Community Contributor