Advertisement

- Canada

- /

- Metals and Mining

- /

- TSX:ARIS

Discovering Canada's Undiscovered Gems In August 2024

Simply Wall St

Reviewed by Simply Wall St

The Canadian market has experienced significant volatility in 2024, with sharp swings in key indices like the S&P/TSX Composite Index reflecting broader economic uncertainties. Despite these fluctuations, discerning investors can still find promising opportunities among small-cap stocks that demonstrate resilience and potential for growth. In this context, identifying undiscovered gems involves looking for companies with strong fundamentals, innovative business models, and the ability to navigate market turbulence effectively.

Top 10 Undiscovered Gems With Strong Fundamentals In Canada

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| TWC Enterprises | 6.74% | 10.99% | 25.68% | ★★★★★★ |

| Jaguar Mining | 1.19% | 5.49% | 5.12% | ★★★★★★ |

| Taiga Building Products | NA | 6.05% | 10.50% | ★★★★★★ |

| Amerigo Resources | 12.87% | 7.49% | 12.97% | ★★★★★☆ |

| Reconnaissance Energy Africa | NA | 31.73% | -6.92% | ★★★★★☆ |

| Firan Technology Group | 17.91% | 3.75% | 23.32% | ★★★★★☆ |

| Mako Mining | 22.90% | 38.12% | 54.79% | ★★★★★☆ |

| Pizza Pizza Royalty | 15.66% | 3.64% | 3.95% | ★★★★☆☆ |

| Queen's Road Capital Investment | 7.20% | 22.14% | 22.20% | ★★★★☆☆ |

| Genesis Land Development | 53.32% | 25.58% | 47.05% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

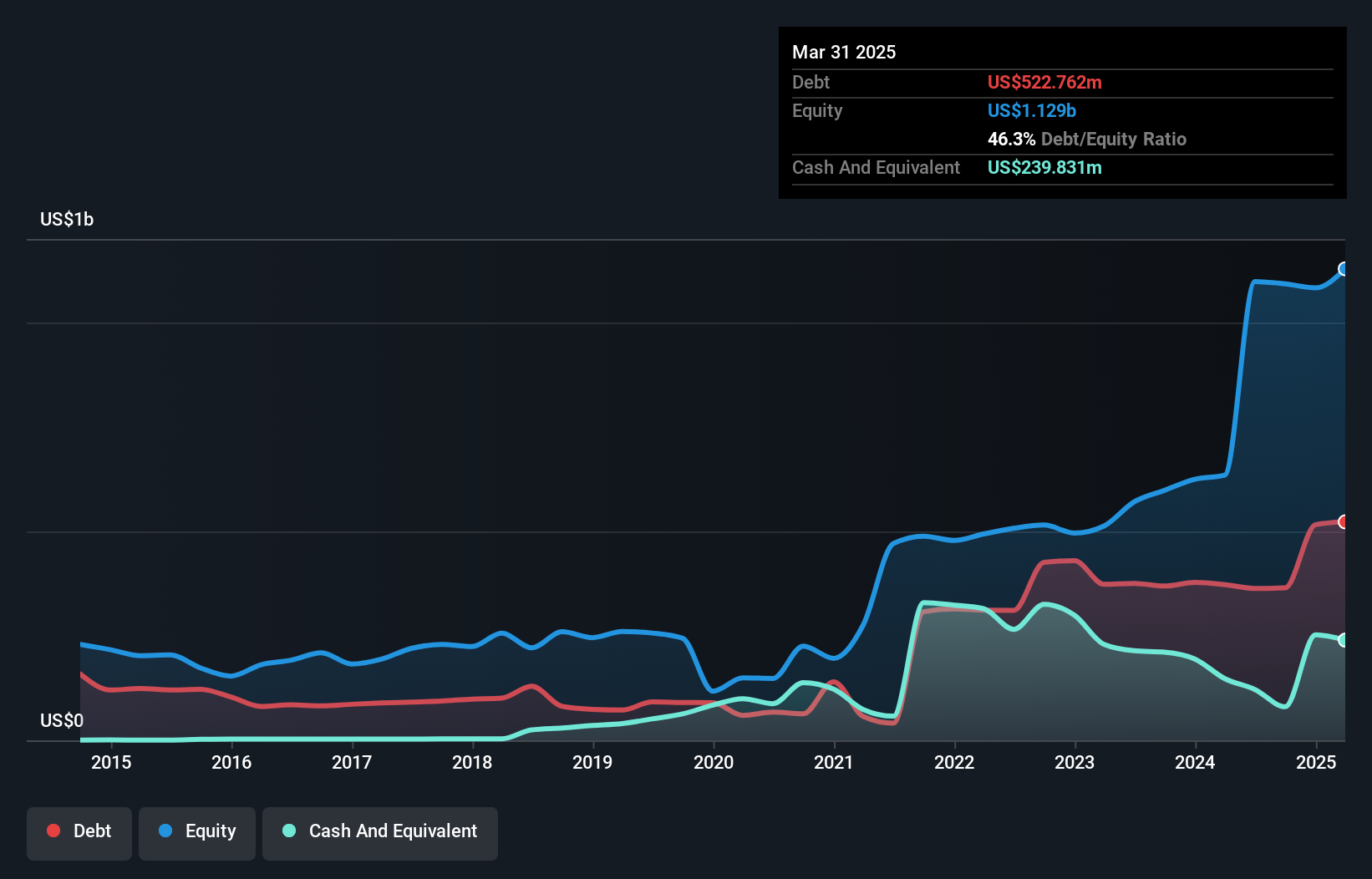

Aris Mining (TSX:ARIS)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Aris Mining Corporation, with a market cap of CA$949.44 million, engages in the acquisition, exploration, development, and operation of gold properties in Canada, Colombia, and Guyana.

Operations: Aris Mining generates revenue primarily from its Segovia Operations ($409.96 million) and the Marmato Project ($48.43 million).

Aris Mining, a Canadian mining company, has shown significant progress recently. The company became profitable this year and is trading at 96.5% below our estimate of its fair value. Its debt to equity ratio increased from 27.8% to 58.7% over the past five years but remains satisfactory with a net debt to equity ratio of 35.5%. Aris's interest payments are well covered by EBIT at 6.7x coverage, indicating strong financial health despite recent shareholder dilution.

- Delve into the full analysis health report here for a deeper understanding of Aris Mining.

Examine Aris Mining's past performance report to understand how it has performed in the past.

Extendicare (TSX:EXE)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Extendicare Inc., with a market cap of CA$636.02 million, operates through its subsidiaries to provide care and services for seniors in Canada.

Operations: Extendicare generates revenue primarily from long-term care services and home healthcare operations. The company reported CA$1.15 billion in total revenue, with a net profit margin of 3.2%.

Extendicare's earnings growth of 3957% over the past year far outpaced the healthcare industry's 5.8%, showcasing its robust performance. Net income for Q2 2024 was CAD 25.89 million, a significant jump from CAD 1.95 million last year, with sales reaching CAD 348.48 million compared to CAD 307.54 million previously reported. The company repurchased up to approximately 7.16 million shares under its buyback program, indicating confidence in its valuation and future prospects despite a high net debt to equity ratio of about 178%.

Lassonde Industries (TSX:LAS.A)

Simply Wall St Value Rating: ★★★★★★

Overview: Lassonde Industries Inc. develops, manufactures, and markets a variety of ready-to-drink beverages, fruit-based snacks, and frozen juice concentrates in Canada, the United States, and internationally with a market cap of CA$1.14 billion.

Operations: Lassonde Industries generates revenue primarily from ready-to-drink beverages, fruit-based snacks, and frozen juice concentrates in Canada, the United States, and internationally. The company has a market cap of CA$1.14 billion.

Lassonde Industries has seen its debt to equity ratio drop from 50.2% to 15.5% over the last five years, reflecting a stronger financial position. The company reported earnings growth of 53.4%, outpacing the Food industry’s 34.8%. Trading at 71.8% below its estimated fair value, Lassonde offers significant upside potential. Recent expansions include a $53 million investment in a North Carolina facility, enhancing production and distribution capabilities while adding new jobs and promoting sustainability initiatives.

- Unlock comprehensive insights into our analysis of Lassonde Industries stock in this health report.

Explore historical data to track Lassonde Industries' performance over time in our Past section.

Next Steps

- Unlock our comprehensive list of 43 TSX Undiscovered Gems With Strong Fundamentals by clicking here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:ARIS

Aris Mining

Engages in the acquisition, exploration, development, and operation of gold properties in Canada, Colombia, and Guyana.

Solid track record and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor