- China

- /

- Electronic Equipment and Components

- /

- SHSE:603186

Exploring High Growth Tech Stocks For Potential Portfolio Enhancement

Reviewed by Simply Wall St

In recent weeks, global markets have experienced significant movements, with U.S. stocks rallying on growth and tax hopes following the election results, while the small-cap Russell 2000 Index notably surged by 8.57% for the week. This environment of optimism and policy shifts presents an intriguing backdrop for investors exploring high-growth tech stocks as potential additions to their portfolios; such stocks often exhibit strong revenue growth prospects and innovative capabilities that align well with current market dynamics.

Top 10 High Growth Tech Companies

| Name | Revenue Growth | Earnings Growth | Growth Rating |

|---|---|---|---|

| Material Group | 20.45% | 24.01% | ★★★★★★ |

| Yggdrazil Group | 24.66% | 85.53% | ★★★★★★ |

| eWeLLLtd | 26.52% | 27.53% | ★★★★★★ |

| Ascelia Pharma | 76.15% | 47.16% | ★★★★★★ |

| Medley | 24.98% | 30.36% | ★★★★★★ |

| Seojin SystemLtd | 33.39% | 49.13% | ★★★★★★ |

| Sarepta Therapeutics | 23.89% | 42.65% | ★★★★★★ |

| Mental Health TechnologiesLtd | 27.88% | 79.61% | ★★★★★★ |

| TG Therapeutics | 34.66% | 56.48% | ★★★★★★ |

| UTI | 114.97% | 134.60% | ★★★★★★ |

Click here to see the full list of 1271 stocks from our High Growth Tech and AI Stocks screener.

Below we spotlight a couple of our favorites from our exclusive screener.

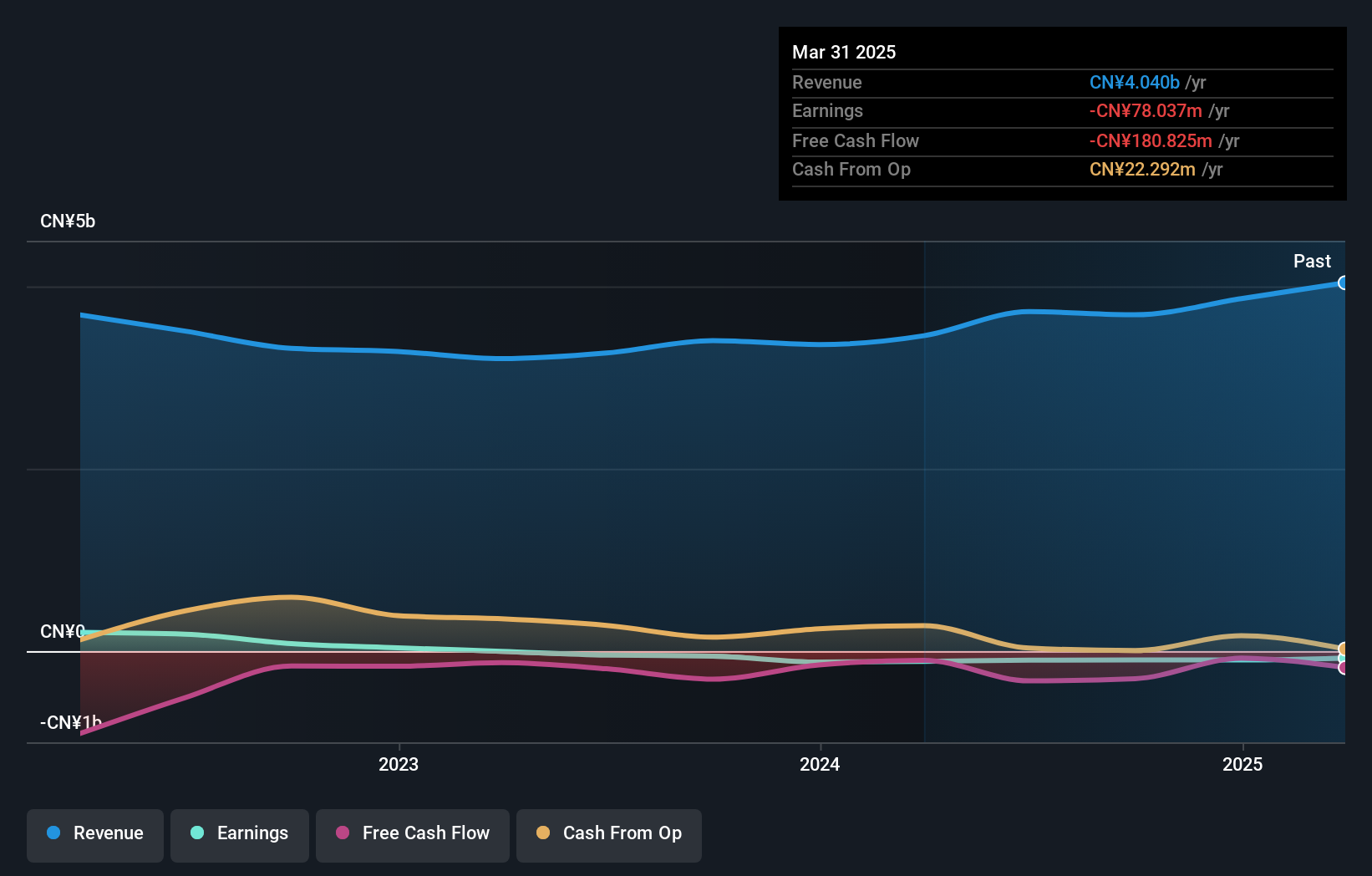

Zhejiang Wazam New MaterialsLTD (SHSE:603186)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Zhejiang Wazam New Materials Co., LTD. specializes in the design, development, production, and sale of copper clad laminates, adhesive sheets, composite materials, and membrane materials with a market capitalization of CN¥4.49 billion.

Operations: Zhejiang Wazam New Materials Co., LTD. focuses on producing and selling copper clad laminates, adhesive sheets, composite materials, and membrane materials. The company operates with a market capitalization of CN¥4.49 billion.

Zhejiang Wazam New Materials Co., LTD. is demonstrating robust potential in the tech sector with its revenue projected to expand by 25.9% annually, outpacing the Chinese market's growth rate of 14.1%. Despite current unprofitability, the company's earnings are expected to surge by an impressive 188.15% per year over the next three years, indicating a swift move towards profitability. This financial trajectory is supported by significant investments in R&D, aligning with recent earnings reports showing a reduction in net loss from CNY 30.52 million to CNY 6.65 million and an increase in sales from CNY 2,497.17 million to CNY 2,823.75 million within nine months of this year alone—evidence of strategic initiatives beginning to bear fruit amidst challenging market conditions.

freee K.K (TSE:4478)

Simply Wall St Growth Rating: ★★★★★☆

Overview: freee K.K. provides cloud-based accounting and HR software solutions in Japan with a market capitalization of ¥171.97 billion.

Operations: The company generates revenue primarily from its Platform Business, amounting to ¥25.43 billion. Its focus on cloud-based solutions positions it within the technology sector in Japan.

Freee K.K. is navigating a transformative phase, with its revenue forecast to grow by 18.2% annually, outstripping the Japanese market's average of 4.2%. This growth trajectory is underpinned by substantial R&D investment, representing 74.8% of its revenue, which fuels innovation and competitive edge in financial software solutions. Recent executive changes and strategic amendments to company bylaws signal a proactive approach to governance and business expansion, aiming to capitalize on emerging opportunities in tech-driven financial services for small businesses. The firm's focus on enhancing its integrated ERP systems through these initiatives suggests a promising outlook despite current unprofitability.

- Click here to discover the nuances of freee K.K with our detailed analytical health report.

Gain insights into freee K.K's historical performance by reviewing our past performance report.

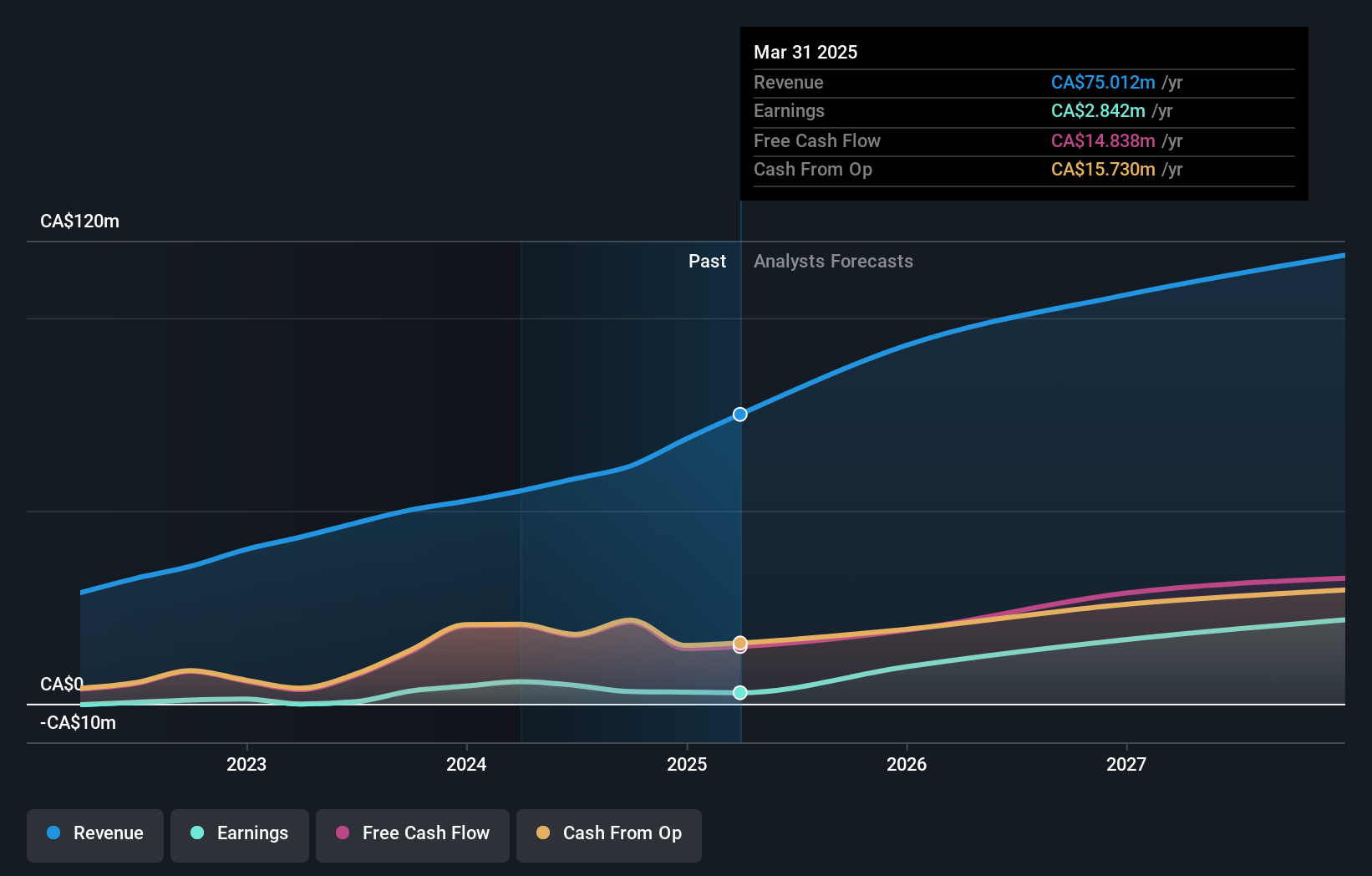

Vitalhub (TSX:VHI)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Vitalhub Corp. develops technology solutions for health and human service providers across Canada, the United States, the United Kingdom, Australia, Western Asia, and internationally with a market cap of CA$579.89 million.

Operations: Vitalhub Corp. generates revenue primarily from its healthcare software segment, which contributes CA$58.32 million. The company operates in multiple international markets, including Canada, the United States, and the United Kingdom.

Vitalhub Corp., recently added to the S&P Global BMI Index, showcases a robust growth trajectory with an anticipated revenue increase of 19.7% annually, outpacing the Canadian market's average of 7.2%. This growth is further underscored by a remarkable earnings surge of 877.1% over the past year, significantly exceeding its industry's average. Despite facing challenges like a one-off loss of CA$3.1M, Vitalhub's aggressive R&D spending—vital for fostering innovation in healthcare technology—positions it well within the high-growth tech landscape as it prepares to announce Q3 results today. The company's strategic presentations at significant forums such as the Cantech Letter Investment Conference highlight its commitment to maintaining momentum and visibility in competitive sectors. With earnings forecasted to grow by an impressive 67.3% annually over the next three years, Vitalhub is poised for continued expansion in its market segment, leveraging substantial investments in technology development to potentially revolutionize healthcare services delivery.

- Click to explore a detailed breakdown of our findings in Vitalhub's health report.

Understand Vitalhub's track record by examining our Past report.

Turning Ideas Into Actions

- Investigate our full lineup of 1271 High Growth Tech and AI Stocks right here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Streamline your investment strategy with Simply Wall St's app for free and benefit from extensive research on stocks across all corners of the world.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Zhejiang Wazam New MaterialsLTD might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SHSE:603186

Zhejiang Wazam New MaterialsLTD

Engages in the design, development, production, and sale of copper clad laminates and adhesive sheets, composite materials, and membrane materials.

Undervalued with high growth potential.