- Canada

- /

- Metals and Mining

- /

- TSXV:BKM

TSX Penny Stocks To Watch In January 2025

Reviewed by Simply Wall St

As we step into 2025, the Canadian market is buoyed by a familiar supportive backdrop, with the TSX having gained 18% in 2024 and investors eyeing potential growth amidst policy uncertainties around tariffs and interest rates. Penny stocks, though often seen as relics of past market eras, continue to offer intriguing opportunities for those looking beyond established names. These smaller or newer companies can present affordable entry points with significant growth potential when backed by strong financials and solid fundamentals.

Top 10 Penny Stocks In Canada

| Name | Share Price | Market Cap | Financial Health Rating |

| Mandalay Resources (TSX:MND) | CA$4.09 | CA$370.94M | ★★★★★★ |

| Pulse Seismic (TSX:PSD) | CA$2.42 | CA$125.06M | ★★★★★★ |

| Silvercorp Metals (TSX:SVM) | CA$4.40 | CA$970.33M | ★★★★★★ |

| Findev (TSXV:FDI) | CA$0.50 | CA$14.32M | ★★★★★★ |

| PetroTal (TSX:TAL) | CA$0.66 | CA$583.7M | ★★★★★★ |

| Foraco International (TSX:FAR) | CA$2.40 | CA$236.24M | ★★★★★☆ |

| NamSys (TSXV:CTZ) | CA$1.14 | CA$31.7M | ★★★★★★ |

| East West Petroleum (TSXV:EW) | CA$0.045 | CA$4.07M | ★★★★★★ |

| Hemisphere Energy (TSXV:HME) | CA$1.83 | CA$179.46M | ★★★★★☆ |

| Tornado Infrastructure Equipment (TSXV:TGH) | CA$0.97 | CA$140.31M | ★★★★★☆ |

Click here to see the full list of 944 stocks from our TSX Penny Stocks screener.

Let's explore several standout options from the results in the screener.

Payfare (TSX:PAY)

Simply Wall St Financial Health Rating: ★★★★★★

Overview: Payfare Inc. is a financial technology company offering instant payout and digital banking solutions for gig economy workers across Canada, the United States, and Mexico, with a market cap of CA$186.87 million.

Operations: The company generates CA$216.87 million in revenue from its data processing segment.

Market Cap: CA$186.87M

Payfare Inc., with a market cap of CA$186.87 million, has shown robust financial performance, generating CA$216.87 million in revenue from its data processing segment. The company is debt-free and boasts high-quality earnings, with profits growing by 74.3% over the past year and exceeding industry averages. Despite increased volatility in share price recently, Payfare's price-to-earnings ratio of 9.7x suggests it may be undervalued compared to the broader Canadian market average of 14.5x. Recent developments include an acquisition agreement valued at approximately CA$200 million and the launch of Pronto by PayfareTM, enhancing financial flexibility for gig economy workers.

- Click to explore a detailed breakdown of our findings in Payfare's financial health report.

- Learn about Payfare's future growth trajectory here.

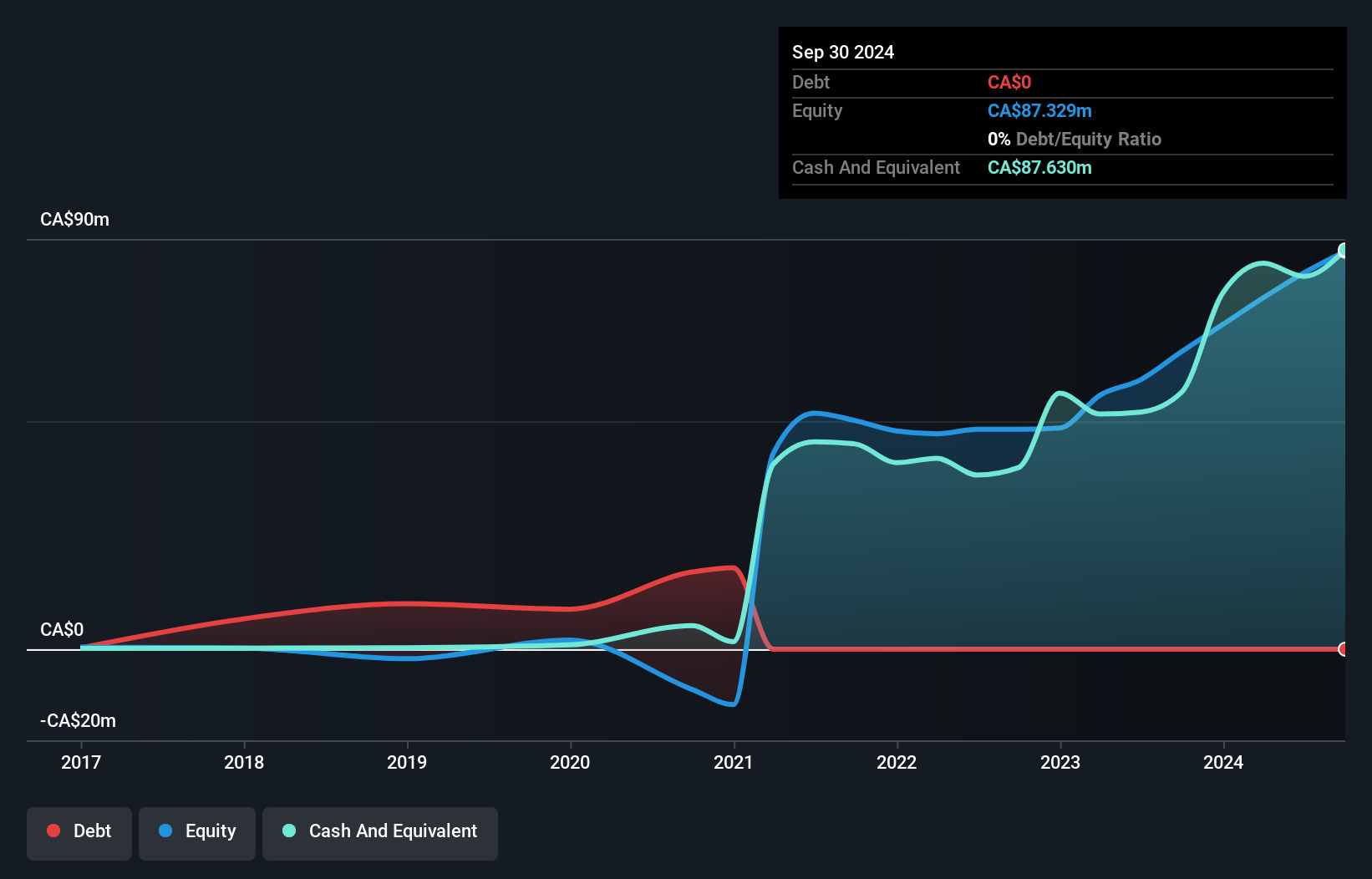

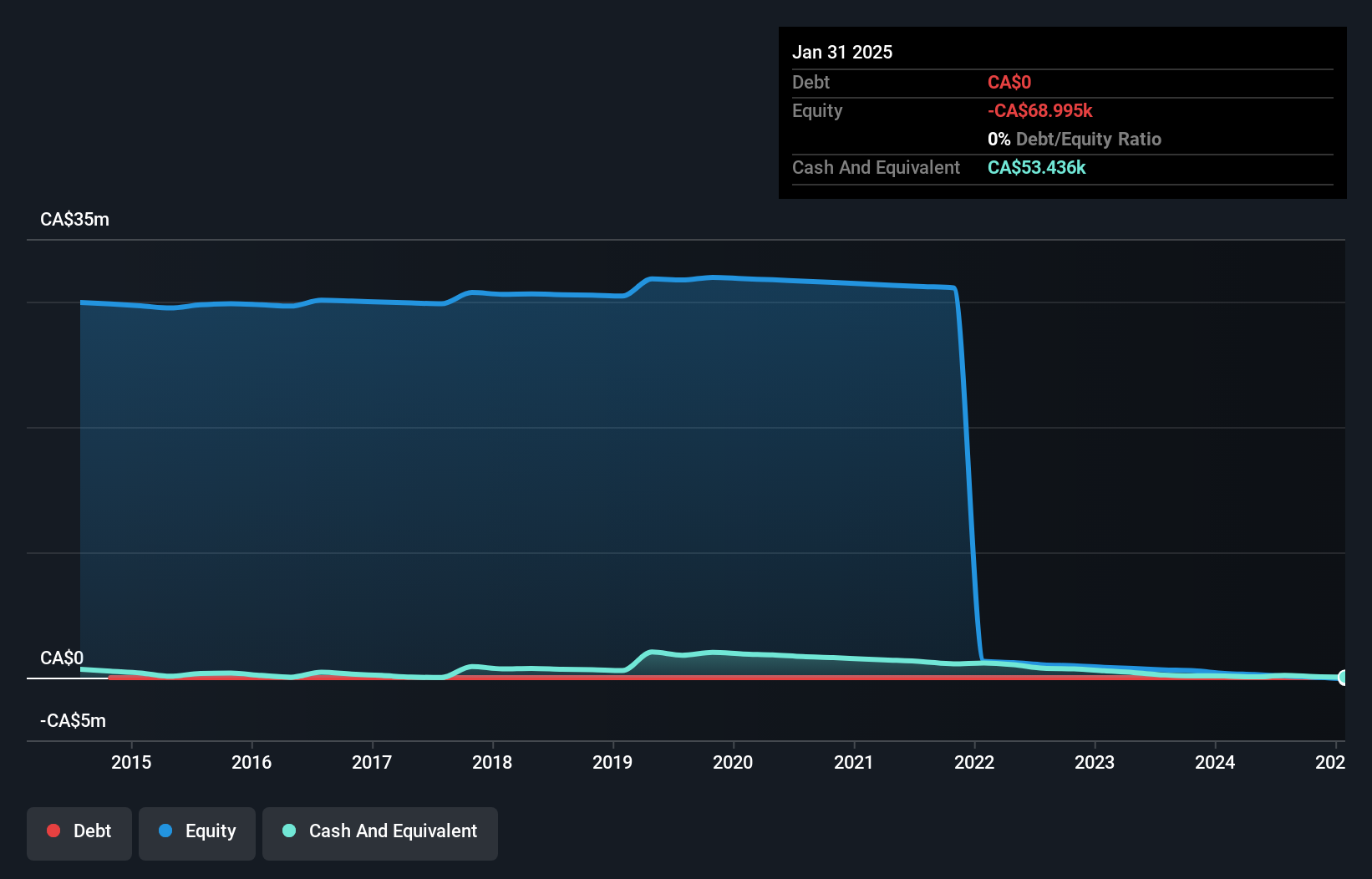

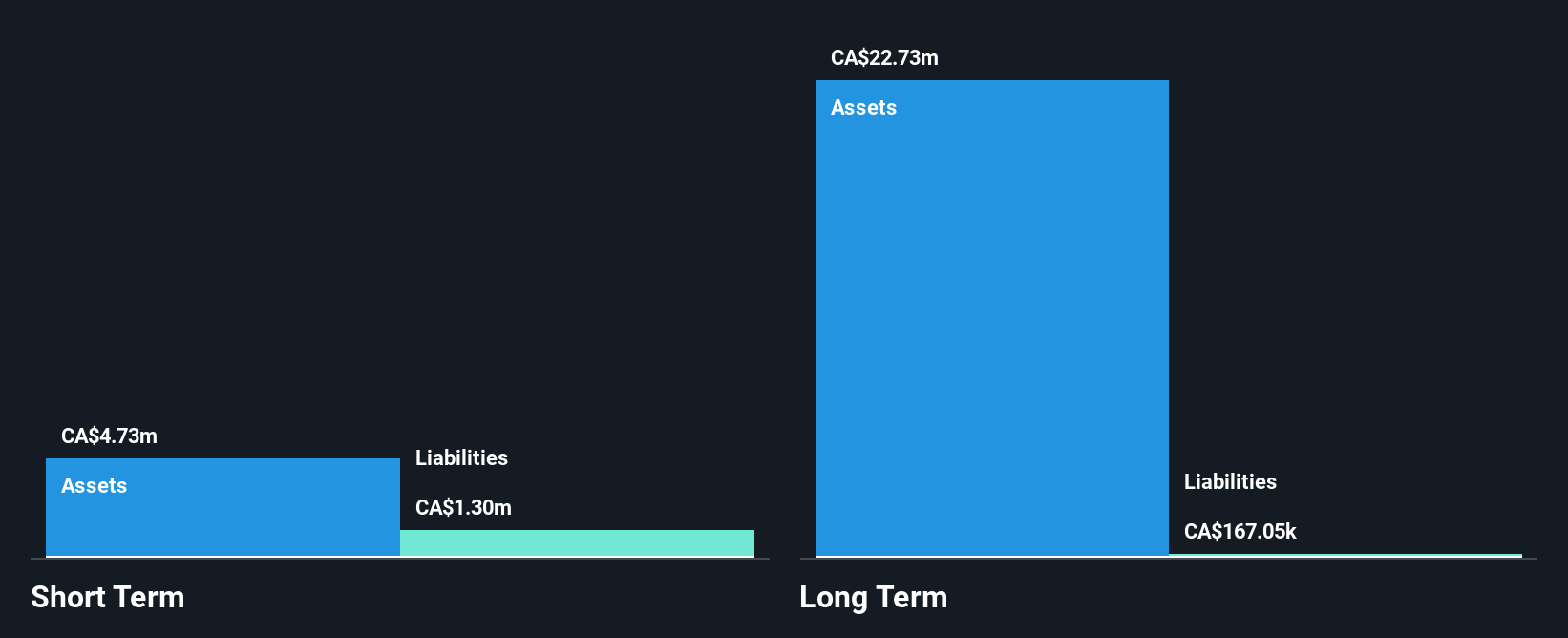

Pacific Booker Minerals (TSXV:BKM)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Pacific Booker Minerals Inc. is involved in the exploration of mineral properties in Canada and has a market capitalization of CA$12.11 million.

Operations: The company has not reported any revenue segments.

Market Cap: CA$12.11M

Pacific Booker Minerals Inc., with a market cap of CA$12.11 million, is pre-revenue and currently unprofitable, reporting increased net losses for the recent quarter. The company has no debt, which can be advantageous in maintaining financial flexibility. However, its short-term assets are insufficient to cover short-term liabilities of CA$690.6K, indicating potential liquidity challenges. Despite a seasoned board averaging 19.6 years in tenure and no significant shareholder dilution recently, the stock exhibits high volatility and lacks meaningful revenue streams to support growth prospects within the metals and mining industry framework.

- Navigate through the intricacies of Pacific Booker Minerals with our comprehensive balance sheet health report here.

- Evaluate Pacific Booker Minerals' historical performance by accessing our past performance report.

Doubleview Gold (TSXV:DBG)

Simply Wall St Financial Health Rating: ★★★★★☆

Overview: Doubleview Gold Corp. is a company focused on the acquisition, exploration, and development of mineral resource properties in Canada, with a market cap of CA$71.45 million.

Operations: Doubleview Gold Corp. currently does not report any revenue segments.

Market Cap: CA$71.45M

Doubleview Gold Corp., with a market cap of CA$71.45 million, is pre-revenue and currently unprofitable, facing increased losses over the past five years. The company has no debt, which provides financial flexibility but has diluted shareholders recently to raise capital. Doubleview's short-term assets do not cover its short-term liabilities of CA$811.3K, suggesting liquidity issues despite recent private placements raising CA$1.6 million in December 2024. Its seasoned management and board bring experience to the table as they advance exploration at the Hat Project in British Columbia, potentially enhancing resource estimates and future prospects through ongoing drilling campaigns.

- Unlock comprehensive insights into our analysis of Doubleview Gold stock in this financial health report.

- Gain insights into Doubleview Gold's past trends and performance with our report on the company's historical track record.

Next Steps

- Discover the full array of 944 TSX Penny Stocks right here.

- Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Jump on the AI train with fast growing tech companies forging a new era of innovation.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSXV:BKM

Pacific Booker Minerals

Engages in the exploration of mineral properties in Canada.

Mediocre balance sheet with low risk.

Market Insights

Weekly Picks

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

The Quiet Giant That Became AI’s Power Grid

Recently Updated Narratives

A case for USD $14.81 per share based on book value. Be warned, this is a micro-cap dependent on a single mine.

Occidental Petroleum to Become Fairly Priced at $68.29 According to Future Projections

Agfa-Gevaert is a digital and materials turnaround opportunity, with growth potential in ZIRFON, but carrying legacy risks.

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)