Advertisement

- Canada

- /

- Metals and Mining

- /

- TSXV:GGM

Those Who Purchased Granada Gold Mine (CVE:GGM) Shares Three Years Ago Have A 71% Loss To Show For It

It is a pleasure to report that the Granada Gold Mine Inc. (CVE:GGM) is up 45% in the last quarter. But only the myopic could ignore the astounding decline over three years. To wit, the share price sky-dived 71% in that time. So it's about time shareholders saw some gains. Of course the real question is whether the business can sustain a turnaround.

View our latest analysis for Granada Gold Mine

With just CA$206,970 worth of revenue in twelve months, we don't think the market considers Granada Gold Mine to have proven its business plan. We can't help wondering why it's publicly listed so early in its journey. Are venture capitalists not interested? So it seems shareholders are too busy dreaming about the progress to come than dwelling on the current (lack of) revenue. It seems likely some shareholders believe that Granada Gold Mine will find or develop a valuable new mine before too long.

We think companies that have neither significant revenues nor profits are pretty high risk. There is almost always a chance they will need to raise more capital, and their progress - and share price - will dictate how dilutive that is to current holders. While some such companies do very well over the long term, others become hyped up by promoters before eventually falling back down to earth, and going bankrupt (or being recapitalized). It certainly is a dangerous place to invest, as Granada Gold Mine investors might realise.

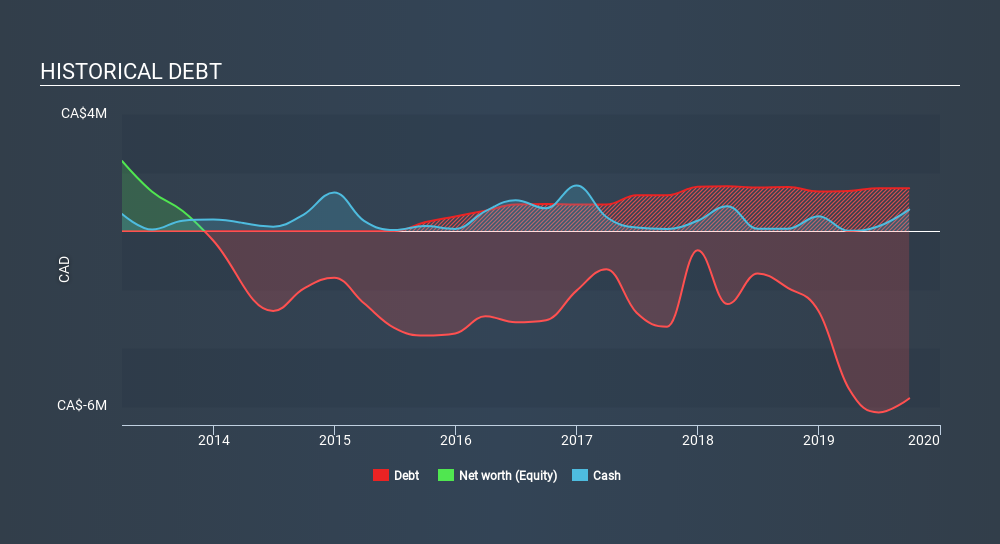

Granada Gold Mine had liabilities exceeding cash by CA$6.3m when it last reported in September 2019, according to our data. That puts it in the highest risk category, according to our analysis. But with the share price diving 34% per year, over 3 years , it's probably fair to say that some shareholders no longer believe the company will succeed. The image below shows how Granada Gold Mine's balance sheet has changed over time; if you want to see the precise values, simply click on the image. You can click on the image below to see (in greater detail) how Granada Gold Mine's cash levels have changed over time.

In reality it's hard to have much certainty when valuing a business that has neither revenue or profit. What if insiders are ditching the stock hand over fist? I'd like that just about as much as I like to drink milk and fruit juice mixed together. You can click here to see if there are insiders selling.

What about the Total Shareholder Return (TSR)?

We've already covered Granada Gold Mine's share price action, but we should also mention its total shareholder return (TSR). The TSR is a return calculation that accounts for the value of cash dividends (assuming that any dividend received was reinvested) and the calculated value of any discounted capital raisings and spin-offs. We note that Granada Gold Mine's TSR, at -71% is higher than its share price return of -71%. When you consider it hasn't been paying a dividend, this data suggests shareholders have benefitted from a spin-off, or had the opportunity to acquire attractively priced shares in a discounted capital raising.

A Different Perspective

While the broader market gained around 10% in the last year, Granada Gold Mine shareholders lost 22%. Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. Regrettably, last year's performance caps off a bad run, with the shareholders facing a total loss of 14% per year over five years. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. It's always interesting to track share price performance over the longer term. But to understand Granada Gold Mine better, we need to consider many other factors. Take risks, for example - Granada Gold Mine has 5 warning signs (and 3 which make us uncomfortable) we think you should know about.

If you would prefer to check out another company -- one with potentially superior financials -- then do not miss this free list of companies that have proven they can grow earnings.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on CA exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.

About TSXV:GGM

Granada Gold Mine

A junior mining and exploration company, acquires, explores for, and develops mineral properties in Canada.

Slight with imperfect balance sheet.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|40.2% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|62.7% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.1% undervalued

UN

Community Contributor