Advertisement

- Canada

- /

- Healthcare Services

- /

- TSX:EXE

Why We Think Extendicare Inc.'s (TSE:EXE) CEO Compensation Is Not Excessive At All

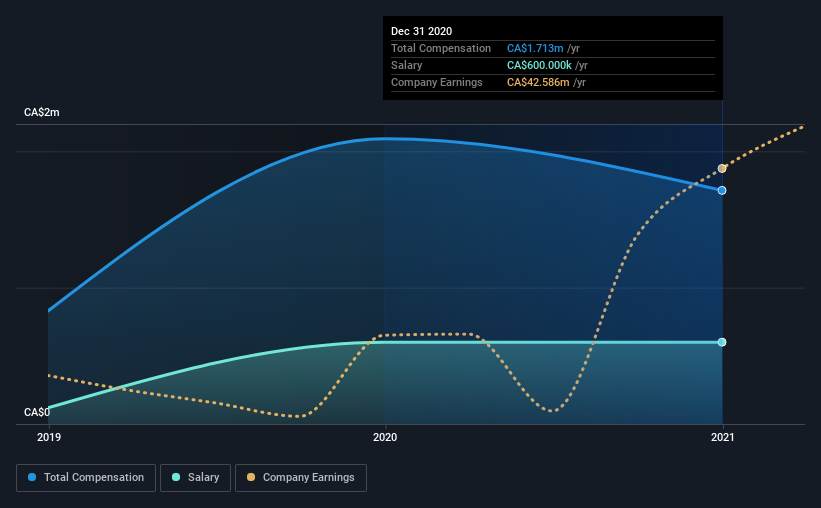

Under the guidance of CEO Michael Guerriere, Extendicare Inc. (TSE:EXE) has performed reasonably well recently. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 27 May 2021. Based on our analysis of the data below, we think CEO compensation seems reasonable for now.

View our latest analysis for Extendicare

How Does Total Compensation For Michael Guerriere Compare With Other Companies In The Industry?

At the time of writing, our data shows that Extendicare Inc. has a market capitalization of CA$716m, and reported total annual CEO compensation of CA$1.7m for the year to December 2020. Notably, that's a decrease of 18% over the year before. While we always look at total compensation first, our analysis shows that the salary component is less, at CA$600k.

For comparison, other companies in the same industry with market capitalizations ranging between CA$242m and CA$969m had a median total CEO compensation of CA$1.6m. This suggests that Extendicare remunerates its CEO largely in line with the industry average. Furthermore, Michael Guerriere directly owns CA$323k worth of shares in the company.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | CA$600k | CA$600k | 35% |

| Other | CA$1.1m | CA$1.5m | 65% |

| Total Compensation | CA$1.7m | CA$2.1m | 100% |

On an industry level, roughly 40% of total compensation represents salary and 60% is other remuneration. In Extendicare's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

A Look at Extendicare Inc.'s Growth Numbers

Over the past three years, Extendicare Inc. has seen its earnings per share (EPS) grow by 17% per year. It achieved revenue growth of 7.0% over the last year.

Shareholders would be glad to know that the company has improved itself over the last few years. It's good to see a bit of revenue growth, as this suggests the business is able to grow sustainably. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Extendicare Inc. Been A Good Investment?

Extendicare Inc. has served shareholders reasonably well, with a total return of 29% over three years. But they would probably prefer not to see CEO compensation far in excess of the median.

To Conclude...

The company's decent performance might have made most shareholders happy, possibly making CEO remuneration the least of the concerns to be discussed in the upcoming AGM. Despite the pleasing results, we still think that any proposed increases to CEO compensation will be examined based on a case by case basis and linked to performance outcomes.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. In our study, we found 3 warning signs for Extendicare you should be aware of, and 2 of them are concerning.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

When trading stocks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Extendicare might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About TSX:EXE

Extendicare

Through its subsidiaries, provides care and services for seniors in Canada.

Solid track record established dividend payer.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|1.3% undervalued

TI

Community Contributor