- Canada

- /

- Metals and Mining

- /

- TSX:IVN

3 TSX Stocks Trading At Estimated Discounts Of Up To 40.6%

Reviewed by Simply Wall St

The Canadian TSX has experienced a modest decline of about 3% amid recent economic uncertainties, including softening labor markets and potential interest rate cuts by central banks. In such an environment, identifying undervalued stocks can offer investors opportunities to acquire quality investments at potentially discounted prices.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Computer Modelling Group (TSX:CMG) | CA$11.83 | CA$22.18 | 46.7% |

| Calian Group (TSX:CGY) | CA$44.49 | CA$72.78 | 38.9% |

| Kinaxis (TSX:KXS) | CA$151.07 | CA$283.39 | 46.7% |

| Viemed Healthcare (TSX:VMD) | CA$10.45 | CA$20.08 | 48% |

| Bragg Gaming Group (TSX:BRAG) | CA$6.63 | CA$10.65 | 37.8% |

| Endeavour Mining (TSX:EDV) | CA$30.63 | CA$51.53 | 40.6% |

| NanoXplore (TSX:GRA) | CA$2.30 | CA$4.56 | 49.6% |

| Blackline Safety (TSX:BLN) | CA$5.28 | CA$10.20 | 48.3% |

| Opsens (TSX:OPS) | CA$2.90 | CA$4.64 | 37.5% |

| Boyd Group Services (TSX:BYD) | CA$218.63 | CA$342.08 | 36.1% |

We're going to check out a few of the best picks from our screener tool.

Constellation Software (TSX:CSU)

Overview: Constellation Software Inc., with a market cap of CA$90.38 billion, acquires, builds, and manages vertical market software businesses in Canada, the United States, Europe, and internationally.

Operations: Revenue from the Software & Programming segment amounted to $9.27 billion.

Estimated Discount To Fair Value: 23.1%

Constellation Software's recent earnings report highlights robust financial performance, with second-quarter revenue at US$2.47 billion and net income of US$177 million, reflecting strong cash flows. Despite a high level of debt, the company is trading 23.1% below its estimated fair value and is highly undervalued based on discounted cash flow analysis. The forecasted annual earnings growth rate of 23.6% significantly outpaces the Canadian market average, indicating potential for substantial long-term gains.

- Our growth report here indicates Constellation Software may be poised for an improving outlook.

- Dive into the specifics of Constellation Software here with our thorough financial health report.

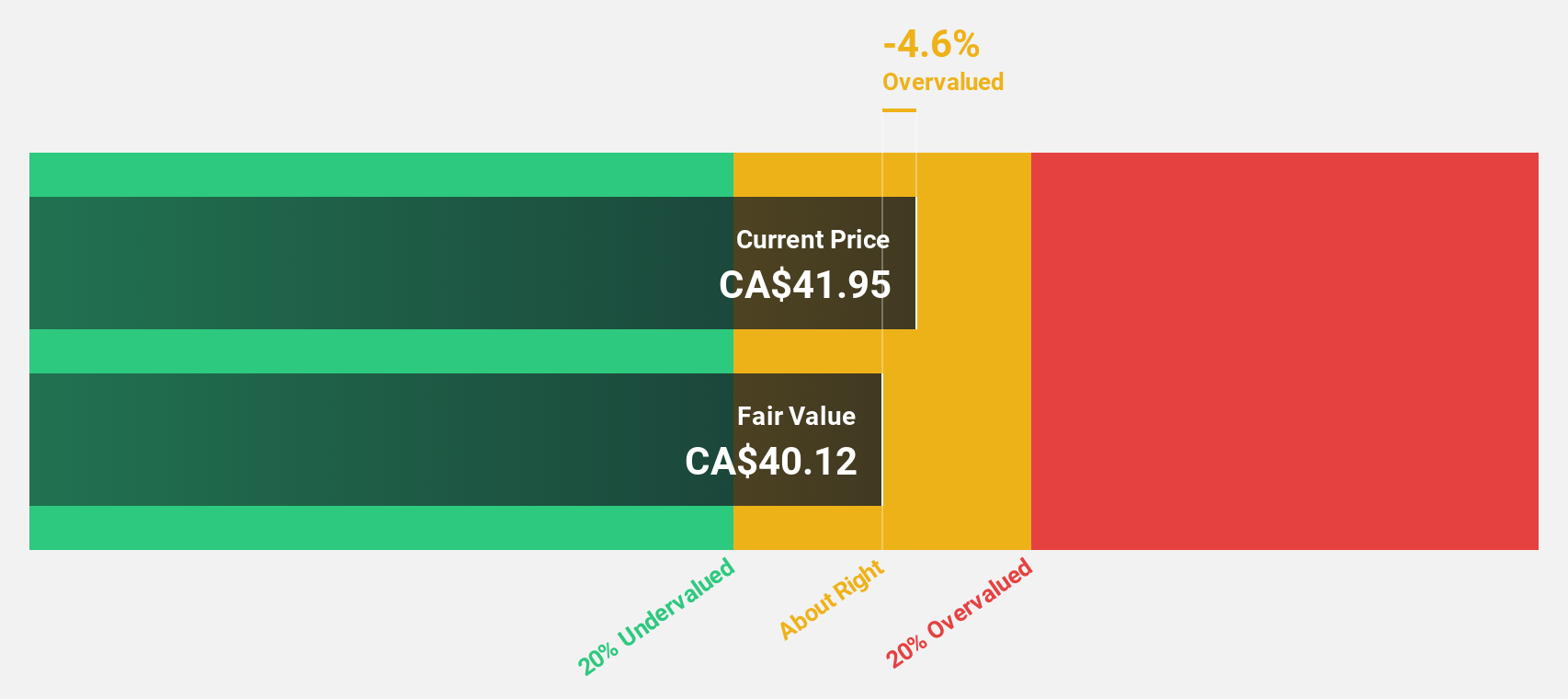

Endeavour Mining (TSX:EDV)

Overview: Endeavour Mining plc, with a market cap of CA$7.06 billion, operates as a gold mining company in West Africa through its subsidiaries.

Operations: Revenue segments (in millions of $): Houndé Mine: 612.70, Sabodala Massawa Mine: 509.60, Mana Mine Burkina Faso: 308.40, Ity Mine Côte D’Ivoire: 708.10 Endeavour Mining generates revenue from its operations in West Africa primarily through the Houndé Mine ($612.70M), Sabodala Massawa Mine ($509.60M), Mana Mine Burkina Faso ($308.40M), and Ity Mine Côte D’Ivoire ($708.10M).

Estimated Discount To Fair Value: 40.6%

Endeavour Mining is trading at CA$30.63, significantly below its estimated fair value of CA$51.53, suggesting it may be undervalued based on cash flows. Despite a dividend yield of 3.63% that isn't well covered by earnings or free cash flows, the company's revenue is forecast to grow 11.3% annually, outpacing the Canadian market's 6.8%. Recent settlements and strategic divestments have also bolstered its financial position with an expected $60 million in cash payments and future royalties from gold sales.

- Upon reviewing our latest growth report, Endeavour Mining's projected financial performance appears quite optimistic.

- Click here and access our complete balance sheet health report to understand the dynamics of Endeavour Mining.

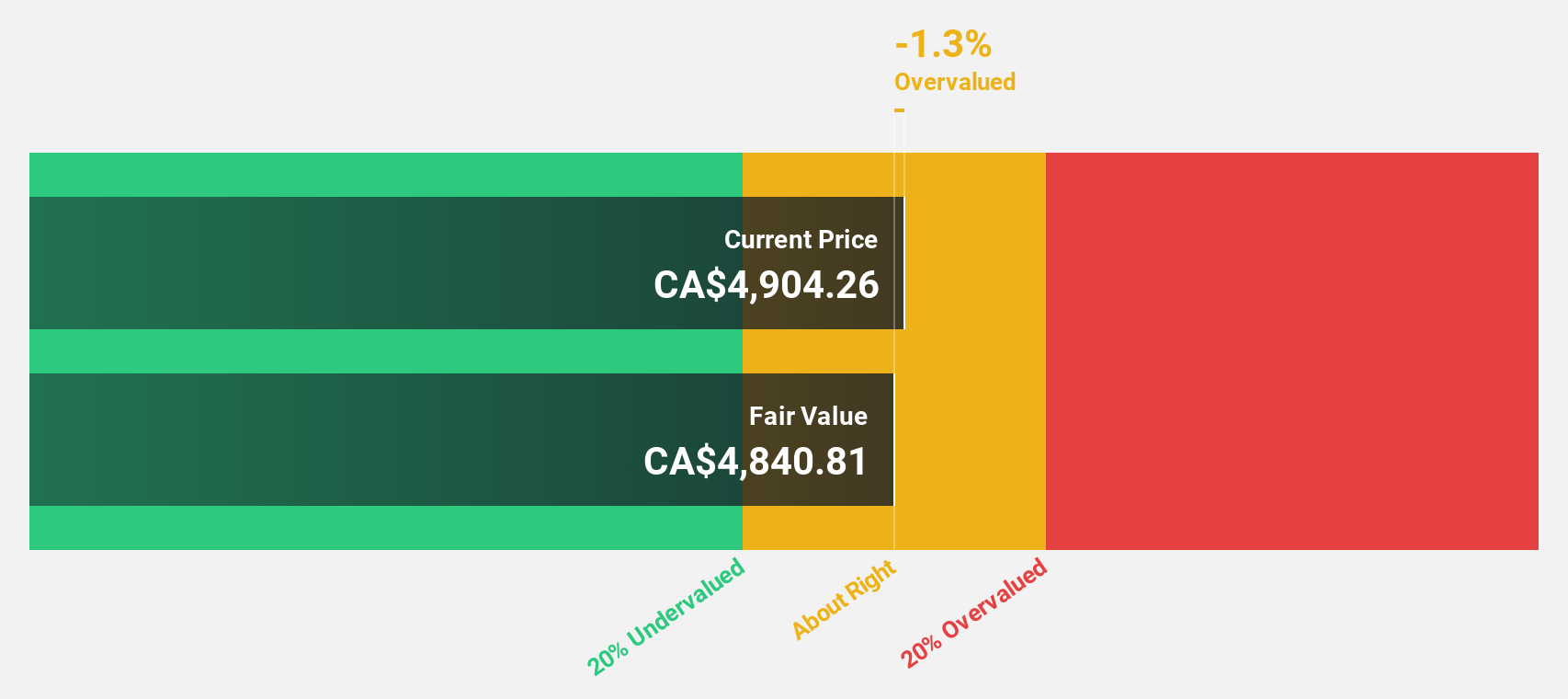

Ivanhoe Mines (TSX:IVN)

Overview: Ivanhoe Mines Ltd. focuses on the mining, development, and exploration of minerals and precious metals primarily in Africa, with a market cap of CA$21.71 billion.

Operations: The company's revenue segments include mining, development, and exploration of minerals and precious metals primarily in Africa.

Estimated Discount To Fair Value: 27.9%

Ivanhoe Mines is trading at CA$17.39, well below its estimated fair value of CA$24.13, indicating potential undervaluation based on cash flows. Recent achievements include a record monthly production of 40,347 tonnes of copper at the Kamoa-Kakula Copper Complex and a significant MOU with Zambia's Ministry of Mines to explore new projects. Despite past shareholder dilution and low revenue, earnings are forecast to grow significantly at 71.6% per year, with analysts expecting further stock price appreciation by 36.1%.

- Our expertly prepared growth report on Ivanhoe Mines implies its future financial outlook may be stronger than recent results.

- Take a closer look at Ivanhoe Mines' balance sheet health here in our report.

Turning Ideas Into Actions

- Embark on your investment journey to our 27 Undervalued TSX Stocks Based On Cash Flows selection here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:IVN

Ivanhoe Mines

Engages in the mining, development, and exploration of minerals and precious metals primarily in Africa.

High growth potential and fair value.