- Canada

- /

- Oil and Gas

- /

- TSX:VET

Analysts Are Betting On Vermilion Energy Inc. (TSE:VET) With A Big Upgrade This Week

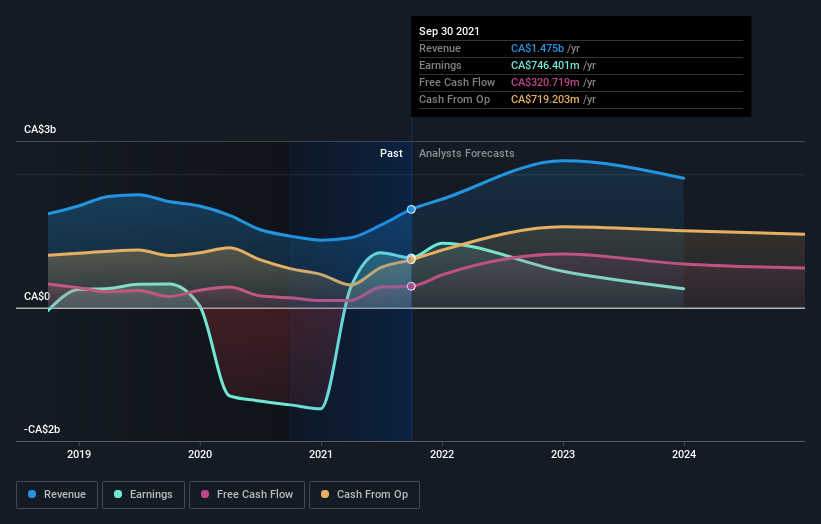

Celebrations may be in order for Vermilion Energy Inc. (TSE:VET) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The analysts have sharply increased their revenue numbers, with a view that Vermilion Energy will make substantially more sales than they'd previously expected. The market may be pricing in some blue sky too, with the share price gaining 11% to CA$17.68 in the last 7 days. Could this upgrade be enough to drive the stock even higher?

After this upgrade, Vermilion Energy's three analysts are now forecasting revenues of CA$2.2b in 2022. This would be a sizeable 49% improvement in sales compared to the last 12 months. Prior to the latest estimates, the analysts were forecasting revenues of CA$2.0b in 2022. It looks like there's been a clear increase in optimism around Vermilion Energy, given the decent improvement in revenue forecasts.

See our latest analysis for Vermilion Energy

Additionally, the consensus price target for Vermilion Energy increased 6.7% to CA$18.14, showing a clear increase in optimism from the analysts involved. It could also be instructive to look at the range of analyst estimates, to evaluate how different the outlier opinions are from the mean. Currently, the most bullish analyst values Vermilion Energy at CA$30.00 per share, while the most bearish prices it at CA$13.00. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that Vermilion Energy's rate of growth is expected to accelerate meaningfully, with the forecast 38% annualised revenue growth to the end of 2022 noticeably faster than its historical growth of 6.8% p.a. over the past five years. Compare this with other companies in the same industry, which are forecast to grow their revenue 6.6% annually. Factoring in the forecast acceleration in revenue, it's pretty clear that Vermilion Energy is expected to grow much faster than its industry.

The Bottom Line

The most important thing to take away from this upgrade is that analysts lifted their revenue estimates for next year. Analysts also expect revenues to grow faster than the wider market. There was also an increase in the price target, suggesting that there is more optimism baked into the forecasts than there was previously. Seeing the dramatic upgrade to next year's forecasts, it might be time to take another look at Vermilion Energy.

Analysts are clearly in love with Vermilion Energy at the moment, but before diving in - you should be aware that we've identified some warning flags with the business, such as a weak balance sheet. For more information, you can click through to our platform to learn more about this and the 4 other warning signs we've identified .

You can also see our analysis of Vermilion Energy's Board and CEO remuneration and experience, and whether company insiders have been buying stock.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About TSX:VET

Vermilion Energy

An oil and gas producer, focuses on the acquisition, exploration, development, and optimization of producing properties in North America, Europe, and Australia.

Undervalued low.

Similar Companies

Market Insights

Community Narratives