- Canada

- /

- Oil and Gas

- /

- TSX:CNQ

Canadian Natural Resources And 2 More Top TSX Dividend Stocks

Reviewed by Simply Wall St

The Canadian market has shown robust performance, with a 10% increase over the past year and earnings expected to grow by 15% annually. In this thriving environment, dividend stocks like Canadian Natural Resources stand out as appealing options for investors looking for steady income and potential growth.

Top 10 Dividend Stocks In Canada

| Name | Dividend Yield | Dividend Rating |

| Bank of Nova Scotia (TSX:BNS) | 6.71% | ★★★★★★ |

| Whitecap Resources (TSX:WCP) | 7.34% | ★★★★★★ |

| Secure Energy Services (TSX:SES) | 3.53% | ★★★★★☆ |

| Boston Pizza Royalties Income Fund (TSX:BPF.UN) | 8.15% | ★★★★★☆ |

| Enghouse Systems (TSX:ENGH) | 3.45% | ★★★★★☆ |

| Russel Metals (TSX:RUS) | 4.30% | ★★★★★☆ |

| Royal Bank of Canada (TSX:RY) | 3.73% | ★★★★★☆ |

| Firm Capital Mortgage Investment (TSX:FC) | 8.52% | ★★★★★☆ |

| Canadian Natural Resources (TSX:CNQ) | 4.41% | ★★★★★☆ |

| Canadian Western Bank (TSX:CWB) | 3.01% | ★★★★★☆ |

Click here to see the full list of 33 stocks from our Top TSX Dividend Stocks screener.

Here's a peek at a few of the choices from the screener.

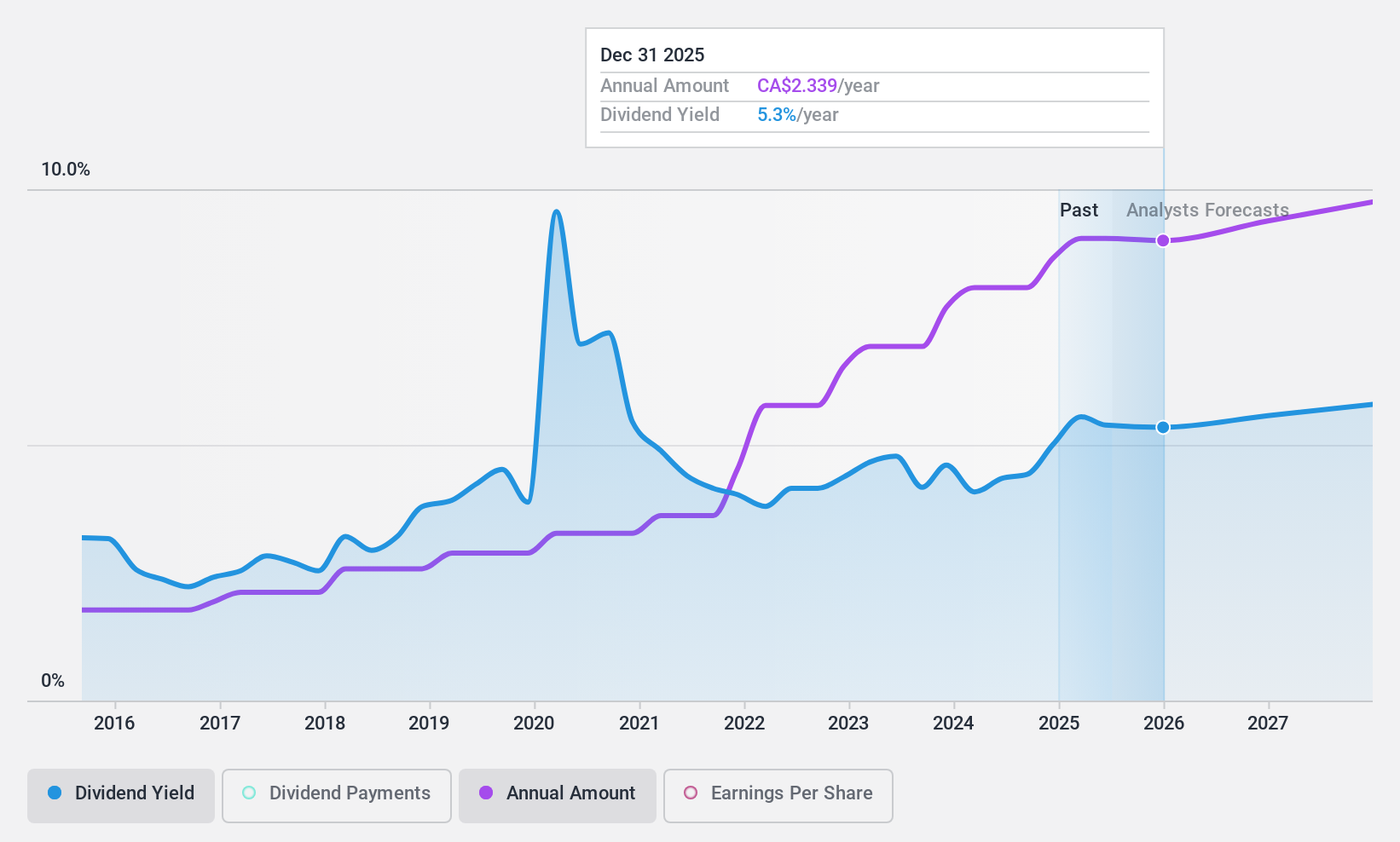

Canadian Natural Resources (TSX:CNQ)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: Canadian Natural Resources Limited, with a market capitalization of CA$101.73 billion, is engaged in the acquisition, exploration, development, production, marketing, and sale of crude oil, natural gas, and natural gas liquids.

Operations: Canadian Natural Resources Limited generates revenue primarily through its segments: Oil Sands Mining and Upgrading (CA$15.80 billion), Exploration and Production - North America (CA$17.43 billion), with smaller contributions from Midstream and Refining (CA$0.97 billion), Exploration and Production - North Sea (CA$0.58 billion), and Exploration and Production - Offshore Africa (CA$0.57 billion).

Dividend Yield: 4.4%

Canadian Natural Resources Limited offers a consistent dividend yield of 4.41%, although it's below the top tier in the Canadian market. The dividends are sustainably covered by both earnings and cash flows, with payout ratios at 56.2% and 48.8% respectively, indicating reliability without overextending financial resources. Recent financials show a dip in net income from CAD 1,799 million to CAD 987 million year-over-year for Q1 2024, but the company maintains its commitment to shareholder returns with stable dividends and active share buybacks totaling CAD 3,533 million since January this year.

- Take a closer look at Canadian Natural Resources' potential here in our dividend report.

- The valuation report we've compiled suggests that Canadian Natural Resources' current price could be quite moderate.

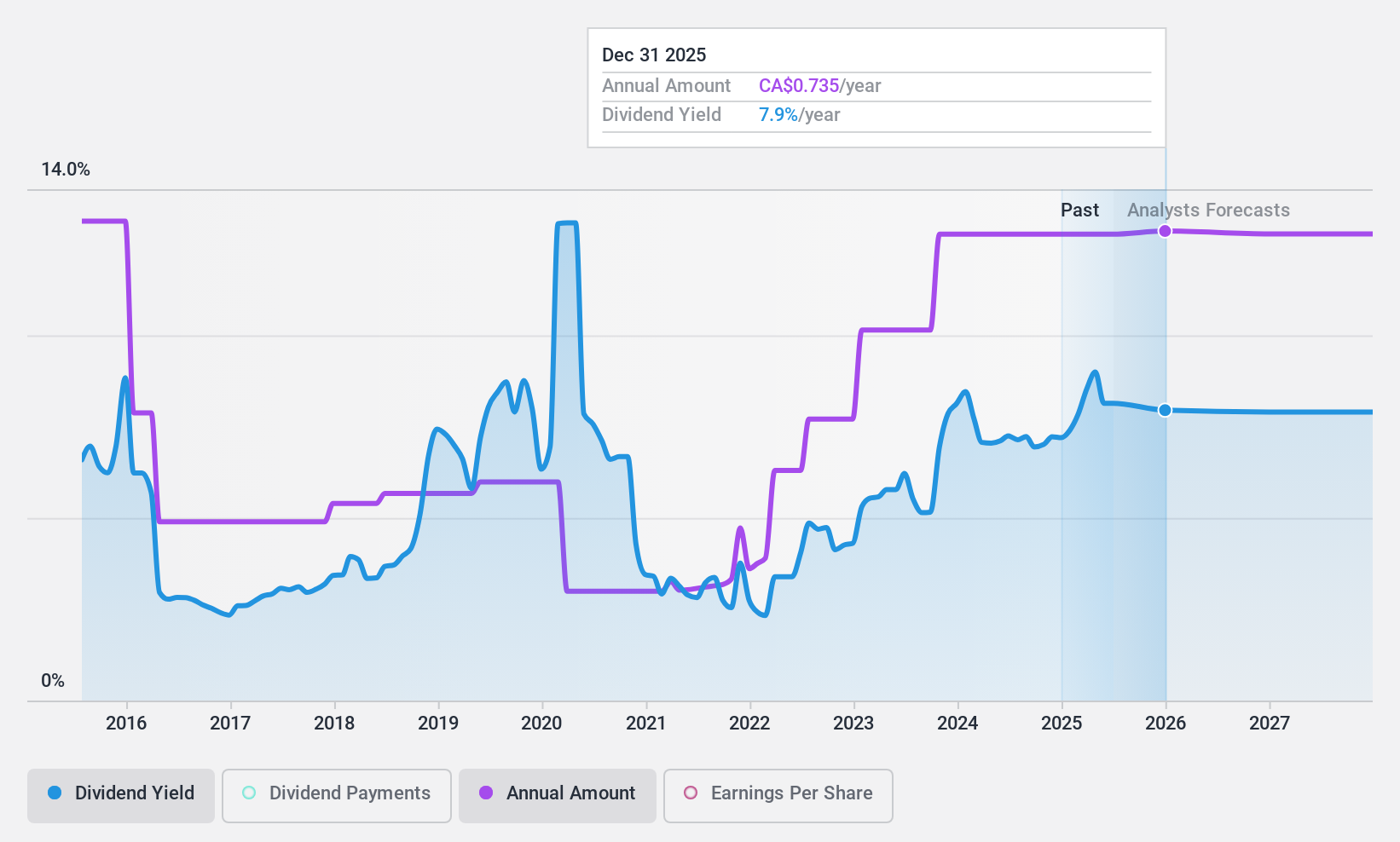

Rogers Sugar (TSX:RSI)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Rogers Sugar Inc. operates in the refining, packaging, marketing, and distribution of sugar and maple products across Canada, the U.S., Europe, and other international markets with a market cap of approximately CA$729.13 million.

Operations: Rogers Sugar Inc. generates CA$944.83 million from its sugar operations and CA$215.14 million from its maple products sales.

Dividend Yield: 6.4%

Rogers Sugar Inc. (RSI) exhibits a mixed dividend profile with a high yield of 6.39%, ranking it in the top 25% of Canadian dividend payers. However, its dividends are not well supported by earnings or cash flows, with a payout ratio reaching 193.3%. Recent financials show improvement; Q2 sales increased to CAD 300.94 million from CAD 272.95 million year-over-year, and net income rose to CAD 13.94 million from CAD 11.06 million, suggesting potential stability despite high debt levels and unchanged dividends over the past decade.

- Unlock comprehensive insights into our analysis of Rogers Sugar stock in this dividend report.

- Our expertly prepared valuation report Rogers Sugar implies its share price may be lower than expected.

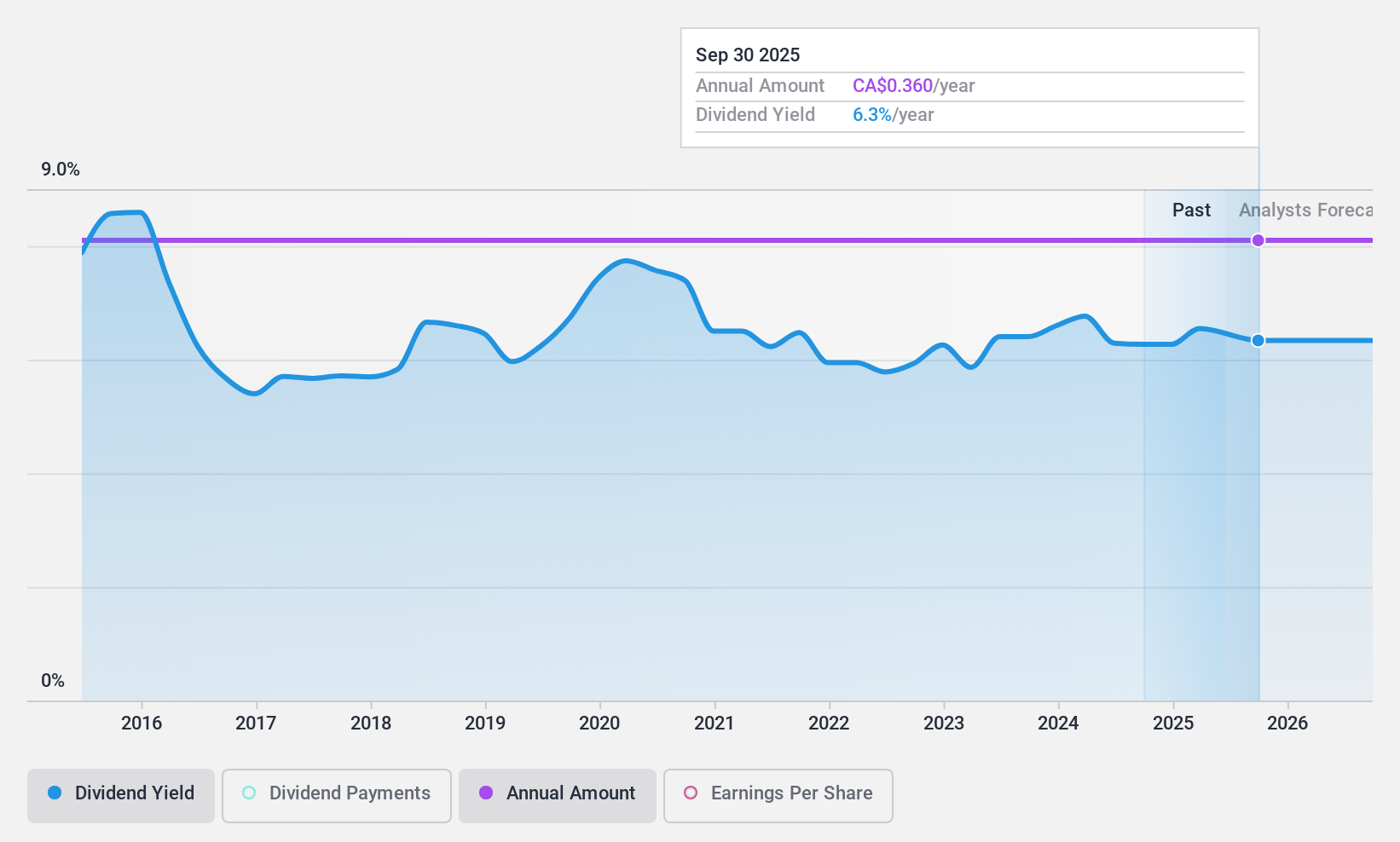

Whitecap Resources (TSX:WCP)

Simply Wall St Dividend Rating: ★★★★★★

Overview: Whitecap Resources Inc. is an oil and gas company specializing in the acquisition, development, and production of petroleum and natural gas assets in Western Canada, with a market capitalization of approximately CA$5.97 billion.

Operations: Whitecap Resources Inc. generates its revenue primarily from the exploration and production of oil and gas, totaling approximately CA$3.23 billion.

Dividend Yield: 7.3%

Whitecap Resources has demonstrated a solid track record in dividend performance, with stable and growing payouts over the past decade, currently offering a high yield of 7.34%, placing it among the top dividend payers in Canada. The dividends are well-supported by both earnings and cash flows, with payout ratios of 56.1% and 82% respectively. Despite trading below fair value by 31.9%, recent financial results indicate robust revenue growth to CAD 905.4 million in Q2 from CAD 790 million the previous year, alongside increased net income to CAD 244.5 million from CAD 175.4 million, signaling strong operational performance and potential for continued dividend reliability amidst strategic acquisitions aimed at long-term shareholder value creation.

- Click here to discover the nuances of Whitecap Resources with our detailed analytical dividend report.

- Upon reviewing our latest valuation report, Whitecap Resources' share price might be too pessimistic.

Taking Advantage

- Click this link to deep-dive into the 33 companies within our Top TSX Dividend Stocks screener.

- Hold shares in these firms? Setup your portfolio in Simply Wall St to seamlessly track your investments and receive personalized updates on your portfolio's performance.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:CNQ

Canadian Natural Resources

Acquires, explores for, develops, produces, markets, and sells crude oil, natural gas, and natural gas liquids (NGLs).

Established dividend payer and good value.