Advertisement

Analysts Have Been Trimming Their HEXO Corp. (TSE:HEXO) Price Target After Its Latest Report

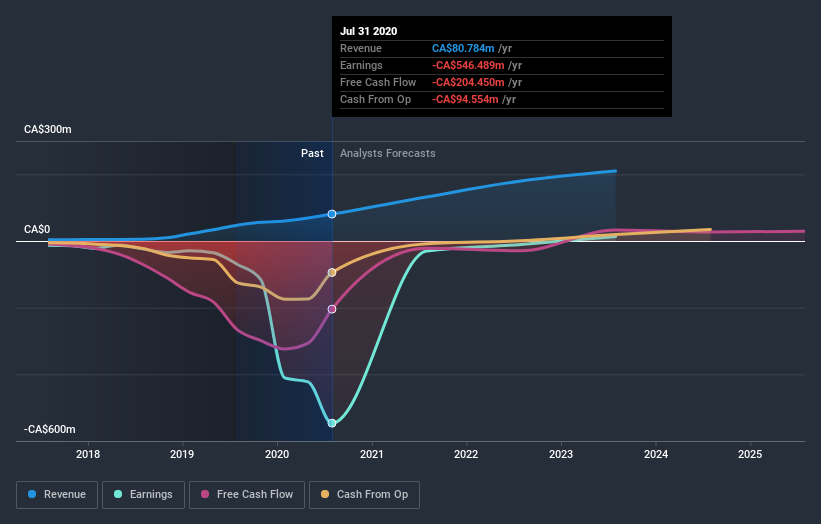

There's been a notable change in appetite for HEXO Corp. (TSE:HEXO) shares in the week since its annual report, with the stock down 13% to CA$0.81. It was a pretty bad result overall; while revenues were in line with expectations at CA$81m, statutory losses exploded to CA$1.77 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. With this in mind, we've gathered the latest statutory forecasts to see what the analysts are expecting for next year.

View our latest analysis for HEXO

Following the latest results, HEXO's twelve analysts are now forecasting revenues of CA$131.9m in 2021. This would be a substantial 63% improvement in sales compared to the last 12 months. Losses are predicted to fall substantially, shrinking 96% to CA$0.068. Yet prior to the latest earnings, the analysts had been forecasting revenues of CA$133.2m and losses of CA$0.062 per share in 2021. So it's pretty clear the analysts have mixed opinions on HEXO even after this update; although they reconfirmed their revenue numbers, it came at the cost of a per-share losses.

The consensus price target fell 17% to CA$1.03per share, with the analysts clearly concerned by ballooning losses. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. Currently, the most bullish analyst values HEXO at CA$1.75 per share, while the most bearish prices it at CA$0.75. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

One way to get more context on these forecasts is to look at how they compare to both past performance, and how other companies in the same industry are performing. We can infer from the latest estimates that forecasts expect a continuation of HEXO'shistorical trends, as next year's 63% revenue growth is roughly in line with 73% annual revenue growth over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to see their revenues grow 32% per year. So it's pretty clear that HEXO is forecast to grow substantially faster than its industry.

The Bottom Line

The most important thing to note is the forecast of increased losses next year, suggesting all may not be well at HEXO. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of HEXO's future valuation.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. We have forecasts for HEXO going out to 2023, and you can see them free on our platform here.

And what about risks? Every company has them, and we've spotted 3 warning signs for HEXO (of which 1 can't be ignored!) you should know about.

If you decide to trade HEXO, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if HEXO might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About TSX:HEXO

HEXO

HEXO Corp., together with its subsidiaries, produces, markets, and sells cannabis in Canada.

Good value with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor