Advertisement

- Canada

- /

- Healthcare Services

- /

- TSX:VMD

Viemed Healthcare (TSE:VMD) Is Growing Earnings But Are They A Good Guide?

Many investors consider it preferable to invest in profitable companies over unprofitable ones, because profitability suggests a business is sustainable. However, sometimes companies receive a one-off boost (or reduction) to their profit, and it's not always clear whether statutory profits are a good guide, going forward. In this article, we'll look at how useful this year's statutory profit is, when analysing Viemed Healthcare (TSE:VMD).

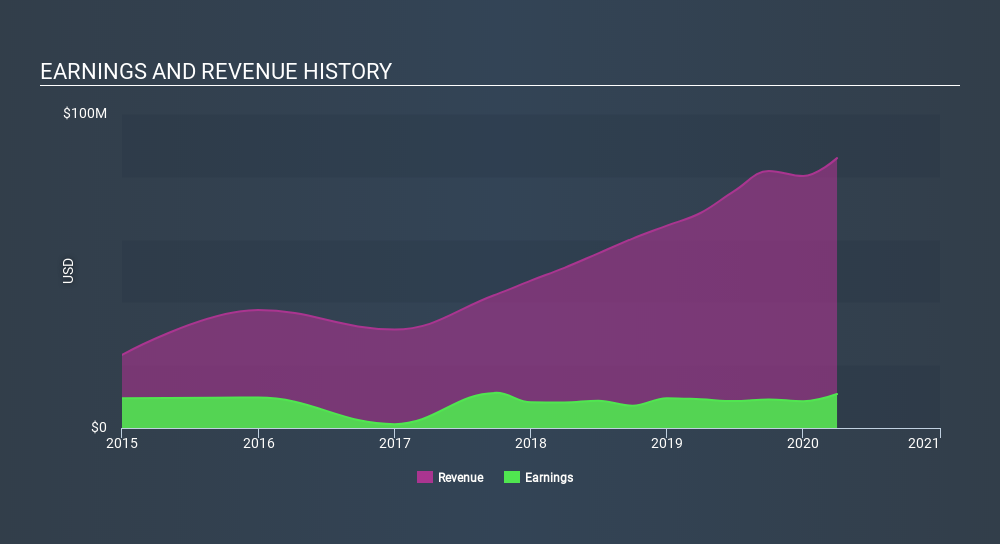

It's good to see that over the last twelve months Viemed Healthcare made a profit of US$10.8m on revenue of US$85.9m. Happily, it has grown both its profit and revenue over the last three years, as you can see in the chart below.

See our latest analysis for Viemed Healthcare

Of course, when it comes to statutory profit, the devil is often in the detail, and we can get a better sense for a company by diving deeper into the financial statements. As a result, today we're going to take a closer look at Viemed Healthcare's cashflow, and unusual items, with a view to understanding what these might tell us about its statutory profit. That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Zooming In On Viemed Healthcare's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. To get the accrual ratio we first subtract FCF from profit for a period, and then divide that number by the average operating assets for the period. The ratio shows us how much a company's profit exceeds its FCF.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. That is not intended to imply we should worry about a positive accrual ratio, but it's worth noting where the accrual ratio is rather high. To quote a 2014 paper by Lewellen and Resutek, "firms with higher accruals tend to be less profitable in the future".

Over the twelve months to March 2020, Viemed Healthcare recorded an accrual ratio of 0.23. Therefore, we know that it's free cashflow was significantly lower than its statutory profit, which is hardly a good thing. In fact, it had free cash flow of US$1.6m in the last year, which was a lot less than its statutory profit of US$10.8m. Viemed Healthcare's free cash flow actually declined over the last year, but it may bounce back next year, since free cash flow is often more volatile than accounting profits. However, that's not all there is to consider. We can see that unusual items have impacted its statutory profit, and therefore the accrual ratio. The good news for shareholders is that Viemed Healthcare's accrual ratio was much better last year, so this year's poor reading might simply be a case of a short term mismatch between profit and FCF. Shareholders should look for improved cashflow relative to profit in the current year, if that is indeed the case.

The Impact Of Unusual Items On Profit

The fact that the company had unusual items boosting profit by US$865k, in the last year, probably goes some way to explain why its accrual ratio was so weak. While we like to see profit increases, we tend to be a little more cautious when unusual items have made a big contribution. We ran the numbers on most publicly listed companies worldwide, and it's very common for unusual items to be once-off in nature. And, after all, that's exactly what the accounting terminology implies. If Viemed Healthcare doesn't see that contribution repeat, then all else being equal we'd expect its profit to drop over the current year.

Our Take On Viemed Healthcare's Profit Performance

Summing up, Viemed Healthcare received a nice boost to profit from unusual items, but could not match its paper profit with free cash flow. Considering all this we'd argue Viemed Healthcare's profits probably give an overly generous impression of its sustainable level of profitability. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. To that end, you should learn about the 3 warning signs we've spotted with Viemed Healthcare (including 1 which shouldn't be ignored).

Our examination of Viemed Healthcare has focussed on certain factors that can make its earnings look better than they are. And, on that basis, we are somewhat skeptical. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About TSX:VMD

Viemed Healthcare

Through its subsidiaries, provides home medical equipment (HME) and post-acute respiratory healthcare services in the United States.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor