Advertisement

Gildan Activewear And 2 Other TSX Stocks That Might Be Trading Below Their Estimated Value

Simply Wall St

Reviewed by Simply Wall St

As the Canadian market navigates a landscape of manageable yet persistent inflation and potential rate cuts, investors are keenly observing how these economic shifts might influence stock valuations. In this context, identifying stocks that may be trading below their estimated value becomes crucial, as they could offer opportunities for growth amidst evolving market conditions.

Top 10 Undervalued Stocks Based On Cash Flows In Canada

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| West Fraser Timber (TSX:WFG) | CA$101.52 | CA$172.34 | 41.1% |

| WELL Health Technologies (TSX:WELL) | CA$5.00 | CA$9.81 | 49% |

| TerraVest Industries (TSX:TVK) | CA$137.25 | CA$273.77 | 49.9% |

| Magellan Aerospace (TSX:MAL) | CA$15.50 | CA$28.55 | 45.7% |

| K92 Mining (TSX:KNT) | CA$15.26 | CA$27.89 | 45.3% |

| Ivanhoe Mines (TSX:IVN) | CA$11.31 | CA$19.97 | 43.4% |

| Groupe Dynamite (TSX:GRGD) | CA$38.20 | CA$70.82 | 46.1% |

| goeasy (TSX:GSY) | CA$206.49 | CA$382.04 | 46% |

| Blackline Safety (TSX:BLN) | CA$6.20 | CA$10.18 | 39.1% |

| Allied Gold (TSX:AAUC) | CA$18.01 | CA$28.46 | 36.7% |

Let's take a closer look at a couple of our picks from the screened companies.

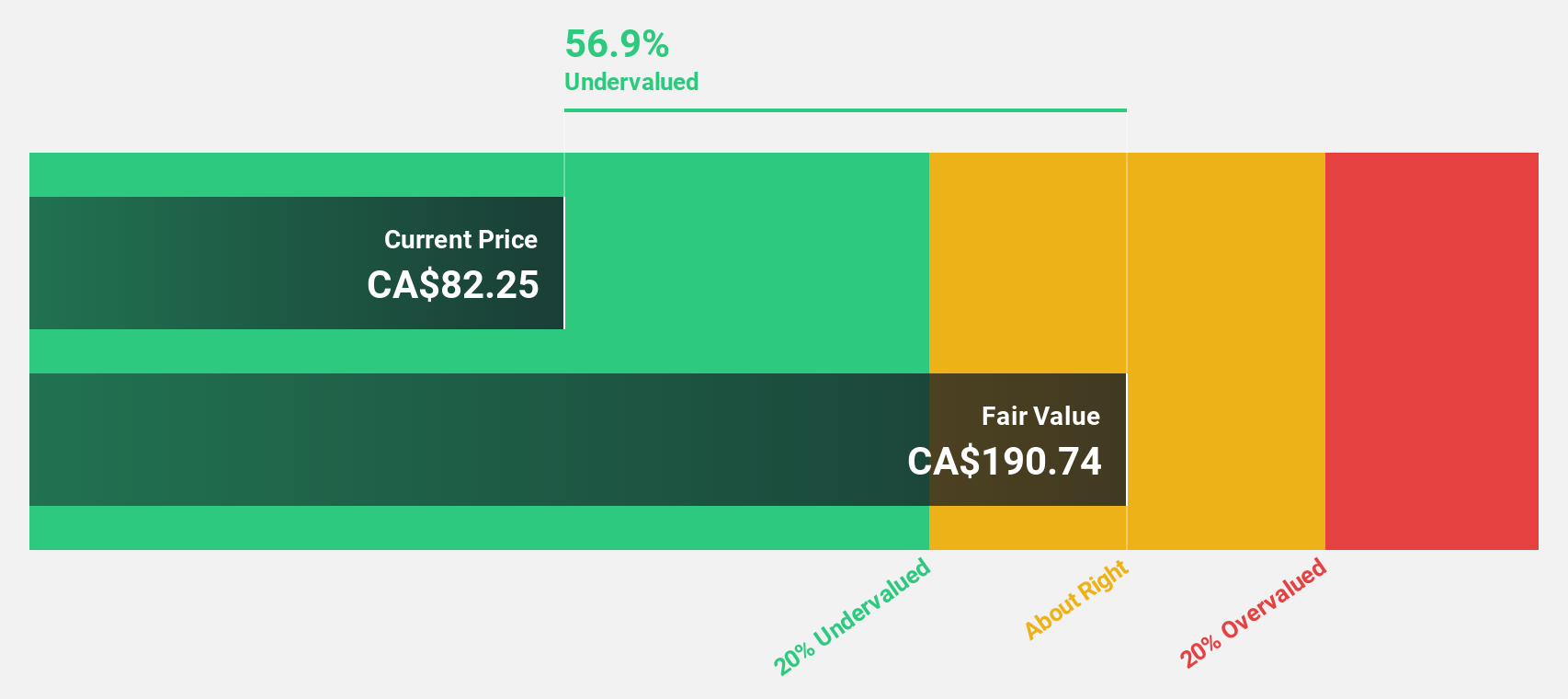

Gildan Activewear (TSX:GIL)

Overview: Gildan Activewear Inc. is a company that manufactures and sells various apparel products, with a market cap of CA$11.63 billion.

Operations: The company's revenue segment for apparel amounts to $3.34 billion.

Estimated Discount To Fair Value: 20%

Gildan Activewear is trading at approximately 20% below its estimated fair value, presenting an opportunity for investors focused on cash flow valuation. Despite holding a high level of debt, the company has demonstrated strong financial performance with net income rising to US$137.93 million in Q2 2025 from US$58.4 million a year ago. Earnings are projected to grow at 18.48% annually, outpacing the Canadian market's growth rate of 10.9%.

- Our earnings growth report unveils the potential for significant increases in Gildan Activewear's future results.

- Click to explore a detailed breakdown of our findings in Gildan Activewear's balance sheet health report.

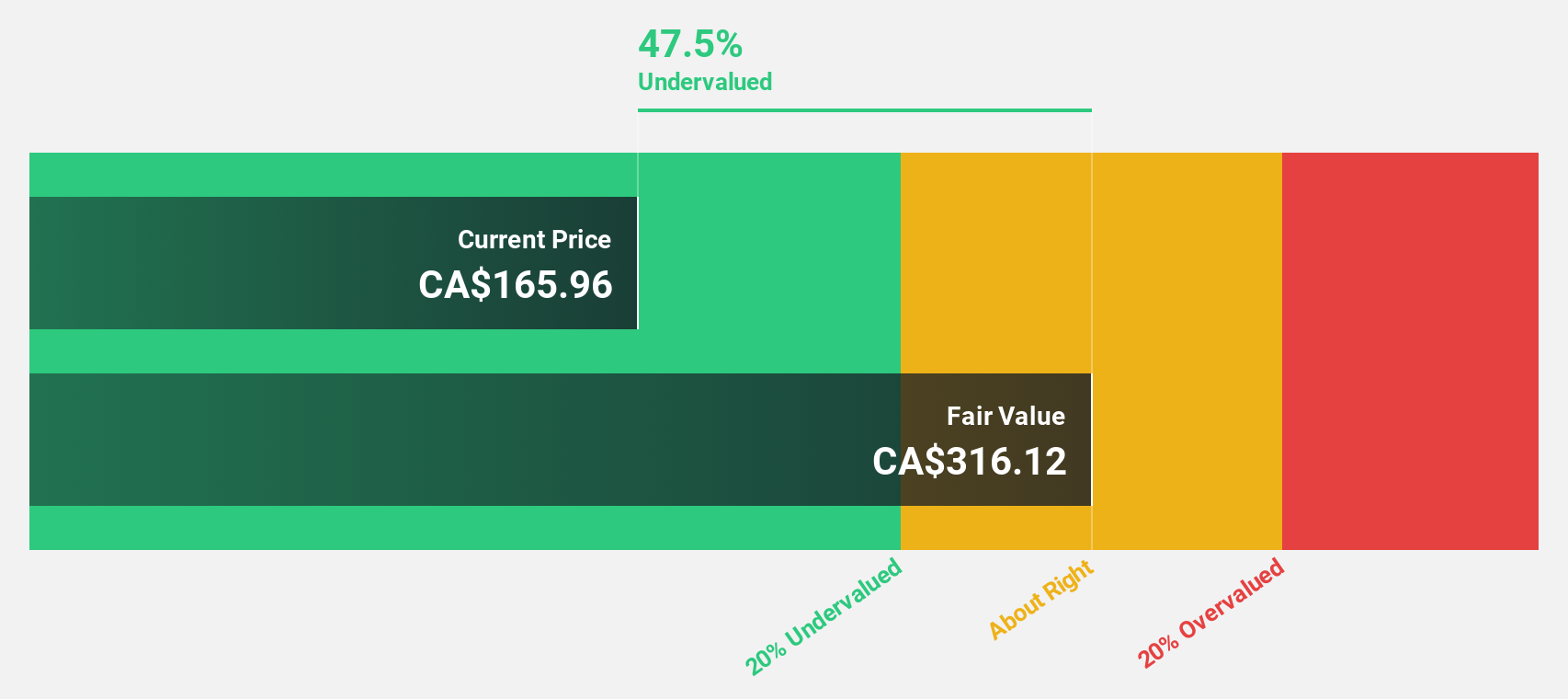

TerraVest Industries (TSX:TVK)

Overview: TerraVest Industries Inc. is a diversified manufacturer providing goods and services to sectors such as agriculture, mining, energy, and more across Canada, the United States, and internationally with a market cap of CA$3.01 billion.

Operations: The company's revenue is primarily derived from its Compressed Gas Equipment segment at CA$482.68 million, followed by HVAC and Containment Equipment at CA$380.50 million, Service at CA$221.65 million, and Processing Equipment at CA$103.10 million.

Estimated Discount To Fair Value: 49.9%

TerraVest Industries is trading at CA$137.25, significantly below its estimated fair value of CA$273.77, highlighting potential undervaluation based on cash flows. Despite a recent dip in quarterly net income to CA$11.25 million from CA$11.92 million, nine-month revenue surged to CA$951.74 million from the previous year's CA$681.16 million, reflecting strong growth prospects with forecasted earnings and revenue increases of 22.1% and 25.1% annually, respectively, surpassing market averages.

- According our earnings growth report, there's an indication that TerraVest Industries might be ready to expand.

- Click here to discover the nuances of TerraVest Industries with our detailed financial health report.

