Advertisement

- Canada

- /

- Personal Products

- /

- TSX:JWEL

A Fresh Digital Focus: Assessing Jamieson Wellness (TSX:JWEL) Valuation After Board Appointment of Gayle Tait

Simply Wall St

Reviewed by Simply Wall St

Jamieson Wellness (TSX:JWEL) has named Gayle Tait to its Board of Directors. This move signals the company’s intent to sharpen its digital strategy and accelerate growth in the e-commerce space.

See our latest analysis for Jamieson Wellness.

Jamieson Wellness shares are hovering near CA$34.71 after a choppy stretch, with momentum softening over the last month and a 3.8% one-year total shareholder return. The board’s digital-savvy appointment hints at a renewed push for growth, which could influence sentiment in the quarters ahead.

If this strategic shift has you thinking bigger, consider expanding your search and discover fast growing stocks with high insider ownership.

With Jamieson trading at a notable discount to analyst targets and the board turning to digital leadership, the real question is whether this creates a timely buying opportunity or if the market already anticipates future growth.

Price-to-Earnings of 25.1: Is it justified?

Jamieson Wellness carries a price-to-earnings (P/E) ratio of 25.1, notably above both the North American Personal Products industry average and its close peer group. At a last close of CA$34.71, the market is assigning a premium to the company’s current earnings relative to most sector rivals.

The P/E ratio measures how much investors are willing to pay for each dollar of Jamieson’s earnings. It serves as a common yardstick to compare profitability across similar companies, especially in mature, brand-driven industries. A higher multiple like this suggests high investor confidence in future profit growth, defensible brand value, or unique market positioning.

However, Jamieson's P/E sits well above the industry average of 19.8 and the peer group average of just 15.3. The company is valued at a level more typical of businesses expected to deliver strong, consistent growth. This premium pricing hints that the market anticipates significant upside or perhaps the valuation is stretched compared to fundamentals. Without a calculated fair ratio, it is less clear whether this high multiple is fully warranted, but the gap to sector norms stands out as sizable.

See what the numbers say about this price — find out in our valuation breakdown.

Result: Price-to-Earnings of 25.1 (OVERVALUED)

However, if revenue growth stalls or the digital push fails to boost profits, the market’s optimism could quickly unwind for Jamieson Wellness.

Find out about the key risks to this Jamieson Wellness narrative.

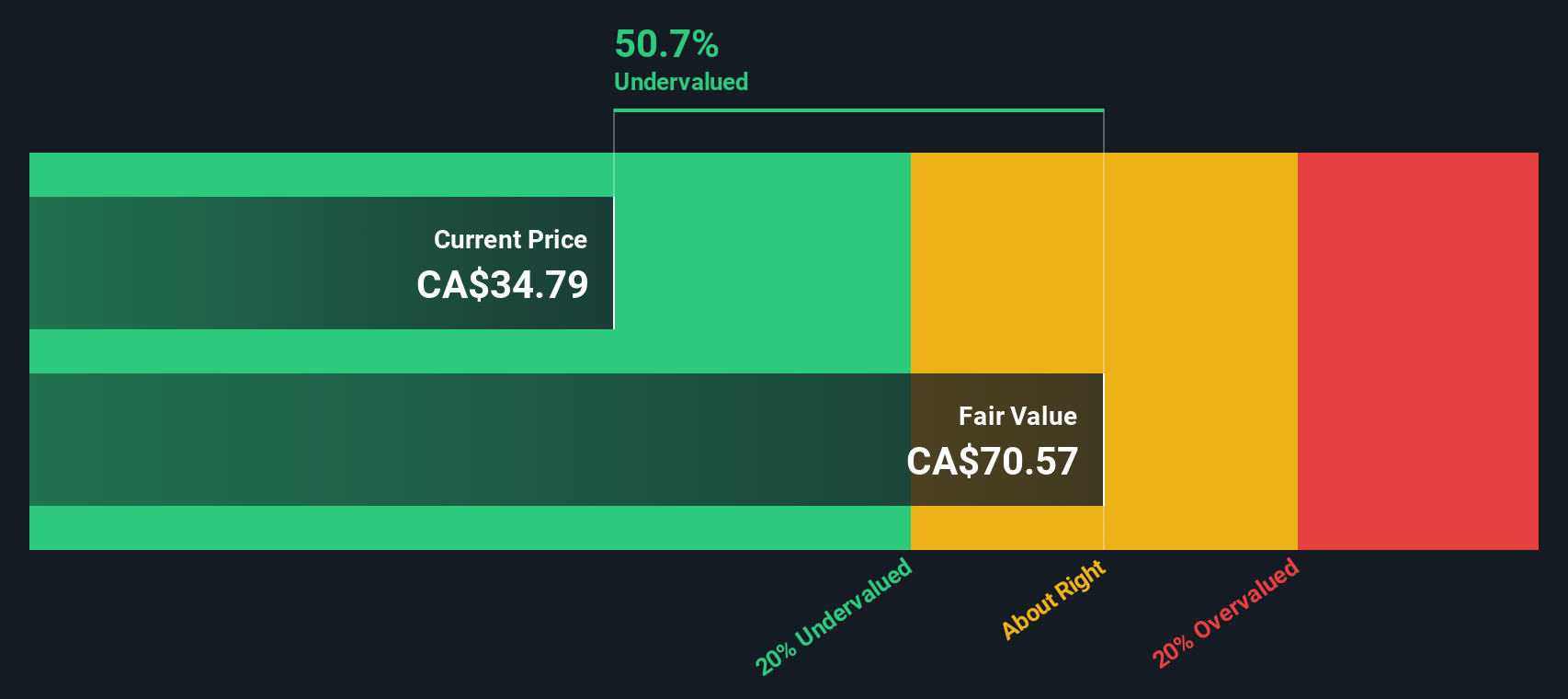

Another View: Discounted Cash Flow Perspective

While Jamieson Wellness looks expensive compared to its peers on earnings multiples, our DCF model presents a very different story. In this perspective, the stock trades at a steep 50% discount to our calculated fair value, which may indicate a significant undervaluation if the model’s assumptions hold.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Jamieson Wellness for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Jamieson Wellness Narrative

If you see things differently or want to dig a little deeper into the data, you can explore the numbers yourself and build a narrative in just a few minutes, using your own approach, Do it your way.

A great starting point for your Jamieson Wellness research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Smart investors never settle for the obvious. Expand your horizons with opportunities you might be missing. The best stocks often hide in plain sight, and the right screener can put them on your radar instantly.

- Unlock the potential of high-yield investments by checking out these 17 dividend stocks with yields > 3%, where you’ll find reliable companies with impressive payouts.

- Seize the early edge in technology by scanning these 27 quantum computing stocks and spot companies racing ahead in the future of quantum computing.

- Jump on powerful trends with these 27 AI penny stocks and tap into the momentum of trailblazers using artificial intelligence to change their industries.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:JWEL

Jamieson Wellness

Develops, manufactures, distributes, markets, and sells the natural health products for human in Canada, the United States, China, and internationally.

Solid track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor