Advertisement

Undervalued Small Caps With Insider Activity In Global For June 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a complex landscape marked by steady interest rates and mixed economic signals, small-cap stocks have emerged as resilient performers amid the broader market's fluctuations. With the Federal Reserve maintaining its rate stance and geopolitical tensions influencing investor sentiment, identifying promising small-cap opportunities with active insider participation can be crucial for investors seeking to capitalize on potential growth in this dynamic environment.

Top 10 Undervalued Small Caps With Insider Buying Globally

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Lion Rock Group | 5.0x | 0.4x | 49.97% | ★★★★☆☆ |

| Tristel | 29.0x | 4.1x | 9.93% | ★★★★☆☆ |

| A.G. BARR | 19.2x | 1.8x | 44.22% | ★★★★☆☆ |

| Hemisphere Energy | 5.2x | 2.2x | 8.76% | ★★★★☆☆ |

| Nexus Industrial REIT | 6.6x | 2.9x | 19.32% | ★★★★☆☆ |

| Sing Investments & Finance | 7.3x | 3.7x | 38.99% | ★★★★☆☆ |

| Absolent Air Care Group | 22.1x | 1.7x | 49.73% | ★★★☆☆☆ |

| Fuller Smith & Turner | 12.0x | 0.9x | -33.13% | ★★★☆☆☆ |

| Morguard North American Residential Real Estate Investment Trust | 5.6x | 1.8x | 9.86% | ★★★☆☆☆ |

| Seeing Machines | NA | 2.6x | 39.56% | ★★★☆☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

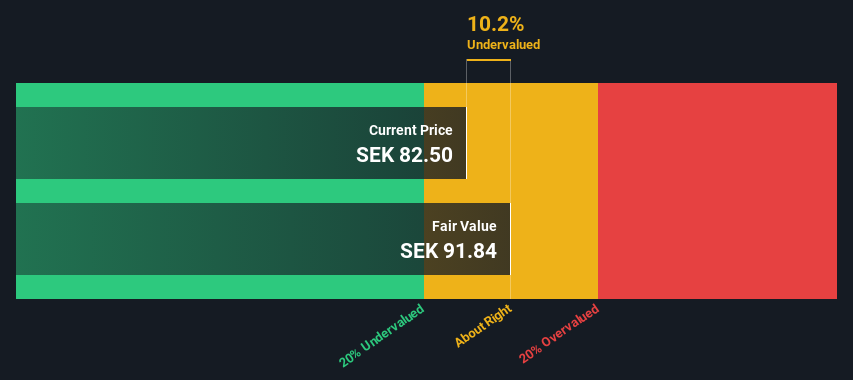

AcadeMedia (OM:ACAD)

Simply Wall St Value Rating: ★★★★☆☆

Overview: AcadeMedia operates as a leading educational services provider, offering adult education, compulsory and upper secondary schools, along with preschool and international programs, with a market cap of approximately SEK 4.35 billion.

Operations: AcadeMedia's primary revenue streams are derived from its Preschool & International segment (SEK 7.88 billion) and Upper Secondary Schools (SEK 6.54 billion), with Compulsory School also contributing significantly at SEK 4.70 billion. The company's gross profit margin has shown fluctuations, reaching a peak of 31.20% in recent periods, indicating varying efficiency in managing production costs relative to revenue generation over time.

PE: 10.8x

AcadeMedia, a smaller company in the education sector, recently reported third-quarter sales of SEK 5.04 billion, up from SEK 4.61 billion the previous year, with net income rising to SEK 241 million. Their strategic refinancing with DNB, Nordea, and SEB for SEK 1.66 billion until April 2028 enhances cash flow by SEK 116 million and supports international growth ambitions. Insider confidence is evident through recent share purchases in March and April this year. Earnings are projected to grow annually by over 15%.

- Dive into the specifics of AcadeMedia here with our thorough valuation report.

Review our historical performance report to gain insights into AcadeMedia's's past performance.

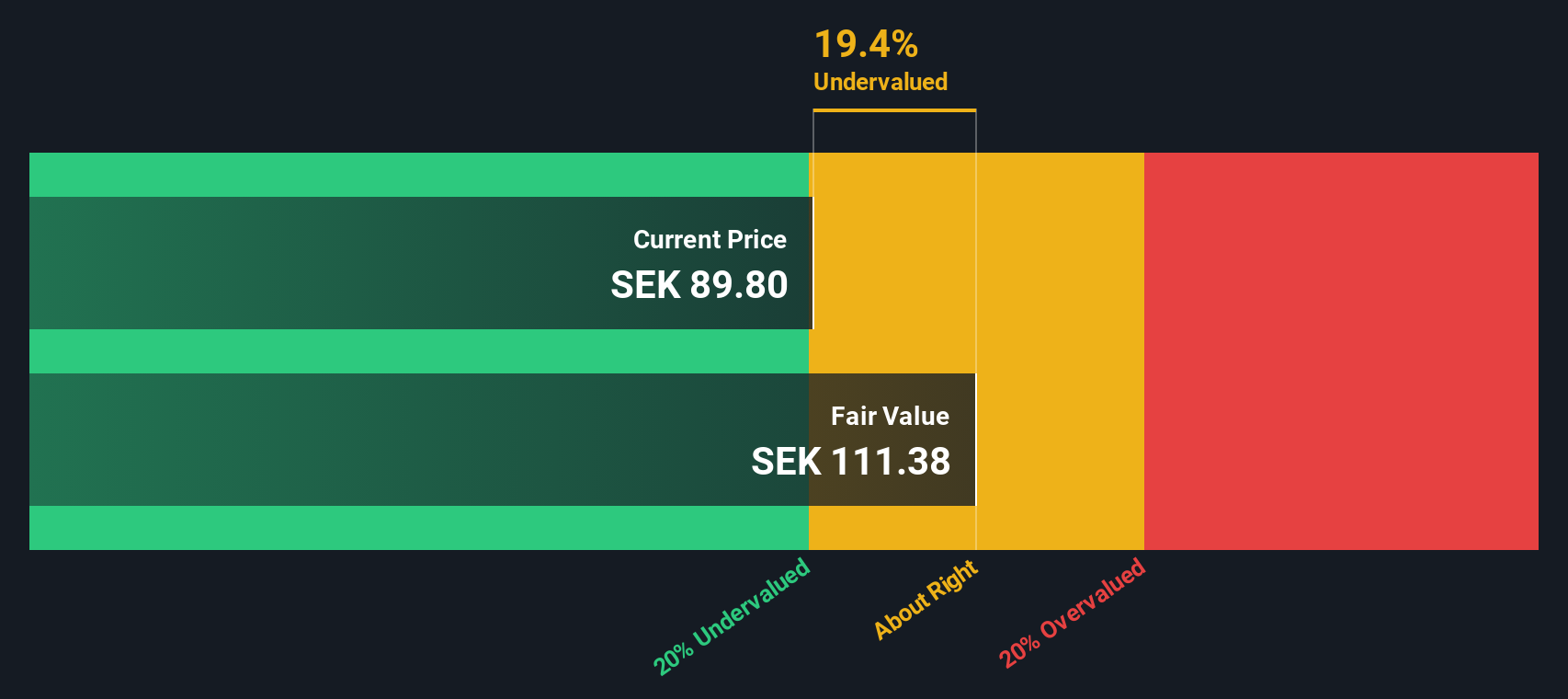

Hanza (OM:HANZA)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Hanza is a manufacturing solutions provider that offers comprehensive production services across main and other markets, with a market cap of approximately SEK 2.67 billion.

Operations: The company generates revenue primarily from Main Markets and Other Markets, with the Main Markets contributing a larger share. Over recent periods, the net income margin has shown variability, reaching 5.17% in December 2023 before declining to 2.38% by March 2025. Operating expenses are a significant part of the cost structure, with General & Administrative Expenses consistently being a major component.

PE: 33.1x

Hanza's recent financial performance shows growth, with Q1 2025 sales at SEK 1,326 million up from SEK 1,253 million the previous year. Net income increased to SEK 40 million from SEK 34 million. Despite lower profit margins at 2.4% compared to last year's 4.4%, insider confidence is evident as Francesco Franze purchased shares worth approximately SEK 6.8 million, increasing their stake by nearly 3.6%. This activity suggests potential optimism about future prospects despite current challenges in covering interest payments and reliance on external borrowing for funding.

- Get an in-depth perspective on Hanza's performance by reading our valuation report here.

Gain insights into Hanza's historical performance by reviewing our past performance report.

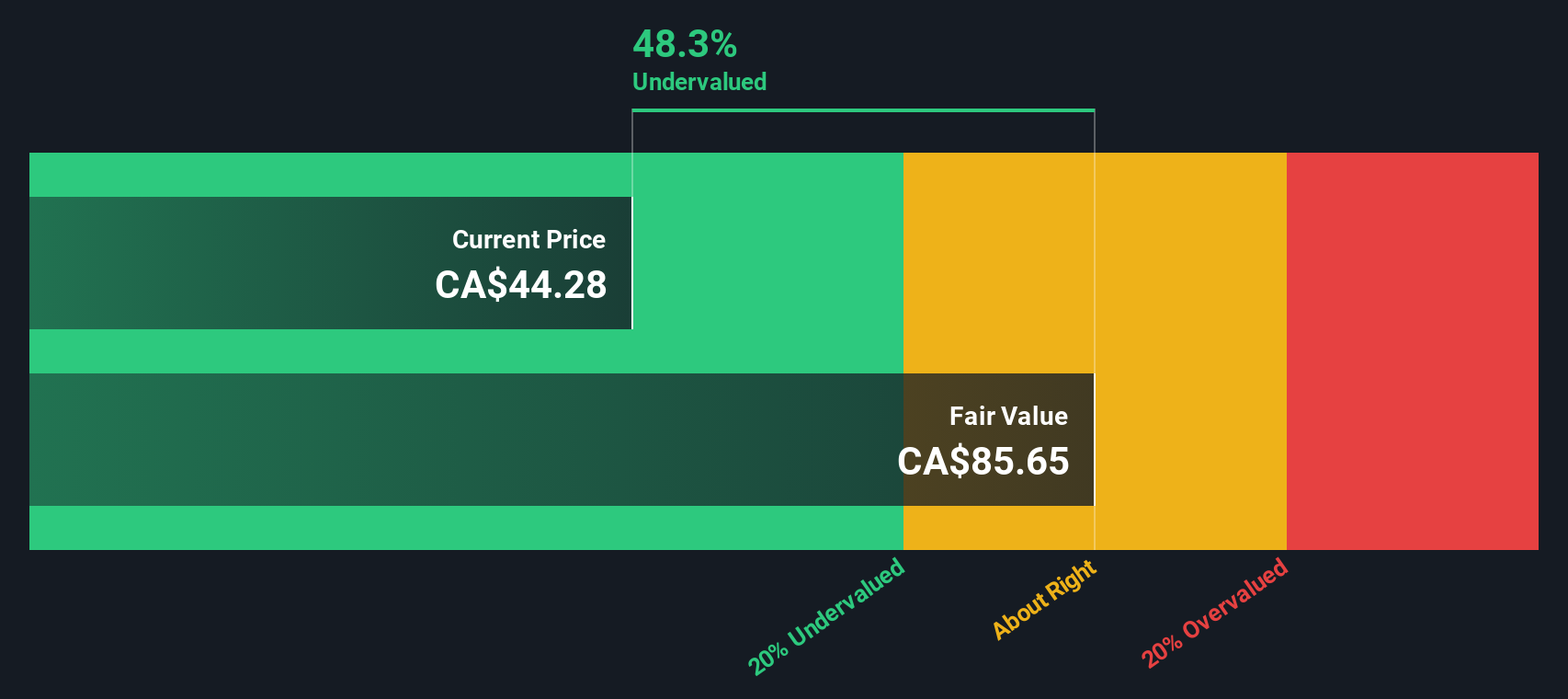

Trisura Group (TSX:TSU)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Trisura Group operates as a specialty insurance provider, focusing on niche markets through its segments including Trisura Specialty and US Programs, with a market capitalization of approximately CA$1.68 billion.

Operations: Trisura Group generates its revenue primarily from Trisura US Programs and Trisura Specialty, with the former contributing significantly more. The company's cost of goods sold (COGS) has been a major component of expenses, impacting its gross profit margin, which has shown variability over time, reaching 5.99% in the latest period. Operating expenses have generally remained lower compared to COGS but have also fluctuated across periods.

PE: 18.5x

Trisura Group, a smaller company in the insurance sector, recently reported a net income of C$28.99 million for Q1 2025, down from C$36.43 million the previous year. Despite this dip, earnings are projected to grow by 23.71% annually. The company relies solely on external borrowing for funding, which carries higher risk but also potential rewards if managed well. Insider confidence is evident as they have been purchasing shares consistently over recent months, signaling belief in future growth prospects.

- Click to explore a detailed breakdown of our findings in Trisura Group's valuation report.

Evaluate Trisura Group's historical performance by accessing our past performance report.

Turning Ideas Into Actions

- Dive into all 164 of the Undervalued Global Small Caps With Insider Buying we have identified here.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hanza might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About OM:HANZA

High growth potential with excellent balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

The "Molecular Pencil": Why Beam's Technology is Built to Win

Fair Value US$65.01|65.4% undervalued

DA

Community Contributor

The silent giant behind virtually every advanced chip powering AI, smartphones, and modern infrastructure.

Fair Value US$310.00|6.1% undervalued

OS

Community Contributor

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Fair Value US$387.77|34.2% undervalued

YI

Community Contributor

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.6% undervalued

BE

Community Contributor