Advertisement

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. We note that Avino Silver & Gold Mines Ltd. (TSE:ASM) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Avino Silver & Gold Mines

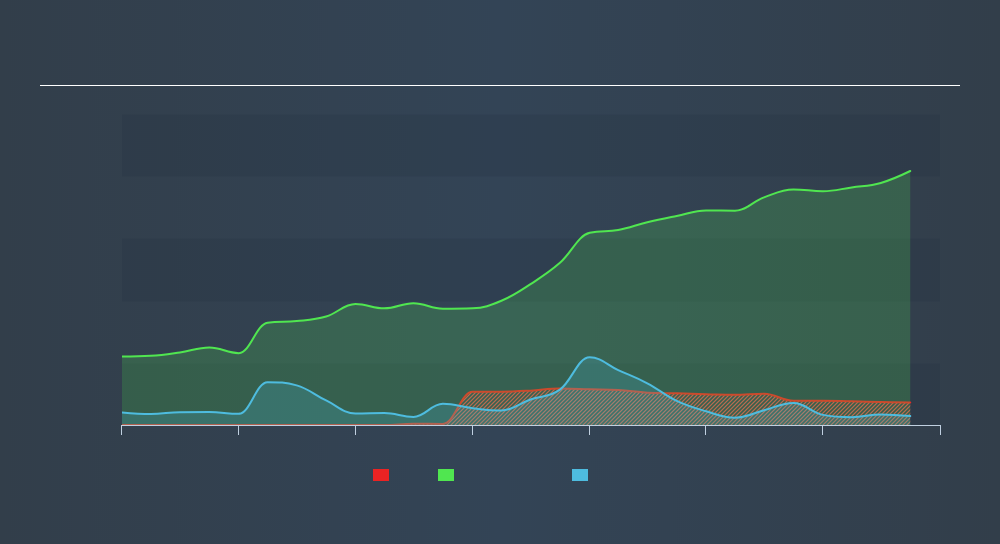

What Is Avino Silver & Gold Mines's Net Debt?

The image below, which you can click on for greater detail, shows that Avino Silver & Gold Mines had debt of US$7.26m at the end of September 2019, a reduction from US$10.0m over a year. However, because it has a cash reserve of US$2.88m, its net debt is less, at about US$4.38m.

How Healthy Is Avino Silver & Gold Mines's Balance Sheet?

We can see from the most recent balance sheet that Avino Silver & Gold Mines had liabilities of US$10.5m falling due within a year, and liabilities of US$21.0m due beyond that. On the other hand, it had cash of US$2.88m and US$9.02m worth of receivables due within a year. So it has liabilities totalling US$19.6m more than its cash and near-term receivables, combined.

This deficit isn't so bad because Avino Silver & Gold Mines is worth US$38.0m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Avino Silver & Gold Mines can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

In the last year Avino Silver & Gold Mines had negative earnings before interest and tax, and actually shrunk its revenue by 15%, to US$30m. That's not what we would hope to see.

Caveat Emptor

Not only did Avino Silver & Gold Mines's revenue slip over the last twelve months, but it also produced negative earnings before interest and tax (EBIT). To be specific the EBIT loss came in at US$2.3m. When we look at that and recall the liabilities on its balance sheet, relative to cash, it seems unwise to us for the company to have any debt. So we think its balance sheet is a little strained, though not beyond repair. Another cause for caution is that is bled US$10.0m in negative free cash flow over the last twelve months. So suffice it to say we consider the stock very risky. For riskier companies like Avino Silver & Gold Mines I always like to keep an eye on whether insiders are buying or selling. So click here if you want to find out for yourself.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

About TSX:ASM

Avino Silver & Gold Mines

Engages in the acquisition, exploration, and advancement of mineral properties in Mexico.

Flawless balance sheet with solid track record.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.4% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|17.8% undervalued

TI

Community Contributor