Advertisement

Results: Green Thumb Industries Inc. Exceeded Expectations And The Consensus Has Updated Its Estimates

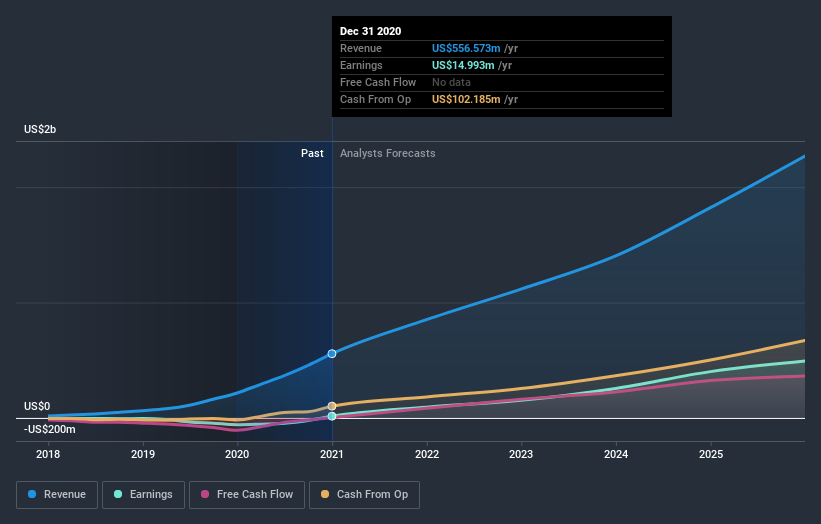

Last week saw the newest full-year earnings release from Green Thumb Industries Inc. (CSE:GTII), an important milestone in the company's journey to build a stronger business. Revenues were US$557m, approximately in line with whatthe analysts expected, although statutory earnings per share (EPS) crushed expectations, coming in at US$0.07, an impressive 124% ahead of estimates. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. So we gathered the latest post-earnings forecasts to see what estimates suggest is in store for next year.

See our latest analysis for Green Thumb Industries

Taking into account the latest results, the current consensus from Green Thumb Industries' 18 analysts is for revenues of US$851.5m in 2021, which would reflect a substantial 53% increase on its sales over the past 12 months. Green Thumb Industries is also expected to turn profitable, with statutory earnings of US$0.41 per share. Yet prior to the latest earnings, the analysts had been anticipated revenues of US$827.2m and earnings per share (EPS) of US$0.41 in 2021. So it looks like there's been no major change in sentiment following the latest results, although the analysts have made a modest lift to to revenue forecasts.

The analysts increased their price target 12% to US$44.06, perhaps signalling that higher revenues are a strong leading indicator for Green Thumb Industries's valuation. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. There are some variant perceptions on Green Thumb Industries, with the most bullish analyst valuing it at US$72.70 and the most bearish at US$42.78 per share. This is a fairly broad spread of estimates, suggesting that analysts are forecasting a wide range of possible outcomes for the business.

Taking a look at the bigger picture now, one of the ways we can understand these forecasts is to see how they compare to both past performance and industry growth estimates. It's pretty clear that there is an expectation that Green Thumb Industries' revenue growth will slow down substantially, with revenues to the end of 2021 expected to display 53% growth on an annualised basis. This is compared to a historical growth rate of 92% over the past three years. By way of comparison, the other companies in this industry with analyst coverage are forecast to grow their revenue at 32% annually. So it's pretty clear that, while Green Thumb Industries' revenue growth is expected to slow, it's still expected to grow faster than the industry itself.

The Bottom Line

The most important thing to take away is that there's been no major change in sentiment, with the analysts reconfirming that the business is performing in line with their previous earnings per share estimates. Pleasantly, they also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow faster than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Green Thumb Industries analysts - going out to 2025, and you can see them free on our platform here.

That said, it's still necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Green Thumb Industries , and understanding these should be part of your investment process.

If you decide to trade Green Thumb Industries, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About CNSX:GTII

Green Thumb Industries

Manufactures, distributes, markets, and sells of cannabis products for medical and adult-use in the United States.

Adequate balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor