Advertisement

Curaleaf Holdings (CNSX:CURA) Seems To Be Really Weighed Down By Its Debt

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Curaleaf Holdings, Inc. (CNSX:CURA) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Curaleaf Holdings

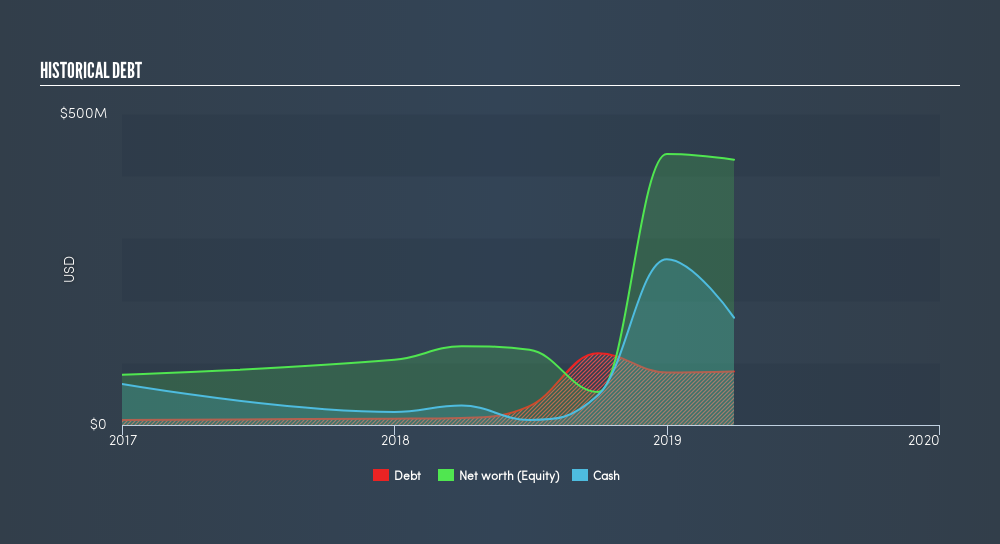

What Is Curaleaf Holdings's Debt?

You can click the graphic below for the historical numbers, but it shows that as of March 2019 Curaleaf Holdings had US$85.9m of debt, an increase on US$11.3m, over one year. But it also has US$172.6m in cash to offset that, meaning it has US$86.7m net cash.

How Strong Is Curaleaf Holdings's Balance Sheet?

The latest balance sheet data shows that Curaleaf Holdings had liabilities of US$26.2m due within a year, and liabilities of US$148.6m falling due after that. Offsetting this, it had US$172.6m in cash and US$11.7m in receivables that were due within 12 months. So it actually has US$9.55m more liquid assets than total liabilities.

Having regard to Curaleaf Holdings's size, it seems that its liquid assets are well balanced with its total liabilities. So while it's hard to imagine that the US$3.16b company is struggling for cash, we still think it's worth monitoring its balance sheet. Given that Curaleaf Holdings has more cash than debt, we're pretty confident it can manage its debt safely. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately the future profitability of the business will decide if Curaleaf Holdings can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Curaleaf Holdings managed to grow its revenue by 308%, to US$103m. When it comes to revenue growth, that's like nailing the game winning 3-pointer!

So How Risky Is Curaleaf Holdings?

Statistically speaking companies that lose money are riskier than those that make money. Anf the fact is that over the last twelve months Curaleaf Holdings lost money at the earnings before interest and tax (EBIT) line. And over the same period it saw negative free cash outflow of US$102m and booked a US$64m accounting loss. However, it has net cash of US$173m, so it has a bit of time before it will need more capital. The good news for shareholders is that Curaleaf Holdings has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. While unprofitable companies can be risky, they can also grow hard and fast in those pre-profit years. When we look at a riskier company, we like to check how their profits (or losses) are trending over time. Today, we're providing readers this interactive graph showing how Curaleaf Holdings's profit, revenue, and operating cashflow have changed over the last few years.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:CURA

Curaleaf Holdings

Produces and distributes cannabis products in the United States and internationally.

Undervalued with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor