- Canada

- /

- Metals and Mining

- /

- TSX:GSV

Companies Like Gold Standard Ventures (TSE:GSV) Are In A Position To Invest In Growth

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. For example, although Amazon.com made losses for many years after listing, if you had bought and held the shares since 1999, you would have made a fortune. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

Given this risk, we thought we'd take a look at whether Gold Standard Ventures (TSE:GSV) shareholders should be worried about its cash burn. In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

See our latest analysis for Gold Standard Ventures

Does Gold Standard Ventures Have A Long Cash Runway?

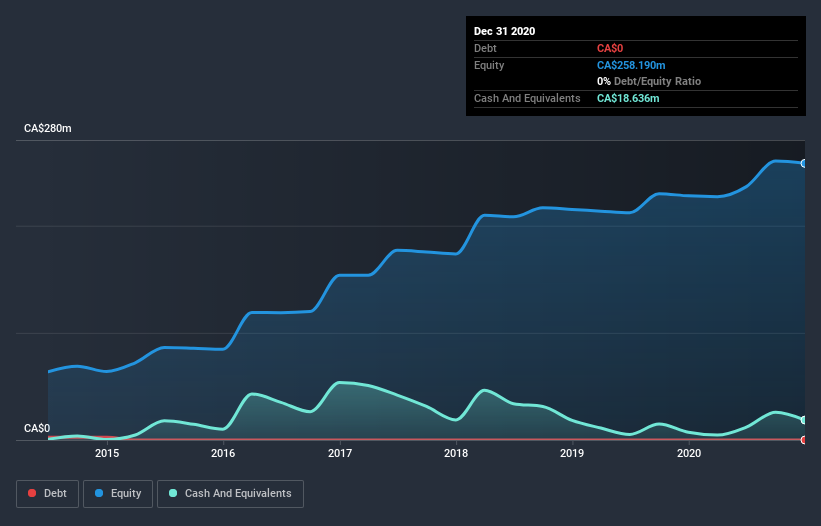

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. In December 2020, Gold Standard Ventures had CA$19m in cash, and was debt-free. In the last year, its cash burn was CA$28m. Therefore, from December 2020 it had roughly 8 months of cash runway. Importantly, the one analyst we see covering the stock thinks that Gold Standard Ventures will reach cashflow breakeven in around 14 months. That means unless the company reduces its cash burn quickly, it may well look to raise more cash. The image below shows how its cash balance has been changing over the last few years.

How Is Gold Standard Ventures' Cash Burn Changing Over Time?

Because Gold Standard Ventures isn't currently generating revenue, we consider it an early-stage business. So while we can't look to sales to understand growth, we can look at how the cash burn is changing to understand how expenditure is trending over time. It's possible that the 7.1% reduction in cash burn over the last year is evidence of management tightening their belts as cash reserves deplete. While the past is always worth studying, it is the future that matters most of all. So you might want to take a peek at how much the company is expected to grow in the next few years.

How Hard Would It Be For Gold Standard Ventures To Raise More Cash For Growth?

While Gold Standard Ventures is showing a solid reduction in its cash burn, it's still worth considering how easily it could raise more cash, even just to fuel faster growth. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. Many companies end up issuing new shares to fund future growth. By looking at a company's cash burn relative to its market capitalisation, we gain insight on how much shareholders would be diluted if the company needed to raise enough cash to cover another year's cash burn.

Gold Standard Ventures' cash burn of CA$28m is about 11% of its CA$268m market capitalisation. As a result, we'd venture that the company could raise more cash for growth without much trouble, albeit at the cost of some dilution.

How Risky Is Gold Standard Ventures' Cash Burn Situation?

On this analysis of Gold Standard Ventures' cash burn, we think its cash burn relative to its market cap was reassuring, while its cash runway has us a bit worried. It's clearly very positive to see that at least one analyst is forecasting the company will break even fairly soon. While we're the kind of investors who are always a bit concerned about the risks involved with cash burning companies, the metrics we have discussed in this article leave us relatively comfortable about Gold Standard Ventures' situation. Separately, we looked at different risks affecting the company and spotted 4 warning signs for Gold Standard Ventures (of which 2 don't sit too well with us!) you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

If you decide to trade Gold Standard Ventures, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:GSV

Gold Standard Ventures

Gold Standard Ventures Corp., an exploration stage company, engages in the development of district-scale and other gold-bearing mineral resource properties in Nevada, the United States.

Adequate balance sheet and slightly overvalued.

Market Insights

Community Narratives