- Canada

- /

- Oil and Gas

- /

- TSXV:EU

enCore Energy Corp. (CVE:EU) Just Released Its Third-Quarter Earnings: Here's What Analysts Think

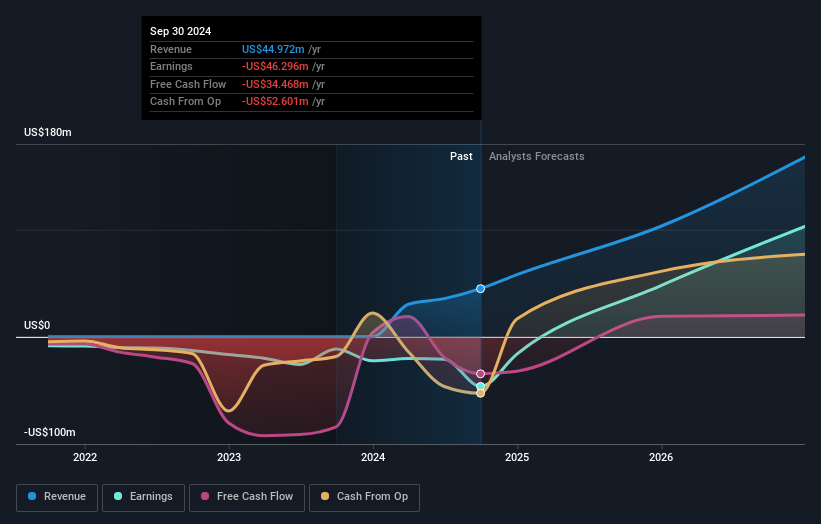

enCore Energy Corp. (CVE:EU) shareholders are probably feeling a little disappointed, since its shares fell 4.2% to CA$5.06 in the week after its latest third-quarter results. The results don't look great, especially considering that statutory losses grew 417% toUS$0.10 per share. Revenues of US$9.6m did beat expectations by 9.7%, but it looks like a bit of a cold comfort. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. We thought readers would find it interesting to see the analysts latest (statutory) post-earnings forecasts for next year.

See our latest analysis for enCore Energy

Taking into account the latest results, the consensus forecast from enCore Energy's three analysts is for revenues of US$103.2m in 2025. This reflects a major 130% improvement in revenue compared to the last 12 months. Earnings are expected to improve, with enCore Energy forecast to report a statutory profit of US$0.26 per share. Before this earnings report, the analysts had been forecasting revenues of US$104.9m and earnings per share (EPS) of US$0.12 in 2025. There was no real change to the revenue estimates, but the analysts do seem more bullish on earnings, given the massive increase in earnings per share expectations following these results.

The consensus price target was unchanged at CA$8.00, implying that the improved earnings outlook is not expected to have a long term impact on value creation for shareholders. That's not the only conclusion we can draw from this data however, as some investors also like to consider the spread in estimates when evaluating analyst price targets. Currently, the most bullish analyst values enCore Energy at CA$10.00 per share, while the most bearish prices it at CA$7.00. This shows there is still a bit of diversity in estimates, but analysts don't appear to be totally split on the stock as though it might be a success or failure situation.

These estimates are interesting, but it can be useful to paint some more broad strokes when seeing how forecasts compare, both to the enCore Energy's past performance and to peers in the same industry. The period to the end of 2025 brings more of the same, according to the analysts, with revenue forecast to display 94% growth on an annualised basis. That is in line with its 100% annual growth over the past five years. Compare this with the broader industry, which analyst estimates (in aggregate) suggest will see revenues grow 1.7% annually. So although enCore Energy is expected to maintain its revenue growth rate, it's definitely expected to grow faster than the wider industry.

The Bottom Line

The biggest takeaway for us is the consensus earnings per share upgrade, which suggests a clear improvement in sentiment around enCore Energy's earnings potential next year. Happily, there were no major changes to revenue forecasts, with the business still expected to grow faster than the wider industry. The consensus price target held steady at CA$8.00, with the latest estimates not enough to have an impact on their price targets.

Following on from that line of thought, we think that the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for enCore Energy going out to 2026, and you can see them free on our platform here..

And what about risks? Every company has them, and we've spotted 1 warning sign for enCore Energy you should know about.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSXV:EU

enCore Energy

Engages in the acquisition, exploration, development, and extraction of uranium resource properties in the United States.

High growth potential and good value.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Automotive Electronics Manufacturer Consistent and Stable

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion