Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that XPhyto Therapeutics Corp. (CSE:XPHY) does use debt in its business. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for XPhyto Therapeutics

How Much Debt Does XPhyto Therapeutics Carry?

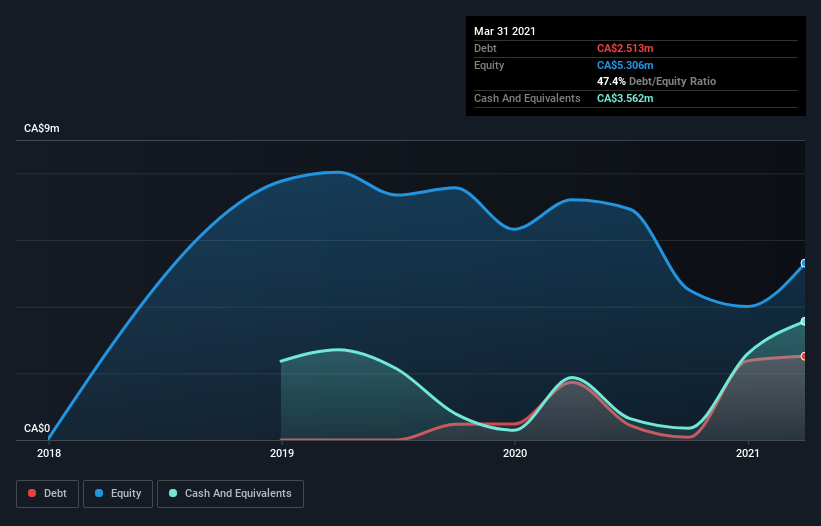

As you can see below, at the end of March 2021, XPhyto Therapeutics had CA$2.51m of debt, up from CA$1.73m a year ago. Click the image for more detail. However, it does have CA$3.56m in cash offsetting this, leading to net cash of CA$1.05m.

A Look At XPhyto Therapeutics' Liabilities

We can see from the most recent balance sheet that XPhyto Therapeutics had liabilities of CA$1.13m falling due within a year, and liabilities of CA$2.80m due beyond that. Offsetting these obligations, it had cash of CA$3.56m as well as receivables valued at CA$408.7k due within 12 months. So these liquid assets roughly match the total liabilities.

This state of affairs indicates that XPhyto Therapeutics' balance sheet looks quite solid, as its total liabilities are just about equal to its liquid assets. So while it's hard to imagine that the CA$129.8m company is struggling for cash, we still think it's worth monitoring its balance sheet. Simply put, the fact that XPhyto Therapeutics has more cash than debt is arguably a good indication that it can manage its debt safely. The balance sheet is clearly the area to focus on when you are analysing debt. But it is XPhyto Therapeutics's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

It seems likely shareholders hope that XPhyto Therapeutics can significantly advance the business plan before too long, because it doesn't have any significant revenue at the moment.

So How Risky Is XPhyto Therapeutics?

By their very nature companies that are losing money are more risky than those with a long history of profitability. And we do note that XPhyto Therapeutics had an earnings before interest and tax (EBIT) loss, over the last year. And over the same period it saw negative free cash outflow of CA$12m and booked a CA$19m accounting loss. Given it only has net cash of CA$1.05m, the company may need to raise more capital if it doesn't reach break-even soon. Overall, its balance sheet doesn't seem overly risky, at the moment, but we're always cautious until we see the positive free cash flow. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 5 warning signs for XPhyto Therapeutics you should be aware of, and 3 of them are significant.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if BioNxt Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About CNSX:BNXT

BioNxt Solutions

Engages in R&D and manufacturing of thin-film (sublingual) and skin patch (transdermal) drug delivery for neurological and autoimmune diseases, enhancing patient compliance and bioavailability.

Low with imperfect balance sheet.

Market Insights

Community Narratives