Advertisement

- Canada

- /

- Metals and Mining

- /

- TSXV:MGM

We're Not Very Worried About Maple Gold Mines's (CVE:MGM) Cash Burn Rate

We can readily understand why investors are attracted to unprofitable companies. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. Nonetheless, only a fool would ignore the risk that a loss making company burns through its cash too quickly.

So should Maple Gold Mines (CVE:MGM) shareholders be worried about its cash burn? For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

View our latest analysis for Maple Gold Mines

When Might Maple Gold Mines Run Out Of Money?

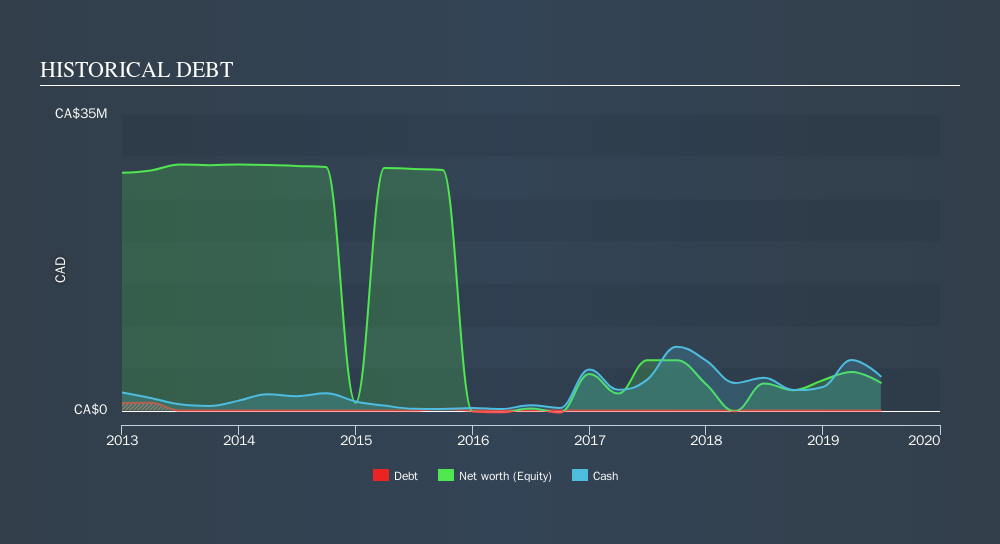

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. As at June 2019, Maple Gold Mines had cash of CA$4.0m and no debt. Importantly, its cash burn was CA$1.8m over the trailing twelve months. That means it had a cash runway of about 2.2 years as of June 2019. Arguably, that's a prudent and sensible length of runway to have. You can see how its cash balance has changed over time in the image below.

How Is Maple Gold Mines's Cash Burn Changing Over Time?

Maple Gold Mines didn't record any revenue over the last year, indicating that it's an early stage company still developing its business. Nonetheless, we can still examine its cash burn trajectory as part of our assessment of its cash burn situation. The 85% reduction in its cash burn over the last twelve months may be good for protecting the balance sheet but it hardly points to imminent growth. Maple Gold Mines makes us a little nervous due to its lack of substantial operating revenue. We prefer most of the stocks on this list of stocks that analysts expect to grow.

How Easily Can Maple Gold Mines Raise Cash?

There's no doubt Maple Gold Mines's rapidly reducing cash burn brings comfort, but even if it's only hypothetical, it's always worth asking how easily it could raise more money to fund further growth. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Commonly, a business will sell new shares in itself to raise cash to drive growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Since it has a market capitalisation of CA$20m, Maple Gold Mines's CA$1.8m in cash burn equates to about 9.0% of its market value. That's a low proportion, so we figure the company would be able to raise more cash to fund growth, with a little dilution, or even to simply borrow some money.

So, Should We Worry About Maple Gold Mines's Cash Burn?

As you can probably tell by now, we're not too worried about Maple Gold Mines's cash burn. In particular, we think its cash burn reduction stands out as evidence that the company is well on top of its spending. But it's fair to say that its cash burn relative to its market cap was also very reassuring. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash, as it seems on track to meet its needs over the medium term. When you don't have traditional metrics like earnings per share and free cash flow to value a company, many are extra motivated to consider qualitative factors such as whether insiders are buying or selling shares. Please Note: Maple Gold Mines insiders have been trading shares, according to our data. Click here to check whether insiders have been buying or selling.

Of course Maple Gold Mines may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSXV:MGM

Moderate with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.1% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|20.9% undervalued

TI

Community Contributor