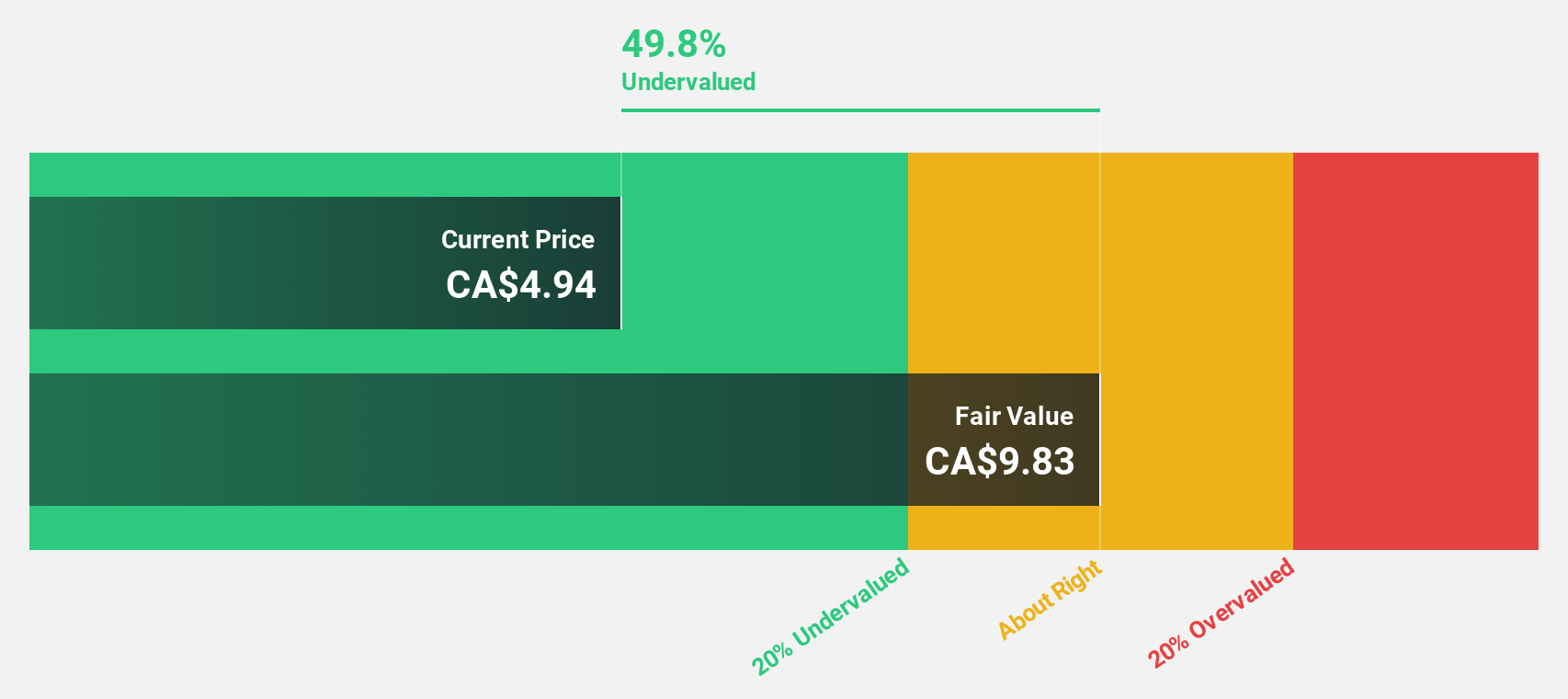

WELL Health Technologies (TSX:WELL)

Overview: WELL Health Technologies Corp. is a practitioner-focused digital healthcare company operating in Canada, the United States, and internationally with a market cap of CA$1.21 billion.

Operations: WELL Health Technologies generates revenue through SaaS and Technology Services (CA$80.89 million), Specialized-provider Staffing (CA$168.94 million), Canadian Patient Services - Primary (CA$229.16 million), WELL Health USA Patient Services - Primary WISP (CA$113.10 million), Canadian Patient Services - Specialized Myhealth (CA$152.50 million), WELL Health USA Patient Services - Primary Circle Medical (CA$103.19 million), and WELL Health USA Patient Services - Specialized CRH Medical (CA$241.55 million).

Estimated Discount To Fair Value: 49%

WELL Health Technologies, trading at CA$5, is significantly undervalued with an estimated fair value of CA$9.81. Despite a drop in net income to CA$12.15 million from last year's very large figure, WELL's revenue for Q2 rose sharply to CA$356.67 million from CA$227.31 million year-over-year. Forecasted annual earnings growth of 129.47% and revenue growth of 14.3% exceed Canadian market averages, supported by strategic expansions and robust financing arrangements through 2027.

- Upon reviewing our latest growth report, WELL Health Technologies' projected financial performance appears quite optimistic.

- Take a closer look at WELL Health Technologies' balance sheet health here in our report.

Where To Now?

- Get an in-depth perspective on all 27 Undervalued TSX Stocks Based On Cash Flows by using our screener here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Simply Wall St is a revolutionary app designed for long-term stock investors, it's free and covers every market in the world.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSX:GIL

Very undervalued with exceptional growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor