Advertisement

- Canada

- /

- Metals and Mining

- /

- TSX:DPM

Shareholders Will Probably Not Have Any Issues With Dundee Precious Metals Inc.'s (TSE:DPM) CEO Compensation

Key Insights

- Dundee Precious Metals will host its Annual General Meeting on 8th of May

- CEO David Rae's total compensation includes salary of US$588.7k

- Total compensation is similar to the industry average

- Dundee Precious Metals' EPS declined by 3.2% over the past three years while total shareholder return over the past three years was 23%

Under the guidance of CEO David Rae, Dundee Precious Metals Inc. (TSE:DPM) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 8th of May. Here is our take on why we think the CEO compensation looks appropriate.

See our latest analysis for Dundee Precious Metals

How Does Total Compensation For David Rae Compare With Other Companies In The Industry?

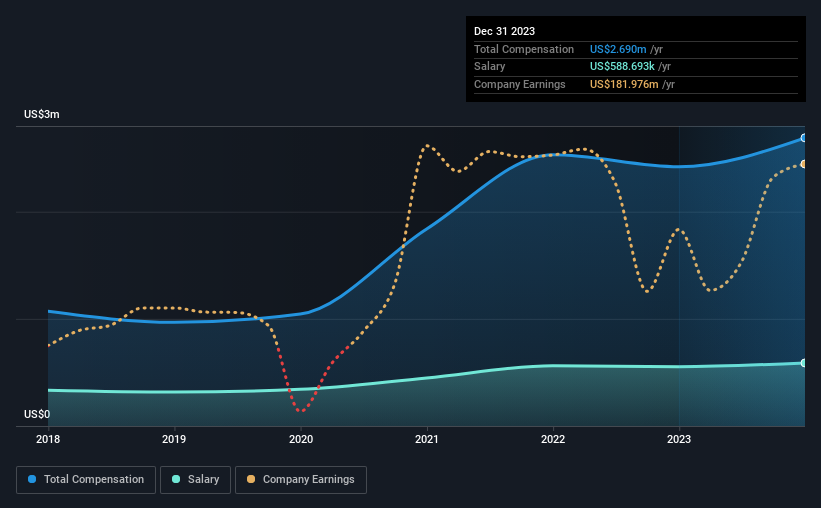

According to our data, Dundee Precious Metals Inc. has a market capitalization of CA$1.9b, and paid its CEO total annual compensation worth US$2.7m over the year to December 2023. That's a notable increase of 11% on last year. While this analysis focuses on total compensation, it's worth acknowledging that the salary portion is lower, valued at US$589k.

For comparison, other companies in the Canadian Metals and Mining industry with market capitalizations ranging between CA$1.4b and CA$4.4b had a median total CEO compensation of US$2.6m. So it looks like Dundee Precious Metals compensates David Rae in line with the median for the industry. Moreover, David Rae also holds CA$1.2m worth of Dundee Precious Metals stock directly under their own name.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$589k | US$554k | 22% |

| Other | US$2.1m | US$1.9m | 78% |

| Total Compensation | US$2.7m | US$2.4m | 100% |

On an industry level, around 94% of total compensation represents salary and 6% is other remuneration. It's interesting to note that Dundee Precious Metals allocates a smaller portion of compensation to salary in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

Dundee Precious Metals Inc.'s Growth

Over the last three years, Dundee Precious Metals Inc. has shrunk its earnings per share by 3.2% per year. It achieved revenue growth of 20% over the last year.

The decrease in EPS could be a concern for some investors. On the other hand, the strong revenue growth suggests the business is growing. These two metrics are moving in different directions, so while it's hard to be confident judging performance, we think the stock is worth watching. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has Dundee Precious Metals Inc. Been A Good Investment?

Dundee Precious Metals Inc. has generated a total shareholder return of 23% over three years, so most shareholders would be reasonably content. But they would probably prefer not to see CEO compensation far in excess of the median.

In Summary...

Some shareholders will be pleased by the relatively good results, however, the results could still be improved. Still, we think that until shareholders see an improvement in EPS growth, they may find it hard to justify a pay rise for the CEO.

CEO compensation is a crucial aspect to keep your eyes on but investors also need to keep their eyes open for other issues related to business performance. That's why we did some digging and identified 1 warning sign for Dundee Precious Metals that you should be aware of before investing.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:DPM

Dundee Precious Metals

A gold mining company, engages in the acquisition, exploration, development, mining, and processing of precious metals.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value US$282.83|32.8% undervalued

BL

Community Contributor

Planet Labs: At The Heart Of The Emerging New Space Boom

Fair Value US$11.31|45.4% undervalued

AN

Community Contributor

Exxon in Guyana 5 year forecast Low $135 to High $189

Fair Value US$174.00|37.0% undervalued

AG

Community Contributor